Technology Investment Banking: Take Over the World with Zero Earnings and Negative Cash Flows?

- Investment Banking Industry Groups: Technology

- “TMT” vs. Technology Investment Banking

- Recruiting: How to Bootstrap Your Way into Tech IB

- What Do Analysts and Associates in Technology Investment Banking Do?

- Technology Trends and Drivers

- Sub-Sectors within Technology Investment Banking

- Technology Valuation and Financial Modeling

- Technology Investment Banking League Tables: The Top Banks

- Technology Investment Banking Exit Opportunities

- Is Technology the Best Group? Will Tech Continue to Conquer the World?

- For Further Reading

- Pros and Cons of Technology Investment Banking

- Want More?

Study enough history, and you’ll soon realize that not all companies exist to make a profit.

Many exist to change social behavior, or to create an “empire” for their government/military backers (e.g., the East India Company).

Technology investment banking often serves companies in one of these categories.

Many tech companies are not necessarily aiming for profits, but they are trying to “make the world a better place” – or at least, alter social behavior to their liking.

Just look at Uber: it may never generate positive cash flows, but it made some of its early backers wealthy while screwing over its poor drivers.

Increased income and wealth inequality: achievement unlocked!

In addition to poking fun at SoftBank-backed startups, we’ll also take a look at the following points in this industry overview:

- The main sub-industries within and around technology, including technology vs. TMT investment banking.

- How deals, financial modeling, and valuation are different.

- What investor presentations, valuations, and Fairness Opinions look like.

- The top banks in the sector and exit opportunities.

- Overall pros and cons of the group, including whether or not “Big Tech” will be more valuable than all human + extraterrestrial civilizations by 2050.

Investment Banking Industry Groups: Technology

Technology Investment Banking Definition: In technology IB, bankers advise companies in the software, internet, hardware/equipment, semiconductors, and IT services markets on mergers, acquisitions, and debt and equity issuances.

Technology is the textbook example of an industry group within investment banking, which means that professionals in the group work on all types of deals, but only within a single industry.

Each vertical in tech is a bit different, but most companies fall into one of two categories:

- Earlier-Stage / Growth-Oriented – These firms include venture-backed tech startups as well as small and mid-cap companies that want to raise capital, grow, and eventually sell to a larger company or go public.

- Mature – These include many of the largest, global, public companies with tens of billions in revenue; they frequently acquire smaller companies to enter new markets and keep innovating.

At smaller banks, you’ll be working with companies in category #1 more often, which makes sell-side M&A deals and equity issuances more common.

At larger banks, companies in category #2 are more common, so expect to see more buy-side M&A deals, leveraged buyouts, and debt issuances to support those deals.

In terms of geography, the U.S. has the most highly valued tech companies (Apple, Microsoft, Amazon, Alphabet [Google], and Facebook), while China is in second place with Alibaba and Tencent.

Other Asian countries, such as South Korea, Taiwan, and Japan, also rank prominently due to hardware and semiconductor companies based there.

Europe noticeably lacks large-cap, public tech companies, but it does have a few big names, such as SAP in Germany and Spotify in Sweden.

“TMT” vs. Technology Investment Banking

Some banks have dedicated Technology groups, while others put it within the “Technology, Media & Telecom” (TMT) group.

TMT is much broader because it also includes companies like AT&T, Verizon, Softbank, China Telecom, Deutsche Telekom, etc., as well as media companies such as Disney, Vivendi, and ViacomCBS.

Traditionally, media companies produce content, telecom companies offer delivery services for content, and technology companies provide software, hardware, and services for the consumption of content (as well as for non-content-related business/personal tasks).

Increasingly, however, there’s a convergence between companies in the TMT sector.

For example, is Netflix a “technology” company or a “media” company?

I would argue that it began as a technology company, but it has increasingly turned into a media company due to its shift to original content production (Benedict Evans agrees).

In this article, we’ll focus on technology companies (see our separate coverage of media and telecom investment banking).

Recruiting: How to Bootstrap Your Way into Tech IB

Technology IB is not highly specialized in terms of accounting, valuation, or financial modeling, and it also doesn’t require detailed legal knowledge (unlike restructuring).

Having an engineering or computer science background and experience working at tech companies helps, but it is not necessary to get in.

An advanced degree might help in a few areas that are more technical, such as semiconductors, but you don’t need the degree to understand most companies.

Investment banks follow the standard recruitment process for undergrads and MBAs, where the quality of your program, your grades, your work experience, and your networking efforts make the biggest impact.

One difference compared with other sectors is that there are dozens, if not hundreds, of tech-focused boutique banks.

That’s because there are always startups and smaller companies in search of funding, and investors are always looking for the next big thing.

These tech-focused boutiques can be a good entry point into the industry – but you don’t necessarily want to work there full-time because you may not get the deal or modeling experience you want.

What Do Analysts and Associates in Technology Investment Banking Do?

As always, your work will be based on pitch books, deals, and “random tasks.”

However, your vertical and the types of companies you work with will make the biggest difference in your day-to-day activities.

For example, if you’re at a boutique bank that raises funding for early-stage software and internet companies, expect to work on a lot of boring private placements.

There’s little modeling or valuation work, and while you will learn about the market, you won’t gain skills that are especially useful for most exit opportunities.

On the other hand, if you’re in the TMT group of a bulge bracket bank, expect to work on a lot of M&A deals and leveraged buyouts involving mature companies, with the occasional debt or convertible bond issuance.

These deals are more interesting initially, but by the time you’ve run 253 slightly different merger models, you may get tired of them as well.

The IT services, semiconductors, and hardware sectors tend to be more mature, so you’ll focus more on concepts such as profitability and cash flows there.

But if you work in internet and software, you’ll encounter a wide range of companies, ranging from mature-and-profitable firms to early-stage companies bleeding money.

Technology Trends and Drivers

A few key drivers that apply to all the verticals within technology include:

- Innovation and Upgrade Cycles – When Apple first introduced the iPhone, no one had seen a device quite like it before. Sales soared, and hundreds of millions of new customers eventually bought the device. But then smartphone innovation slowed down, and it became more of a “replacement market” rather than a “must buy this amazing new gadget” market.

- (Dis)inflation and Pricing Power – Most tech products naturally fall in price over time as manufacturing processes become more efficient and the cost of raw materials falls. Therefore, high inflation tends to disadvantage many tech companies because they don’t necessarily have the pricing power to keep up; firms must constantly improve their products and services to maintain their profit margins, which is easier with low inflation.

- Geopolitics and “National Security” – Traditionally, technology has not been a heavily regulated sector, but that is starting to change as countries view it as vital to their national security. Cold War 2.0 between the U.S. and China has made a major impact on all tech firms, and the China vs. India conflict, with India banning dozens of Chinese apps, is heightening tensions.

- Broader Economic Conditions and Personal/Business Spending – Technology is usually viewed as a “highly sensitive” sector with a high Beta. It performs well when unemployment is low, disposable income is rising, and businesses have more cash to spend on servers, software, and devices. And when budgets fall due to a recession, IT spending is often the first area to be cut (do you need a new computer right now?).

- Tax, Trade, IP, and Fiscal Policy – How well does a country protect intellectual property rights? If enforcement is poor, software companies will struggle due to piracy. Does the country’s tax policy favor large companies, small businesses, individuals, or government-owned entities? Does the country discourage imports with tariffs, or does it encourage free trade? Tech supply chains are global, so all these policies make a difference.

Sub-Sectors within Technology Investment Banking

Large banks break up their tech and TMT groups in countless different ways; you’ll see everything from 15 different sub-groups to only 3-4.

However, we’re going to stick with the split above – Software, Internet, Hardware & Equipment, Semiconductors, and IT Services – because it’s easiest to explain the companies and sector drivers that way.

Software

Representative Large-Cap Public Companies: Microsoft, Oracle, SAP, Salesforce, Adobe, VMware, and Intuit.

There are surprisingly few large, pure-play software companies worldwide, at least if you judge “size” based on revenue.

That’s partially because of consolidation in the sector by companies like Oracle, but it’s also because most large companies in this space sell primarily to enterprises, not consumers (gaming companies like Nintendo and EA are sometimes classified under “media” instead).

Enterprise accounts take a lot of effort to win, but they tend to be “sticky” once the sale is made, which gives a big advantage to the large, entrenched players.

A long time ago, software companies used to sell an initial license priced based on the number of “seats” at the company and then charge for support and maintenance each year (which was often 15-20% of the initial license fee).

But companies have moved to the Software as a Service (SaaS) model, where customers pay a monthly or annual subscription fee to use software delivered remotely.

Customers pay less upfront and don’t have to worry about their local installations, and companies gain more revenue visibility.

That business model shift has also affected accounting and financial modeling for software companies, and you need to be familiar with metrics like CAC (Customer Acquisition Costs), LTV (Lifetime Value), Churn, Billings, and Unearned Revenue to do proper analysis.

To learn more, see a16z’s guides to SaaS valuation and key metrics.

Internet

Representative Large-Cap Public Companies: Amazon, Alphabet (Google), JD.com, Facebook, Tencent, Alibaba, Baidu, Rakuten, and Netflix (???).

“Internet companies” do everything from social networking to e-commerce (either via marketplaces or direct from companies to consumers) to search engines to all-powerful mobile apps (e.g., WeChat).

Drivers here include user growth, Monthly Active Users (MAUs), and Average Revenue per User (ARPU).

Social-media companies like Facebook depend heavily on advertising revenue, but others may rely on in-app user purchases and microtransactions.

For marketplace companies (Alibaba), gross merchandise value (GMV), which represents the total sales volume of all transactions on the site over a specific period, is critical.

For direct internet retailers that own physical inventory, like Amazon, traditional metrics like Gross Margin and Days Inventory Outstanding are important because margins tend to be thin.

Finally, subscription-based companies like Netflix depend on user growth, price increases, and content expansion to grow. They try to keep their churn (cancellation rate) as low as possible, which is always a challenge with a consumer product.

Hardware & Equipment

Representative Large-Cap Public Companies: Apple, Samsung, Hon Hai Precision Industry (Foxconn), Huawei, Dell, Hitachi, HP, Lenovo, Cisco, Pegatron, and Xiaomi.

Note the geographic split: names from the U.S., China, Taiwan, Japan, and South Korea are all on this list.

Unlike most software and internet companies, hardware companies must spend a huge amount on CapEx to build factories and manufacture their products.

This makes them more similar to industrials companies in some ways, so traditional metrics like gross margins and cash flows matter a lot.

Some of these firms are consumer-focused (Apple and Dell), while others provide manufacturing services for other companies (Foxconn), and others provide a mix of services and consumer and business products.

Supply chains and manufacturing efficiency are critical for companies in this sector, as are sales channels (direct vs. distributors vs. retail).

Since many of these hardware markets have matured over time (smartphones, tablets, PCs, and laptops), companies have been trying to earn revenue from additional sources, such as apps and subscription services (see: Apple).

Semiconductors

Representative Large-Cap Public Companies: Intel, Taiwan Semiconductor Manufacturing Company (TSMC), Micron, Qualcomm, SK hynix, Broadcom, NXP Semiconductors, Applied Materials, Texas Instruments, ASE, ASML, and Nvidia.

Finally! A few European names (NXP and ASML) make the list.

If hardware companies assemble “devices,” semiconductor companies make the insides of those devices: chips such as CPUs, memory (RAM), and graphics cards.

Like hardware companies, many semiconductors companies tend to be CapEx-intensive, but they also have high research & development costs.

Business models span a wide range, with the traditional, vertically integrated model as one option, but also “fabless” and “fablite” models.

“Fabless” companies outsource their manufacturing to third parties to reduce their expenses and upfront capital costs, while “fablite” companies mix the two models and outsource only some of their manufacturing to reduce costs while maintaining quality.

The semiconductor industry is highly cyclical, even more so than other verticals within tech.

News of a new operating system or smartphone can spike chip demand, but if companies respond with too much of a production increase, prices can plummet – especially if demand turns out to be lower than expected.

Key metrics include the book-to-bill ratio (orders received / orders shipped) and capacity utilization, which can tell you where a company is in the cycle.

IT Services

Representative Large-Cap Public Companies: IBM, Accenture, Fujitsu, NEC, Visa, NTT Data, Tata Consultancy, DXC Technology, PayPal, MasterCard, Cognizant, Automatic Data Processing (ADP), Capgemini, Infosys, and Fiserv.

Look, another European name (Capgemini)! Also, two Indian companies (Tata and Infosys) make this list.

“Wait a minute,” you say, “Why are Visa, PayPal, and MasterCard also on this list? What?!”

They’re all in the “Data Processing & Outsourced Services” category, which is one of the two major verticals in IT Services, along with “IT Consulting & Other Services.”

Yes, they’re arguably more like financial services companies, but they also depend heavily on technology.

Companies in the “IT Consulting” category do not sell software, hardware, or content: instead, they provide services to set up or maintain custom systems for clients.

Key drivers include business spending and the ease or difficulty of outsourcing/offshoring.

In the Data Processing segment, key drivers include employment levels (for companies like ADP that do payroll processing) and overall consumer spending for companies like PayPal and Visa.

Technology Valuation and Financial Modeling

There are no huge accounting or valuation differences in technology, and you still use standard methodologies such as the DCF, comparable company analysis, precedent transactions, accretion/dilution, and LBO models.

However, some of the metrics and nuances are different.

For example, you need to know about deferred revenue, billings, and revenue recognition if you’re modeling a SaaS company like Atlassian:

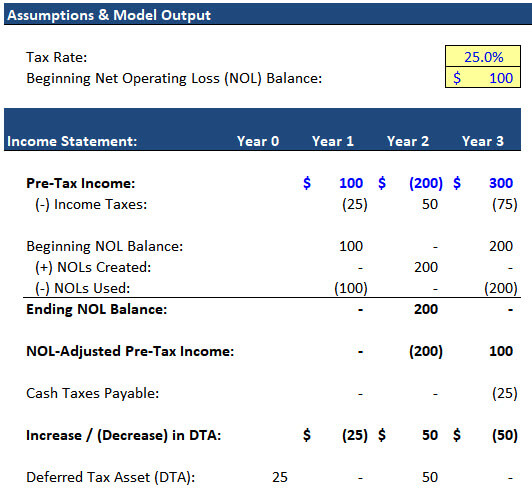

Many tech companies have significant Net Operating Loss (NOL) balances, so you’ll also have to be familiar with how they work, and how they interact with book taxes, cash taxes, and deferred taxes on the financial statements:

Something like Section 382 for the treatment of NOLs in M&A deals is unlikely to come up, but it could if you have more significant deal experience.

Many tech companies also have convertible bonds, so you need to know something about the accounting and valuation for those instruments as well.

We cover these topics in our Advanced Financial Modeling course, which includes a convertible bond case study based on Netflix:

Advanced Financial Modeling

Learn more complex "on the job" investment banking models and complete private equity, hedge fund, and credit case studies to win buy-side job offers.

learn moreOn the hardware side, it also includes a bonus case study based on Dell.

If you want to see a few examples of valuations, Fairness Opinions, and investor presentations, please take a look at these:

Software

IBM / Red Hat – Guggenheim and Morgan Stanley

Salesforce / Tableau – Goldman Sachs

Ultimate Software (Leveraged Buyout by Hellman & Friedman) – Goldman Sachs

Internet

Microsoft / LinkedIn – Qatalyst Partners

Shutterfly (Leveraged Buyout by Apollo) – Morgan Stanley

Hardware & Equipment

Cisco / Acacia – Goldman Sachs

Xerox / HP (Cancelled) – Guggenheim, Goldman Sachs, and Citi

Semiconductors

Infineon / Cypress Semiconductor – Morgan Stanley

Nvidia / Mellanox – JP Morgan and Credit Suisse

IT Services

Fidelity National Information Services / Worldpay – Centerview, Goldman Sachs, and Credit Suisse

Fiserv / First Data – JP Morgan, BAML, and Evercore

Technology Investment Banking League Tables: The Top Banks

All the bulge brackets have strong tech/TMT teams, but traditionally, Goldman Sachs and Morgan Stanley are known as “the best” (highly subjective).

As you can see from the transactions above, though, plenty of other large banks advise on tech mega-deals: JPM, BAML, Citi, CS, and more.

Among the middle market banks, the usual suspects all have strength in tech: Harris Williams, William Blair, Jefferies, Raymond James, etc.

The elite boutiques also do well in tech, and Qatalyst is probably the leader since it’s the only one that specializes in the industry.

But Evercore, Lazard, Guggenheim, Centerview, and Moelis also pop up on many deals.

There are also dozens, if not hundreds, of boutique banks in the space since technology comprises such a high percentage of overall deal flow.

I’m not sure how to classify Allen & Co., but it should be on this list somewhere as well (maybe more in the “media” category?).

Other names include Union Square Advisors, GCA, CODE Advisors, Raine Group (more of a merchant bank), FT Partners (fintech), Marlin & Associates, Arma Partners, and GP Bullhound.

Yes, there are many others; feel free to suggest other names in the comments.

Technology Investment Banking Exit Opportunities

Similar to healthcare IB, exit opportunities in tech are quite good because you work on many different deal types and do not specialize in obscure accounting and valuation.

All the standard exits are open to you: private equity, venture capital, growth equity, hedge funds, corporate finance, and corporate development.

That said, you’ll only be competitive for some of those if you’ve worked at a larger bank.

For example, no matter how great your deal experience, it’s highly unlikely that you’ll move from a regional boutique bank into tech private equity at Blackstone.

But venture capital, growth equity, or even a smaller PE firm, are more realistic.

Growth equity is so dominated by technology firms that you could almost view that as a separate/additional exit opportunity (think: Summit Partners, TA Associates, TCV, Accel-KKR, Vista Equity, and Vector Capital).

Is Technology the Best Group? Will Tech Continue to Conquer the World?

Over the past decade, the big tech companies have dominated the U.S. and global stock markets.

But tech was also quite dominant in the 1990s, and we all know how that story ended:

The most highly valued companies don’t necessarily “crash and burn,” but the global pecking order changes each decade.

So, it’s highly unlikely that Microsoft, Apple, Amazon, Google, and Facebook will still be the top companies in the world by market cap in 2030 (well, except for Microsoft: it always seems to be in the top 10).

Calls for regulation and “breaking up big tech” will gain traction, especially as politicians on all sides now hate the industry.

Another possibility is that a different industry could displace tech, especially if this turns out to be the biotech century.

I don’t think big tech will ever “die,” but it will become less dominant in terms of market cap and deal activity in the future.

For Further Reading

Good industry sources include:

- News: TechCrunch | Red Herring | Wired | TechNode | TechInAsia

- Mainstream News: FT | WSJ | NYT

- Industry Reports: Baird’s Technology & Services Reports

- Industry Reports from Big 4 Firms: PwC, Deloitte, and KPMG

- Industry Reports from GCA Global: Insights on all sectors within technology

- Books: Fisher Investments on Technology

Pros and Cons of Technology Investment Banking

I’d sum up everything above as follows:

Pros:

- You’ll work on a variety of deals across different sectors, at least at mid-sized and larger banks, though there are relatively fewer debt deals and more M&A and equity ones.

- You’ll gain skills that apply to many industries, so the exit opportunities are good – and you could easily move to another group at your bank.

- Depending on your vertical focus, you could position yourself well for PE, HF, VC, or CD roles.

- Tech has some of the highest deal flow and most active acquirers in the market. The big companies have so much cash that they need to spend it on something, which is where you, the banker, can come in with suggestions.

Cons:

- You could get stuck working on lots of boring private placement and sell-side M&A deals at smaller, tech-focused banks.

- The sector is extremely sensitive to economic conditions, and even the big tech companies can stumble in certain types of recessions.

That’s a short list of cons and a longer list of pros.

I don’t think technology will dominate the financial markets forever, but you can’t go wrong with the technology group in investment banking.

At the very least, you’ll generate a lot more cash flow, personally, than many of the companies you advise.

Want More?

You might be interested in Investment Banking League Tables: Neutral Arbiter of Bank Rankings or Marketing Manipulation?

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Hi Brian, what do you think about Rothschild’s tech team?

I don’t have a strong view, sorry. I usually only look at bank rankings by sector when writing or updating one of these industry-specific articles, and I haven’t looked at tech/TMT in a few years. Rothschild is a good firm overall, though definitely stronger in Europe/EMEA.

I go to a Top 3 MBA school and am considering between these two firms – Lazard SF Tech, Bank of America Palo Alto (either Tech coverage, or Tech M&A). Which would you think is a better fit if I want to move to a large or middle-market PE firm, or move to corp dev role.

For PE, probably about the same. For corp dev, Bank of America is better because it’s more widely recognized outside the finance industry. So on balance, I would probably pick BoA. Lazard might be better for banking long-term.

Can software engineers/tech-related roles break into Tech IB after their MBA? I am currently at a FAANG company and wanted to see if this type of transition is possible post mba.

Yes, potentially, but you usually need some kind of pre-MBA internship or other business-related experience to have the best shot. Otherwise, you’re up against too many former bankers and people with more relevant finance experience. The FAANG brand helps for sure, but you’re still going to be perceived as a career changer.

Hi Brian, thanks for all of the content you produce. Really enjoy reading your posts.

On the topic of IB groups, do you have a view on the generalist experience versus working in specific industry groups? Or even working with a specific set of senior bankers versus working with a broader mix?

I understand that there are pros and cons to each, and that experiences will differ across banks and people. Thanks!

I don’t think it matters that much, but you do benefit from being in certain groups for certain exit opportunities. For example, recruiters are always going to approach people in groups like GS TMT and MS M&A for the top PE roles first. But if you want to stay in banking, this point doesn’t matter, and you should just pick whichever group you like. I don’t think you can really be a generalist forever, though, as senior bankers are all in specific groups, so you’ll have to decide on something eventually.

Hi Brian. I was wondering if you could rank some of the top tech investment banking groups at the major banks. I am aware that GS, MS and Q dominate the space but was wondering what comes next?

We don’t do rankings here. You can find recent league tables in source like the one below:

https://www.globaldata.com/jp-morgan-leads-globaldatas-top-10-global-ma-financial-advisers-league-table-in-ict-sector-in-2019/

Hi Brian. I just received an offer from the technology IB group at Jefferies in NYC. I was just wondering your overall opinion of this group for exits and if you think it’s worth it to lateral and to where?

If you’ve received a solid job offer in the current environment, you should accept it and ask questions later. It’s a good group that has worked on increasingly larger deals over time, but you’re not going to get into KKR or Blackstone from there if that’s your goal. Of course, the vast majority of Analysts at BB/EB banks will also not get into one of those firms.

This was a great write up, thanks for the insight. Starting at a top MBA program this fall with the goal of recruiting for tech IB, and there’s not much info out there besides your blog and WSO, so thank you for sharing. For someone interested in Growth Equity post-MBA, how many years of BB banking xp in the Bay area would you recommend getting before looking to transition?

You should aim to move as soon as possible, so ideally within 1-2 years. Exit opportunities are already more difficult as an Associate, and the longer you stay in the role, the harder it gets to move elsewhere.

Hello Brian, what do you think of TMT in Hong Kong – with all the deals from China, is it a good group to enter? If not, what industry groups are the best bet from your perspective? Thanks!

Sure, if you can actually work in HK. Other good industries are natural resources, real estate, construction/infrastructure, and consumer/retail. But it just depends on what you want to do and where you want to work. These days, most expat bankers are fleeing HK, so it will probably be 99% Chinese in the future.

How do these groups fare in recessions? Massive layoffs at the ANL/AS levels?

Depends heavily on the type of recession. If it’s driven by an actual economic/financial collapse (2008), then yes, there will be layoffs because all activity slows, companies stop spending on IT, etc. But in the current pandemic-driven recession, these groups have fared better because the quarantine, work from home, etc., have all benefited tech companies. Just look at the FAANG market cap since this started.

Technology is one of the more economically sensitive sectors, though, so you should not go in expecting a lot of stability.

Hi Brian, Thanks for the links, very useful.

I would include GP Bullhound as a leading advisor in this industry.

Plus, if I may, for IT Services companies it is one of the few industries in which you will never encounter much asset as they only employ people. Also their EBIT and EBITDA are essentially the same. Valuations are straight forward.

Thanks, I’ve added GP Bullhound.

Hi Brian, you mention Europe lacks large-cap public tech companies. I would guess this is not likely to change. Therefore, would you agree tech is not the most attractive group to get into in Europe going forward? Would you say the same about TMT?

Yes, tech is probably not the best group in Europe, though tech deals do still take place there. They just involve smaller companies. It’s better for media and telecom because there are relatively bigger companies in those sectors.

How do smaller players like Stifel, KeyBanc, Deloitte fit in to the tech IB picture?

They also work on deals – just smaller ones than the BB and EB banks. Some may also focus on slightly different deal types – for example, it looks like KeyBanc has advised on debt and equity issuances rather than M&A.

Hi Brian, for large banks that have multiple offices (ex Goldman in NY and SF), is their West Coast, specifically SF office typically more active in tech than their NY office?

Yes, SF tends to be more active in tech, and NY is more active in media/telecom.