The Consumer Retail Investment Banking Group: King of the Generalists?

Ask anyone joining a large bank which group they’re most interested in, and consumer retail investment banking is a likely answer.

It’s a great place for anyone who wants to work with well-known companies and brands, gain general valuation/modeling experience, and keep their exit options open.

The benefits of the group are almost like the benefits of getting into investment banking: brand/prestige, technical skills, and exit opportunities.

If you’re unsure about your long-term plans but you want to earn a lot and are willing to put in long hours, why not join the consumer retail group?

That’s a good question, but before answering it, I’ll start by explaining the entire sector:

Consumer Retail Investment Banking Defined

Consumer Retail Investment Banking Definition: In consumer retail IB, bankers advise companies in the consumer staples, consumer discretionary, and retail industries on raising debt and equity and completing mergers, acquisitions, and restructuring/bankruptcy deals.

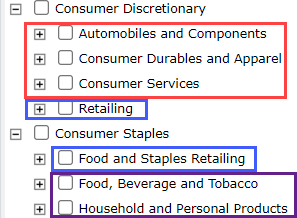

The classifications vary, but the two most common verticals are consumer staples and consumer discretionary; retailers are usually sub-groups within each one:

We will deviate from this slightly by counting retail as the third major vertical.

The trends and drivers are the same, but many key metrics differ, and some accounting/valuation points are different.

Here’s a quick explanation of each vertical:

- Consumer Staples: These companies make products that the average person uses with predictable frequency regardless of the economic environment. Consumption patterns tend to be recession-resistant and stable over time, and most products are “non-durable” (think: food, beverages, tobacco, skincare, home cleaning products, and anything else that lasts for less than 3 years).

- Consumer Discretionary: These firms produce goods that you “want but don’t necessarily need,” such as cars, home appliances, electronics, and luxury goods. Restaurants, travel services, homebuilding companies, and even apparel manufacturers (i.e., clothing companies) are also here. These firms are economically sensitive and highly correlated with consumer sentiment and disposable income.

- Retail: These companies act as distributors for the products above, and they live and die by their locations, store efficiency, inventory management, and margins. Offline retailers are increasingly moving online, but pure-play e-commerce companies are often classified within the Technology or TMT groups (with some exceptions – see below).

At first glance, these categories may not make sense.

For example, why are alcohol and tobacco companies considered “consumer staples” while car companies are “consumer discretionary”?

Doesn’t the average person need a car more than a bottle of whiskey or a box of cigars?

Yes, but the difference is that segments like alcohol and tobacco are not economically sensitive.

In other words, regardless of how the economy is doing, drinkers will keep drinking, and smokers will keep smoking.

But if there’s a recession, car sales will immediately fall as people start postponing their big-ticket purchases or making alternate plans (i.e., public transportation where it exists).

Recruiting into Consumer Retail Investment Banking

The consumer retail group is tied with the industrials group as the “generalist king,” which means there are no special entry requirements.

It’s the same IB recruitment process as always, which you should know from all the other articles on this site.

At the MBA level, a pre-MBA background at a consumer retail company helps, but this matching background is probably less important than in a more specialized industry, like energy.

One other note is that there are quite a few boutique banks that specialize in consumer retail or have significant exposure there.

Many of these markets are so fragmented with so many small companies and startups that there’s a big opportunity for boutiques to advise on deals.

Yes, the bulge brackets and elite boutiques dominate the biggest deals, but unlike a sector such as telecom, plenty of smaller deals still occur.

What Do You Do as an Analyst or Associate in Consumer Retail Investment Banking?

Your average day on the job depends on your bank, the size of the companies you advise, and your specific vertical.

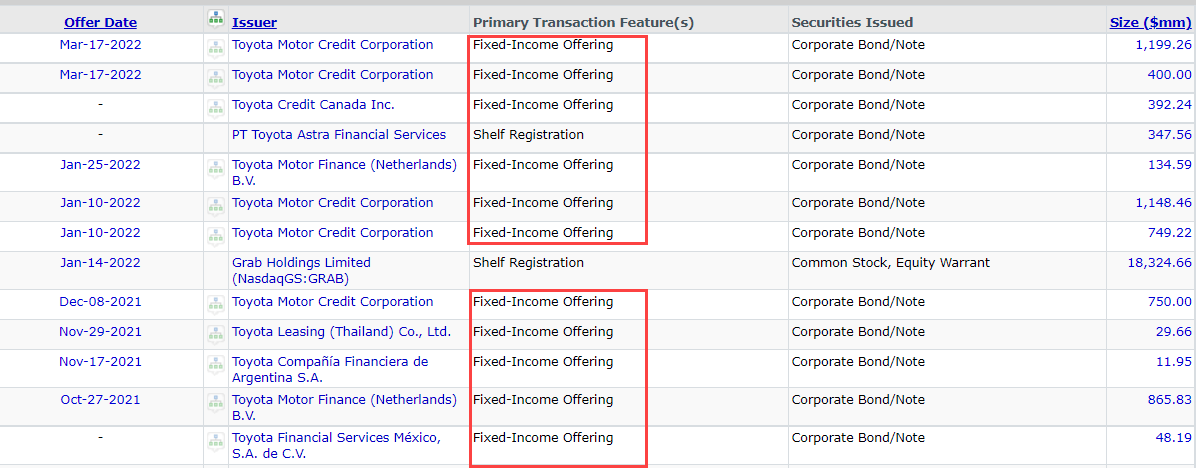

For example, if you work with the biggest companies in the auto vertical, such as Toyota, you’ll advise on a lot of debt issuances and occasional buy-side M&A deals.

These companies are constantly issuing debt:

Sell-side M&A and equity deals are more common if you’re working at a smaller bank that advises startups and other growth companies.

But deal flow is also very dependent on your vertical.

For example, I ran a screen for M&A deals with U.S.-based public sellers worth more than $100 million over the past 3 years and got the following deal counts (retail is not broken out separately):

- Consumer Discretionary: 26 / 31 (~84% of all M&A deals > $100 million)

- Consumer Staples: 5 / 31 (~16% of all M&A deals > $100 million)

M&A activity is heavily concentrated within consumer discretionary for a few reasons:

- Growth – No matter what you do, it’s hard to get consumers to spend more on items like bread, vegetables, or chicken. But if you invent a new luxury good or toy, it could catch on and become a trend.

- Industry Concentration – The consumer staples sector has already had waves of M&A activity that consolidated much of the industry. So, merger opportunities among the remaining companies are limited due to size and regulatory concerns (anti-trust).

Finally, if you work with a lot of offline retailers, expect a good number of restructuring deals as these companies figure out how to survive in the online world:

Consumer Retail Trends and Drivers

Trends and drivers are similar for the different verticals because many “staples” items were once considered “discretionary,” and overall economic growth, wage growth, and employment trends affect everything.

Also, sales of discretionary items – such as home appliances – influence the demand for staples items such as food and beverages.

Some of the key trends and drivers include:

- Personal Consumption Expenditures (PCE) – This represents the value of all goods and services purchased by normal people, and it’s more important on the discretionary side (though it can still affect staples by changing the pricing and product mix). The components include durable goods, non-durable goods, and services.

- Consumer Sentiment – This one is harder to quantify – though people have tried – but it represents how people view their financial prospects and living standards and how they might change in the future.

- Branding – It’s very difficult for many consumer staples companies to distinguish their products from similar products in the market (think: toothpaste or toilet paper). Therefore, brand power is essential if a company wants to avoid competing based purely on price.

- Demographics – Is the company’s target market growing, shrinking, aging, or getting younger? Is household formation up or down? Are people moving to the suburbs or the cities? All these factors influence the demand for specific consumer products.

- Income and Employment – Higher disposable income normally means higher consumer spending, which helps discretionary firms but makes less impact on staples (the same goes for the unemployment rate and wage growth).

- Inflation – Commodities and other raw materials are inputs to almost all consumer products, so when their prices increase, consumer companies may attempt to raise product prices as well. But in competitive markets with few barriers to entry, companies might not be able to pass on these price increases, which means margin pressure. Therefore, it’s important to look at the CPI and the PPI to measure inflation at both the retail and wholesale levels.

- Interest Rates – Many discretionary purchases are financed rather than paid for upfront (think: cars, homes, and even large home appliances), so higher interest rates tend to reduce demand and delay purchases, while lower rates have the opposite effect. Even within the staples sector, interest rates make an impact because some firms might be more capital-intensive or carry more inventory than others, which makes production more expensive when rates are higher.

- Currencies and Exchange Rates – Most large consumer companies operate globally, so fluctuating currencies affect everything from their input and labor costs to their revenue when selling goods abroad and translating sales back into their domestic currency.

These trends all affect retailers, but their impact depends on the retailer’s industry and business model.

For example, a specialty retailer like Home Depot is more sensitive to interest rates and demographics than a grocery store.

Lower interest rates and the migration of younger families into suburban and rural areas mean higher demand for homes and, therefore, for Home Depot’s products.

But most people do not “finance” their grocery purchases, so interest rates matter less, and the specific population profile matters less than the total population in an area.

Consumer Retail Overview by Vertical

Let’s go through this and mix it up with some bank and investor presentations along the way:

Consumer Staples

Representative Large-Cap, Global, Public Companies: Nestlé, Archer-Daniels-Midland, Pepsi, Proctor & Gamble, Wilmar, Bunge, Anheuser-Busch, Tyson Foods, Coca-Cola, Mondelez, Kraft Heinz, Altria, Estée Lauder, Kellogg, Conagra, Colgate-Palmolive, and Kao (Japan).

This list is dominated by food and beverage companies, which isn’t surprising since everyone needs to eat and drink to survive.

“Household and Personal Products” are also in this list (makeup, home cleaning, bathroom supplies, etc.), but they represent a much smaller percentage of the market.

When you analyze companies in this vertical, you focus on brand (reduced risk from competition), recurring revenue, the ability to diversify (geographically product-wise), and free cash flow generation.

Margins are crucial, especially for companies with lesser-known brands, and small pricing differences could explain why one company thrives and another fails.

Distribution and capital intensity are also important because companies here have different business models.

For example, Coke and Pepsi often trade at premiums to other food and beverage companies because they’re franchises and, therefore, have lower cost structures than companies that directly produce and distribute their products.

On the other hand, this franchise model could also turn into a weakness if the company overextends itself or fails to implement quality control with franchisees.

You might break down company performance based on shipments in different segments and analyze the revenue and cost structure for each one separately:

Consumer staples companies traditionally struggle to grow because they serve mature markets with stable consumption patterns, so it’s also critical to dig into the growth drivers:

- Pricing vs. volume?

- New/repurposed products?

- International expansion?

- Acquisitions?

Consumer Discretionary

Representative Large-Cap, Global, Public Companies: Toyota, Stellantis, Mercedes-Benz, Ford, GM, SAIC Motor, Nissan, Panasonic, Kia, Tesla, Renault, Midea (China), DENSO, Nike, Starbucks, McDonald’s, Whirlpool, Sharp, and Goodyear.

This list is dominated by automobile companies, which is no coincidence since they sell the highest-priced items here.

But the list also includes home appliance manufacturers, fashion companies, auto/other tool companies, and even restaurants (if you want to call Starbucks and McDonald’s “restaurants”).

In the auto sector, key drivers include economic growth, consumer sentiment, interest rates, technological advancements (e.g., the transition to hybrids and now electric vehicles (EVs)), and changes in raw material prices and currencies.

The industry tends to be heavily regulated, the barriers to entry are high due to the capital required to produce cars at scale, and inflation can make a very uneven impact.

For example, large car manufacturers may be able to “push back” against component price increases if they do enough business with certain suppliers.

But most auto component companies are smaller and less capitalized and could easily get squeezed due to inflation in raw material prices.

The replacement cycle also plays a major role since the market is mature in most developed countries; most growth comes from EVs and emerging markets earlier in the adoption cycle.

In segments like electronics (e.g., Panasonic and Sharp), R&D/innovation, consumer trends, and the supply and demand of specific components are major drivers.

Many companies in consumer discretionary are also highly dependent on retailers (see below).

For example, textile and apparel companies produce their goods based on retailer demand for inventory.

Finally, in sectors like leisure, travel, and restaurants, major drivers include personal income, consumer preferences, and geography.

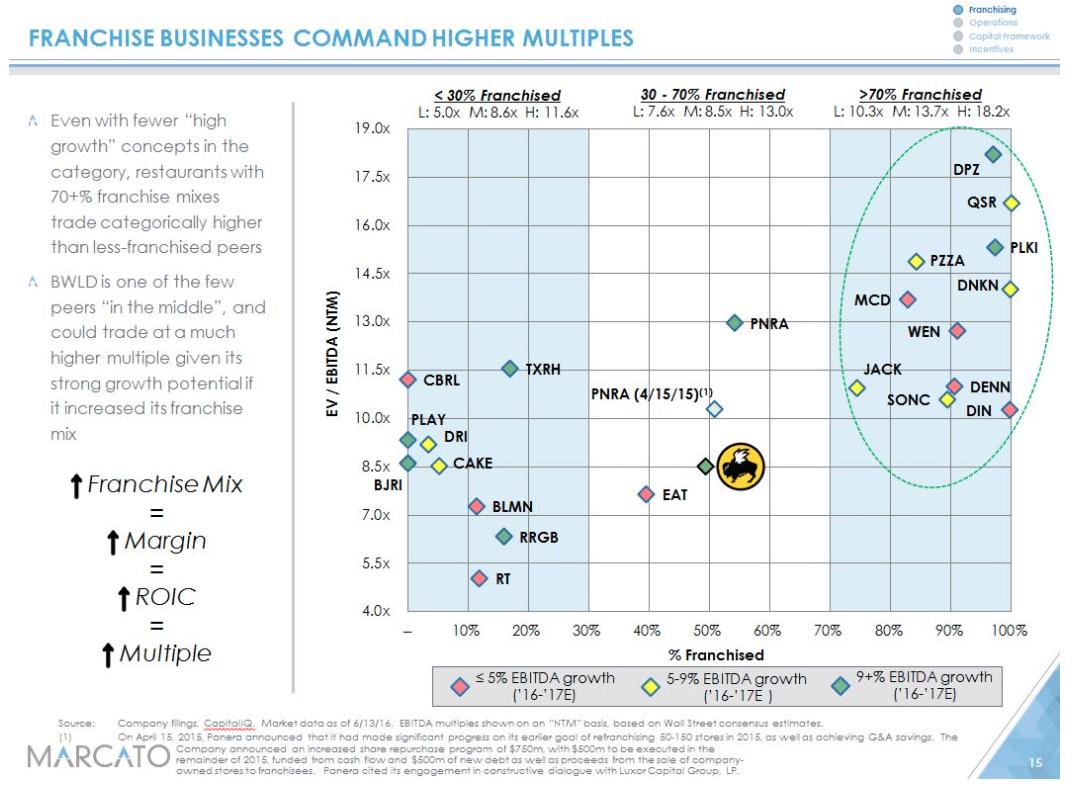

The business model – franchise vs. directly owned – also makes a big difference, and investors often push these companies to become franchise businesses in search of higher multiples:

Retail

Representative Large-Cap, Global, Public Companies: Walmart, Amazon (??), Costo, JD.com (??), Alibaba (??), Target, Wuchan Zhongda, Carrefour (Europe), Aeon (Japan), Sysco, Alimentation Couche-Tard (Canada), TJX, Woolworths (Australia), Loblaw (Canada), J Sainsbury (U.K.), AutoNation, Rite Aid, and AutoZone.

This list is more geographically diverse than the others, which makes sense since retail is a distribution business.

Even if products come from the same suppliers, different companies will spring up in different countries, states, and cities to distribute those products.

The key drivers for retailers are similar to those in the lists above.

If it’s a grocery or drugstore retailer, expect it to act more like a consumer staples company.

If it’s a car, electronics, or appliance retailer, expect more of a consumer discretionary company.

The main difference is that since most retailers do not make their products, they depend on factors such as:

- Location – Are the stores near population centers? What’s the nearby competition like? What’s the demographic profile of the area?

- Margins – Given the extremely high Cost of Goods Sold (COGS) for most retailers, even tiny differences in labor and administrative costs can explain companies’ relative success.

- Same-Store Sales – How have the stores that have been around for at least a year been performing? Is the company growing by improving its product mix, pricing, or foot traffic?

- Inventory – How many times is the company “turning over” its Inventory each year? How does that compare to peer companies, and how does it affect cash flow and the cash conversion cycle?

- Suppliers and Pricing Power – How does the company source its products? Does it have a diverse mix of suppliers, or is it dependent on a few firms? If there’s inflation, who absorbs the rising prices, and who passes them on?

These points are so critical for retailers that some activist investors create detailed analyses to suggest improvements in areas like margins:

Consumer Retail Accounting, Valuation, and Financial Modeling

There’s little to say here because consumer retail is the textbook example of a “standard sector.”

Accounting and 3-statement modeling are straightforward (think: Shipments * Average Selling Price or Sales per Location * # Locations), and valuation uses all the traditional multiples and methodologies, such as the DCF model.

If you want examples, take a look at a few from Goldman Sachs and Centerview:

The differences lie in the metrics and the increased importance of certain topics, such as lease accounting.

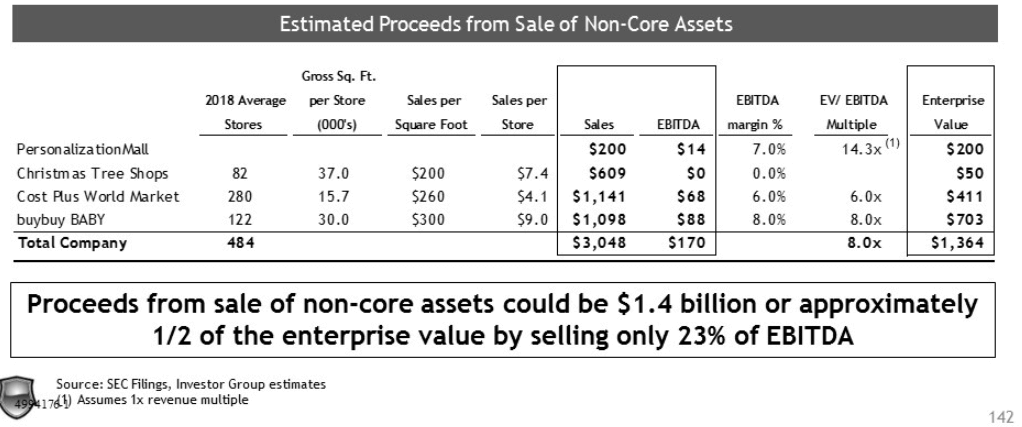

For example, you’ll see a lot of “per store” and “per square foot” metrics for retailers:

And lease accounting takes on increased importance because many consumer/retail companies have a mix of owned and leased properties.

If you don’t understand the differences, it will be difficult to normalize and compare different firms.

Example Valuations, Pitch Books, Fairness Opinions, and Investor Presentations

And now to the best part of any “industry group” article on this site:

Consumer Staples

British American Tobacco / Reynolds

Anheuser-Busch / Craft Brew Alliance

Cargill and Wayne Farms / Sanderson Farms

JAB Cosmetics / Coty

Consumer Discretionary

NASCAR / International Speedway Corporation

- DBO Partners – Fairness Opinion Presentation

- Fairness Opinion in Text

- BAML – Financial Analysis Presentation

Vintage Capital / Red Robin Gourmet Burgers (Cancelled LBO)

BBX Capital / Bluegreen Vacations (Cancelled Deal)

Betterware / DD3 (SPAC Deal in Mexico)

The Scotts Miracle-Gro Company / AeroGrow

Empire Resorts (Restructuring)

Kyocera / AVX Electronics

- Centerview – Deal Overview and Valuation Presentation

- Daiwa Securities – Valuation Analysis Presentation

Buffalo Wild Wings – Standalone Analysis

Retail

Stein Mart (Eventual Bankruptcy)

Sears Restructuring/Bankruptcy

Dufry / Hudson (Travel Retail M&A Deal)

Bed, Bath & Beyond – Standalone Analysis

Consumer Retail Investment Banking League Tables: The Top Firms

You’ll see most of the bulge brackets on consumer retail M&A deals; MS, GS, and BAML are particularly strong in equity issuances.

Other large banks such as JPM, Barclays, and Citi also advise on plenty of M&A and debt deals.

Among the elite boutiques, Centerview is the clear standout for advisory work on the biggest M&A deals in the sector, but the others all have strong practices in this area.

Solomon Partners, formerly known as PJ Solomon, also stands out for its work on notable consumer retail deals, but it’s not normally considered an “elite boutique.”

Among middle-market banks, Jefferies, Harris Williams, William Blair, Baird, and Lincoln International all stand out.

Firms like Piper Jaffray are often strong in specific verticals, like food & beverage and growth-oriented deals.

Among “non-elite” boutique banks, some well-known industry-specific firms are North Point Advisors, Sawaya Segalas (now owned by Canaccord Genuity), Telsey Advisory Group, and Financo (now owned by Raymond James).

And dozens (hundreds?) of other boutique banks have a strong presence in consumer retail, even if they do not specialize in it.

Consumer Retail Investment Banking Exit Opportunities

Since this sector is diverse, your exit opportunities are also quite broad.

If you want to position yourself for the private equity mega-funds, you could aim to work on large-cap M&A deals at a bulge bracket or elite boutique.

If you’re more interested in venture capital, you could advise EV companies on their plans for world domination.

And if you want to work in the distressed, restructuring, or turnaround space, you could advise troubled offline retailers.

Plenty of hedge funds are active in the space, and you’ll see strategies ranging from merger arbitrage to long/short equity to activist/turnaround to credit.

Corporate development and corporate finance are viable paths, as is staying in banking to advance up the ladder.

The only real “downside” to exit opportunities is that you may not be the best candidate for every role.

For example, if you recruit for VC, you’ll be at a slight disadvantage next to someone who worked in the tech, healthcare, or TMT groups.

For Further Reading

Some good information sources include:

- News: Retail Dive, FT Retail & Consumer, Retail Gazette, Retail Week, and WSJ Retail News

- Industry Research: Deloitte, KPMG, PwC, E&Y, and Fitch

- Books: Fisher Investments on Consumer Staples and Fisher Investments on Consumer Discretionary

Is the Consumer Retail Investment Banking Group Right for You?

Since consumer retail investment banking spans a wide range of industries and gives you exposure to all deal types, it’s hard to point to any real downsides.

You won’t get pigeonholed by working in the group, and although some verticals within it are economically sensitive, plenty of others are not.

Therefore, even if deal activity in one area falls off a cliff, you could become busier by moving to another team within the group.

The main downside is that banks are strong in different verticals, and there isn’t necessarily a way to discern your group’s strengths before you sign an offer.

So, don’t join the consumer retail group expecting that you’ll instantly become an adviser to EV companies and buddies with Elon Musk.

You could easily end up advising discount retailers or toilet paper companies.

And you’ll be a great generalist, but you might not feel like a king.

Want More?

You might be interested in Investment Banking League Tables: Neutral Arbiter of Bank Rankings or Marketing Manipulation?

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Hi Brian,

Can you provide thoughts on the C&R group as well as the general investment banking arm at Wells Fargo?

Thanks!

Wells Fargo is strong in debt and industries that do a lot of debt issuances and less strong elsewhere. You’re unlikely to get into one of the biggest PE funds from there, but plenty of people move to mid-sized firms, especially from stronger groups (industrials). I don’t know how strong they’re consumer/retail group is, specifically, but I assume at least fairly good given the number of companies in that sector issuing debt all the time.

Hello Brian,

Currently, how would you compare UBS FIG and CP&R? I am currently in the group placement process for SA.

Thank you,

AS

I don’t have a strong view on either of these groups, but FIG, as usual, is highly specialized and rarely worth it unless you want to work in FIG long-term. So, for 90%+ of people, CP&R is a better bet, even if the specific bank happens to be stronger in FIG.