The Elite Boutique Investment Banks: The Rising Upstarts That Disrupted the Old Guard?

If you received a job offer at Goldman Sachs or Morgan Stanley, would you be crazy to turn it down?

For many years, the answer would have been “yes” – especially if you turned it down to work at a smaller bank.

But in the aftermath of the 2008 financial crisis, that began to change.

Big tech companies and startups weren’t pulling students away – not yet, anyway – but rather other investment banks.

These firms were smaller, they ran leaner deal teams, and they focused on M&A and Restructuring, often advising on the same deals as the bulge brackets.

And they came to be known as the elite boutique investment banks (EBs).

The list, which I’m NOT ranking, but instead displaying in alphabetical order, looks like this:

What Is An Elite Boutique Investment Bank?

Definition: An elite boutique investment bank (EB) is a non-full-service firm that focuses on M&A Advisory or Restructuring, rather than capital markets, and that advises on the same types and sizes of deals as the bulge bracket banks – often with an industry or geographic specialty.

The name came from the fact that the EBs often advise on deals that are as big as the ones the bulge brackets work on (e.g., over $1 billion USD up to the tens of billions USD).

They “punch above their weight class,” so they’re labeled “elite.”

The difference is that they do not provide the same types of financing services, via equity capital markets, debt capital markets, and leveraged finance, that the bulge brackets do.

Also, the elite boutiques often focus on specific industries or regions and may not have the same strength elsewhere.

In an interview, it might sound a little weird if you say “elite boutique” aloud, so you should probably refer to them as “independents” or “independent investment banks.”

Wait, What About the Rankings? Rank the Banks!

I’m deliberately not ranking these firms or creating my own Elite Boutique Investment Bank League Table for a few reasons.

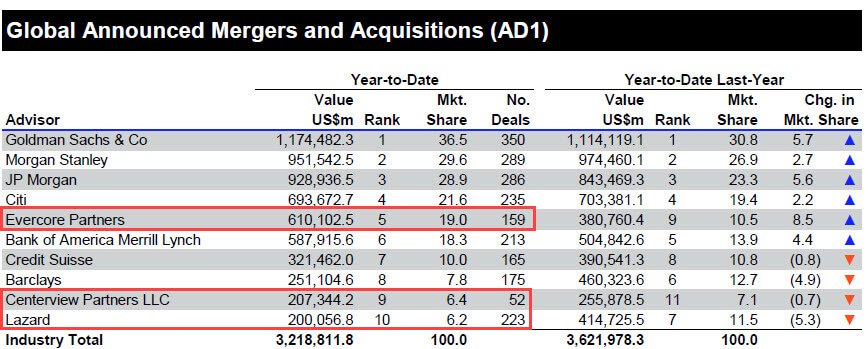

First, the volatility is quite high. Some of the elite boutiques advise on similar dollar volumes of M&A deals as the bulge brackets, but they tend to advise on fewer total deals:

Also, group and location matter more.

For example, the M&A and Restructuring groups at these firms are often viewed as “the best” teams, with standard industry groups not faring as well.

By contrast, a strong industry group at a bulge bracket bank isn’t much different from a strong M&A team at the same bank (see: product groups vs. industry groups).

Finally, there’s some controversy over which banks qualify as “elite boutiques” (see below).

What About Allen & Co.? LionTree? Should Qatalyst, Guggenheim, and Greenhill Be There?

The short answer to all these questions is maybe, maybe not.

Looking at the M&A league table data over the past 5-10 years, the elite boutique firms that most consistently place in the top ~10 worldwide are Evercore, Lazard, and Centerview.

After those, Rothschild (mostly due to Europe) is also quite consistent.

And then things get very random.

For example, in some years, newer firms like Moelis and Qatalyst have placed higher than some of the bulge brackets, while in other years, they did not make the top 20.

Firms such as Greenhill and Perella Weinberg rarely rank well by total deal volume, even if they advise on individual deals that are quite large.

The bottom line is that there isn’t a clear, universal dividing line between “elite boutiques” and “non-elite boutiques.”

However, I will make three quick comments about the classifications/rankings:

- Some firms are too new to judge. LionTree, Robey Warshaw, Dyal Co, and a few others fall into this category. Yes, they’ve advised on some massive deals, but they also haven’t been around for that long. I eliminated firms that have not been around for at least 10 years (since 2010). PJT is an exception since it was spun off from Blackstone.

- Middle Market and Other Full-Service Banks are not Elite Boutiques. This explains why firms like Wells Fargo, RBC, HSBC, Jefferies, Houlihan Lokey, Harris Williams, etc. are not on this list.

- Consistency and Exits Matter. This one explains why I did not include Allen & Co. in the list: they’ve fluctuated quite a bit over the years, and it seems like exit opportunities are not on par with some of the other banks here.

Before you leave an angry comment wondering why your bank was not included, I’ll reiterate that this list is subjective and likely to change in the future.

Outside of Evercore, Lazard, and Centerview, you could make a case against any of the others on this list counting as “elite boutiques,” and you could also argue for the inclusion of other banks not on this list.

Elite Boutique vs. Bulge Bracket, Middle Market, and Regional Boutique Banks

For the full set of differences, please see our article on the top investment banks.

In short, the elite boutiques tend to work on larger deals than middle market firms and regional boutiques, with transaction values often above $1 billion USD.

They often compete with and advise alongside the bulge brackets on deals in that size range.

It’s also easier to use the on-cycle recruiting process to move into private equity or hedge funds coming from an EB since headhunters will contact you directly.

Unlike the bulge brackets, the elite boutiques do not do much equity/debt financing work, and they are not well-known outside the finance industry.

Why Work at an Elite Boutique Investment Bank?

Assuming that you have a competitive profile for elite boutique and bulge bracket banks – more on that here – then many people argue that EBs offer the following advantages:

- Better / More Interesting Deal Experience: Since deal teams are smaller, you’ll have more responsibilities, and you’ll complete more technical work that requires thinking instead of boring administrative tasks.

- Better Culture: Yes, the hours and work/life balance are still bad, but you’ll be treated like a human rather than another cog in the machine. Smaller team sizes also mean fewer fire drills ordered from above.

- Great Exit Opportunities: You’ll be just as competitive for private equity and hedge fund roles, as well as most other jobs at dedicated finance firms.

- Higher Cash Compensation Than the Bulge Brackets: Many EBs pay higher bonuses to junior bankers, and they offer 100% cash compensation to senior bankers – unlike the bulge brackets, where significant percentages are paid in stock or deferred.

- Better Place to Build a Long-Term Career: You can focus more on building client relationships and less on office politics, you’ll be more independent, and you can work with a smaller group of highly driven and capable people who want to be there – not ones who want to leave as soon as a better job offer arrives.

These are the typical claims – but how well do they stack up to reality?

Why Not Work at an Elite Boutique Investment Bank?

First, there are the obvious downsides: the elite boutiques are not well-known outside the finance industry, so your exit opportunities to normal companies, startups, government roles, etc. will be reduced.

Also, you won’t get an “alumni network” of the same depth or breadth that you would at a BB bank.

Then there are some less obvious downsides that people tend to gloss over.

For one thing, the average deal will still be smaller than the average deal at the bulge brackets.

Yes, the EBs do advise on some mega-deals, but they also advise on plenty of smaller, less significant deals as well – take a look at any of these banks’ “Recent Transactions” pages to see.

Another issue is that the experience at elite boutiques is highly variable – more so than it is at the larger banks.

If you’re working in M&A or Restructuring at Evercore in New York, sure, you’ll probably get a great experience with solid exit opportunities.

But if you’re in a smaller industry group at one of the “borderline” EBs in a regional office, anything could happen.

Some of the newer EBs are also dependent on key people, and deal flow tends to suffer when these people retire or get poached.

Finally, the elite boutiques don’t hire that many people each year – altogether, they might make a few hundred front-office entry-level hires worldwide, while the bulge brackets hire in the thousands.

So, even if your ultimate goal is an elite boutique, it’s not a great idea to focus on them exclusively.

Will EBs Take Over the World?

If you’re extremely certain you want to stay in finance long-term, and you’re a competitive candidate for EB/BB banks, then the elite boutiques might seem like the best option.

The most credible argument against them is that there are significant differences between individual banks at this level, and an offer from a “lesser” or newer firm might be worse than one from a large bank.

Advantages of Working in Investment Banking at the Elite Boutiques:

- Better / More Interesting Deal Experience: You’ll have more responsibilities, you’ll do more in-depth analysis for each deal, and you won’t be quite as much of a cog in the machine.

- Higher Cash Compensation: Bonuses for junior bankers tend to be higher, and at the senior levels, there are no deferred or stock-based bonuses.

- Better for a Long-Term Finance Career: EBs give you similar access to private equity and hedge funds, and if you want to stay in investment banking and advance up the ladder, you’ll have a better experience at an EB.

Disadvantages of Working in Investment Banking at the Elite Boutiques:

- Lesser-Known Brand Name and Smaller Alumni Network: These both make it more challenging to leave finance and work in another industry.

- Highly Variable Experience at Different Offices and Banks: While the “top” EBs are fairly consistent, the others fluctuate from year to year, and your experience could be very different depending on the presence of one key rainmaker or a single deal.

- Still Extremely Competitive to Win Internships and Jobs: You still have to start ridiculously early, earn high grades, attend a top university or MBA, and complete a sequence of internships… but you also need more luck since EBs hire fewer people.

- Long Hours and Unpredictable Lifestyle: And do not expect any “lifestyle improvement” over the bulge brackets – some elite boutiques are known for even worse hours!

My advice here is “Buyer beware.”

Yes, you could certainly make a strong case for accepting an offer at one of the top EBs over one at a BB bank.

But as you go down the list and move outside of NYC / London, the rationale gets murkier.

The elite boutiques do offer many benefits, but I’m not quite as “sold” on them as many people online are.

And if you’re competitive for neither bulge brackets nor elite boutiques, the good news is you won’t have to make this tough decision at all – just get started networking elsewhere.

Want more?

You might be interested in reading Middle Market Investment Banks: Solid Entry Point, or “Plan B”?

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Hi Brian,

Can you publish an article about how international students can break into ib?

https://mergersandinquisitions.com/international-student-investment-banking/

Would you consider going exclusively for the EB a great route if you want to avoid interest and lending operations? I know it might be a crazy question to ask in the finance industry but I am genuinely interested. Are you aware of any other routes in finance within Buy-Side and Sell-Side roles, which do not work with interest, lending, and debts?

I don’t really know about that, sorry, but even at an elite boutique, you will be dealing with interest rates and debt because most companies have some amount of debt. If you want to avoid it altogether, you’ll probably need to think about Islamic banking/finance, which I know nothing about.

Hey Brian, at Houlihan Lokey they have a Financial Analysis department that focuses more on Portfolio Valuation, Fairness Opinions, tax analysis etc. but doesn’t work on deals. Do you think this can be relevant to move to IB in another bank or it would better an experience in a regional M&A boutique/ Big4 M&A advisory? Thanks!

You’re generally better off working in actual investment banking, even if it’s at a regional boutique, or in the advisory group of a Big 4 firm, than you are in portfolio valuation / FOs / tax / other groups that are less relevant to deals.

Yes, the HL name is well-known within banking, which will help, but I think it will be hard to spin your experience into sounding like you worked on deals when you did not actually work on deals.

Hey Brian – Outside the normal tips to break into IB, anything else in particular when coming from Big 4? Especially if I am trying to go the EB route?

Thanks!

Sorry, not really. There are no magical tips or tricks, just the usual networking/prep grind. Coming from a Big 4 background, you will probably get a lot of cultural/fit/”airport test” type questions because they will assume you already know accounting quite well… so be prepared to show your non-work interests as well.

Wondering how likely it is to get looks from megafunds from Centerview – seems like their reputation is weaker than Evercore or Lazard?

It’s possible, but yes, it’s probably slightly below the other elite boutiques in terms of recruiting. Not worth it to lateral or try to move to a “better” bank because most Analysts at such banks do not even end up in megafunds anyway.

Regarding Centerview’s reputation in comparison to other elite boutiques, why is it slightly below Lazard and Evercore when it comes to MF recruiting?

I don’t know, but probably because Evercore and Lazard have been around longer.

Hi Brian,

I’m a 26 year old who has gone from public accounting to corporate accounting/financial analysis. I was kind of forced into the role timing wise and because I was desperate to get out of public. I really like the company, they are Fortune 500, because they have great people, culture, etc. The other main reason is because they have a FP&A group that also handles corporate development. I am expecting the acquisitions to pick up in the next 1-2 years due to a strategy change. I am thinking I can hopefully move into this group in 2020.

I realize being 26 and only having a few months of a private equity internship in college means I have been stuck in accounting for way longer than I would’ve like to have been if I want to eventually get into finance more. I guess my problem is that I dont know which route in finance I want to take and my hometown is a good sized city, but they dont have dozens of opportunities in finance. My question is, should I stick it out in this company where I’m liked and doing well and will hopefully have a chance on this team in the next few months… or should I be looking to jump ship into whatever kind of finance role I can get before I pigeonhole myself even more in accounting?

I think you have to wait and see because it depends on how much corporate development activities pick up. If they do, and you can move into the FP&A group and also work on deals, then you should do that. I don’t think leaving right now will help you since you still won’t have deal experience.

But the bigger issue is that you don’t seem sure of what you want to do, so I’m not sure what to say – what is your goal? IB/PE? Something else in finance? Do you want to work on deals or follow companies?

I would need answers to those questions to say anything else.

Hi Brian,

Thanks for your response. My main goal is to work in something more meaningful and interesting. My summer internship at a private equity firm was very interesting. I learned a lot and the idea of fast moving transactions still appeals to me. Plus, I’ve really enjoyed reading your articles across a bunch of different career types. My real question is, given my primarily accounting background, hopefully with a year or two of corporate development experience, how realistic are these tracks?

1) Corporate VC – one of our largest healthcare systems has a VC fund that invests. I figured I could work my way onto their transaction team, eventually get my MBA with their brand name on my resume and then reevaluate.

2) Corporate Restructuring/Turnaround Advisory – I have been interested in this route since it has a lot of good finance and accounting. The main problem is the excessive travel, but I could handle it given the learning opportunities.

3) A small PE fund – My city has a few smaller PE funds, the type where you dont need to spend several years at a brand name investment bank. Maybe spend a few years here and then join a capital advisory/due diligence firm?

4) Stick out the corporate development route – I could easily seeing this be the route I take. I like the company I’m at, I think they are well positioned in the market, and they have a good track record of promoting people.

I appreciate your feedback and the great resource this website has been.

I think #1 is most realistic, and also #4 assuming you get into corporate development.

The problem with #2 is that you often need restructuring or distressed experience to get in (see: https://mergersandinquisitions.com/restructuring-turnaround-consulting/). But some people do get in from CF / CD, so it is possible.

#3 will probably be the most difficult because it’s not easy to move into PE from CD even though they both involve transaction work. If you’re willing to do A LOT of networking over a long period of time, potentially you could do it. But keep in mind that PE is so competitive that even most bankers don’t end up in the field. To get in from outside banking, you’re going to need a lot of time and effort and some luck.

Despite Greenhill’s elite boutique status up in the air, from your knowledge, do they get looks from all the top headhunters?

It’s still very plausible to go from Greenhill to PE/HF/related exits, but it seems to be not quite as good as Evercore/Lazard/Centerview. So I’m not sure I would say “all” but “many,” sure. It’s also tough to distinguish between receiving headhunter attention vs. receiving offers (no one really likes to share how many interviews they had or at which firms).