Boutique Investment Banks: The Full Guide

But it’s logical to address the most serious problem first – namely, that there are four major categories of “boutique banks,” and they are each quite different:

- Elite Boutique Banks (EBs)

- Up-and-Coming Elite Boutiques (UCEBs)

- Industry-Specific Boutiques (ISBs)

- Regional Boutiques (RBs)

Each category is so different that I could write an entire article about each one.

But hardly anyone searches for “industry-specific boutiques,” so I’m going to cover the final three categories here.

Boutique investment banks advise on “smaller deals,” often in the $50 – $100 million range or below, and they usually focus on one specific product, geography, or industry; exit opportunities are more limited as well.

In practice, most boutique investment banks focus on M&A Advisory or Restructuring because it’s difficult to compete in areas like ECM and DCM without much bigger teams.

There are hundreds or thousands of banks worldwide that qualify as “boutiques,” so I can’t possibly list everything. But here are a few examples by category:

What is a “Boutique Investment Bank”?

Definition: A boutique investment bank is a non-full-service firm that focuses on M&A Advisory or Restructuring, rather than capital markets, and that advises on deals that are significantly smaller ($50 – $100 million range or less) than those of bulge bracket or middle market banks; these deals are often concentrated in one industry or geography.

This definition refers primarily to Regional Boutiques (RBs) and some Industry-Specific Boutiques (ISBs).

Elite boutiques (EBs) are a completely different story because they advise on much bigger deals, and Analysts from EBs have much better exit opportunities.

Up-and-coming elite boutiques (UCEBs) also do not fit this definition because they often work on much bigger deals.

However, they are similar to RBs and ISBs in terms of headcount, geographic reach, and industry concentration – and it’s not clear how solid the exit opportunities are.

When in doubt, remember that size matters. If a bank consistently works on deals below $100 million, it’s a boutique, no matter how they try to spin it.

Boutique Investment Banks vs. Middle Market Banks vs. Elite Boutique Investment Banks

It should be easy to tell apart boutique investment banks from the bulge brackets: size, size, and size.

But things get murkier when you compare boutiques, elite boutiques, and middle market banks.

Here’s how you can tell them apart:

- Deal Size: If the firm often advises on $1 billion+ deals, it’s not a regional or industry-specific boutique bank, nor is it a middle market bank. It is likely an elite boutique or up-and-coming elite boutique.

- Services Provided: If the firm legitimately does a lot more than just M&A or Restructuring, it’s probably a middle market bank and not an EB, RB, ISB, or UCEB. But there is a grey area here between MMs and ISBs.

- Industry: If it’s narrowly focused on a single industry, it’s probably an RB, ISB, or UCEB.

- Geography: If it has fewer than 5 offices, it’s probably an RB, ISB, or UCEB. With more than 5 offices, it’s closer to MM or EB territory.

- Headcount: If it has fewer than 250 employees, it could be an ISB, UCEB, or RB. But if it has under 50 employees, it’s almost certainly a UCEB or RB.

- Exit Opportunities: If very few Analysts get into private equity or hedge funds, it’s probably an RB or ISB (the UCEB standing is unclear).

Here are a few examples:

SVB Leerink is a well-known healthcare-focused bank. It does more than just M&A, but most of its deals are under $100 million or “undisclosed.” It only does healthcare, and it has 4 locations and ~200 employees, so we’d say it’s an industry-specific boutique.

LionTree Advisors often works on multi-billion-dollar deals, so you can immediately tell it’s an EB or UCEB. It only does M&A, it focuses strictly on TMT investment banking, it has 4 offices, and it has fewer than 200 employees, so it’s an up-and-coming elite boutique.

Aethlon Capital in Minneapolis has all “undisclosed” deal sizes, indicating the deals are small, it only does M&A and private placements, it has just 1 location, and it has fewer than 10 employees, so it’s a regional boutique.

Ranking these firms is close to impossible, given that there are thousands of them with very limited data, so I’ll cover the major differences by category instead:

Up-and-Coming Elite Boutiques (UCEBs)

These firms are often founded by senior bankers from EB or BB banks who take a few big clients with them and establish a niche within an industry – even with very small teams.

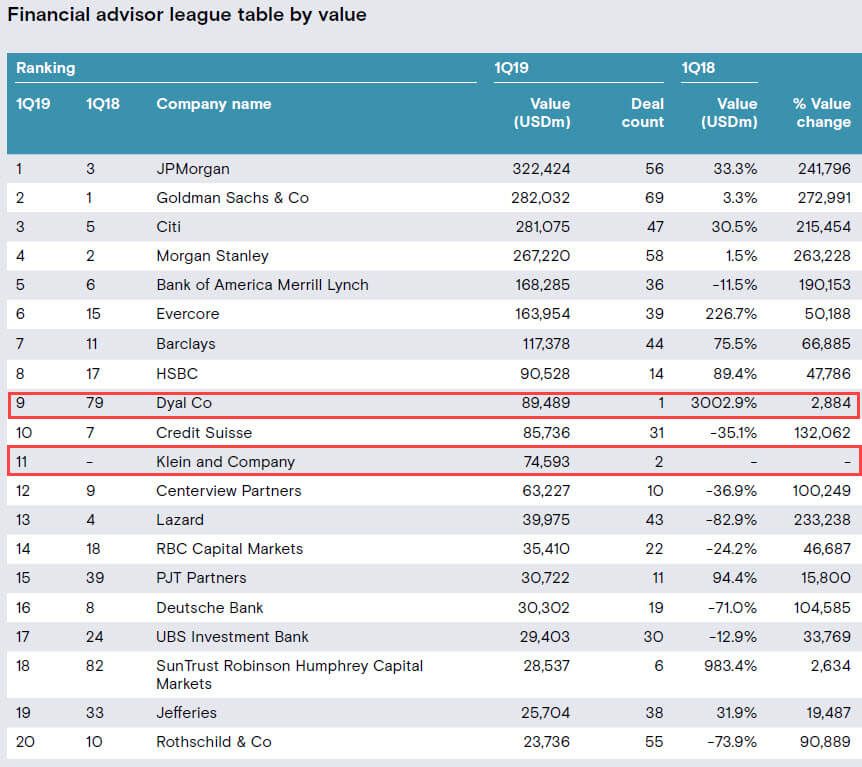

For example, Robey Warshaw has fewer than 20 employees, but it has advised on M&A deals worth tens of billions of dollars, including Comcast’s acquisition of Sky.

This explains why you sometimes see these firms on the league tables, comparing favorably with BB and EB banks in terms of deal values:

In theory, these firms sound great: you still work on large and complex deals, but you’re on a small team, so you get massive deal exposure.

In practice, there are two problems with that:

- The hours are often insane, even by IB standards. Think: 16 hours every day, every week, with no time off while that $70 billion deal is happening.

- Since the Analyst classes are small, and these firms are very new, the exit opportunities are unclear. Most likely, though, you will not have a good shot at large HFs and PE firms until your UCEB turns into an EB instead.

Industry-Specific Boutiques (ISBs)

The ISBs are often closer to middle market banks because they tend to work on larger deals, they may have a few offices, and Analysts have somewhat-better exit opportunities.

But they’re still less diversified than MM banks, and their average deal is far smaller than the average at EB and BB banks.

Examples include SVB Leerink (Healthcare), Ziegler (Healthcare, Senior Living, and Education), FT Partners (Fintech), Raine Group and Allen & Co. (both TMT), Seabury (Transportation/Maritime/Aerospace & Defense), Telsey Advisory Group (Consumer/Retail), Valence Group (Chemicals), and dozens of others.

Industry-specific boutiques are often attractive acquisition targets because they allow larger banks to scale or make up for weaknesses.

For example, Cain Brothers was a well-known ISB in the healthcare sector until KeyBanc acquired it in 2017.

And KBW (Keefe, Bruyette & Woods) was a top ISB in financial services until Stifel acquired it in 2013.

Both firms still operate somewhat independently within larger organizations.

You could make the case that ISBs are closer to MM banks, but they still suffer from some of the same problems as the UCEBs: highly variable culture/hours/lifestyle and unclear exit opportunities.

For example, FT Partners “some of the banks above” are known for old-school banking cultures where Analysts work… a lot, more than even at BB banks.

Yes, they get great deal experience, but their exit opportunities are not commensurate with their hours worked.

Regional Boutiques (RBs)

When most people say “boutique banks,” they’re referring to regional boutiques.

These firms have anywhere from ~5 to ~50 employees, with 1-2 offices, and they advise on smaller deals (usually under $50 million).

Example firms include Marlin & Associates, Financo, Foros, KLR Group, Rivington Capital Advisors, India Brook Partners, Young & Partners, Sawaya Partners, Cleantech Group, and hundreds of others.

You could arguably call some of these firms “industry-specific boutiques” instead; it’s hard to tell because few disclose deal sizes.

Often, these firms are founded by veteran bankers from larger firms who want more independence, so the culture, hours, and lifestyle vary widely.

For example, I once interviewed a reader who interned at a regional boutique bank where:

- The team worked only 40-50 hours per week…

- …because they did not pitch for deals or do pointless work (e.g., changing the border colors in a CIM 15 times).

- Instead, the MDs there used their existing contacts and relationships to advise only on inbound deal inquiries.

Some regional boutiques are closer to MM, EB, or BB firms in terms of hours and lifestyle, so this example is not representative of the entire category.

However, it is fair to say that the average hours are lower at true regional boutique banks, often in the ranges of 60-70 or 50-60 hours per week.

You will probably get more exposure to deal processes at these smaller firms, but there are two big disadvantages:

- Compensation is significantly lower, mostly because of lower bonuses.

- Exit opportunities are much worse, and if you want to win a traditional PE/HF role, you’ll almost certainly have to move to a larger firm.

Why Work at a Boutique Investment Bank?

Boutique banks tend to be good for entry-level candidates, such as:

- University students who are completing their first internships.

- “Late starters” who already graduated and need work experience ASAP.

Recruiting is less competitive, and you can often win interviews and offers with aggressive cold calling and cold emailing.

Boutiques can also be good for senior bankers who are tired of working at big, bureaucratic firms, and who want a better lifestyle and more independence.

However, they’re not so good for people in the middle (Associates, VPs, and Directors) because many boutiques are thinly staffed and don’t necessarily offer a pathway to the top.

Also, rather than paying high salaries + bonuses, many regional boutiques offer “profit-sharing” plans to mid-level bankers, so compensation fluctuates significantly from year to year.

Why Not Work at a Boutique Investment Bank?

Deals are smaller and simpler, the firms are not well-known, and cash compensation is lower – especially at regional boutiques.

The experience is even more variable than working at an MM or EB bank, and the exit opportunities range from “unclear” to “limited.”

Advantages of Working in Investment Banking at a Boutique Bank:

The list of advantages and disadvantages is very similar to the list for middle market banks, but even more extreme:

- Boutiques are good for initial internships and entry-level roles if you got started late, changed your major or career path, or had other issues during undergrad.

- You could get a lot more deal exposure in terms of interaction with executives and counterparties.

- And some boutique banks have great cultures where you’re treated like a human, you spend less time on pointless tasks, and you work more like 60-70 hours per week.

- At the senior levels, cash compensation could be higher than cash compensation at larger banks if you perform well and close many deals.

Disadvantages of Working in Investment Banking at a Boutique Bank:

- Deals tend to be smaller and simpler, which may limit the technical skills you gain.

- Regional boutique banks rarely give full-time return offers to interns, so you’ll have to recruit elsewhere once your internship is done.

- Most boutiques (of all types) have small Analyst classes, which limits your network.

- Bonuses, at least at regional boutiques, are significantly lower.

- It’s not great to be “in the middle” of the hierarchy at these firms because there are fewer spots for Associates, VPs, and Directors, and compensation fluctuates significantly due to profit-share schemes.

- Highly variable work experience and culture, ranging from work-Analysts-to-death at some firms to relax-and-barely-work-more-than-a-standard-corporate-job at others.

- Reduced exit opportunities because you’re unlikely to win traditional PE/HF roles. The main options include corporate development, corporate finance, another bank, and maybe growth equity or venture capital, depending on your industry.

Are Boutique Banks for You?

The merits of boutique banks depend on your options.

If it’s a boutique bank vs. something outside IB/PE, such as a Big 4 firm or corporate finance at a mid-sized company, take the boutique offer.

If you end up cold-calling companies all day, move to another bank.

In most cases, MM banks beat boutique banks, and EB/BB banks beat MM banks, but there are always exceptions.

ISBs and MMs are sometimes a tougher call, and if you want to focus on a specific industry over the long term, an ISB might be a better bet.

And I’m not sure what to make of the UCEBs yet; there’s too little data on exit opportunities and long-term career outcomes.

But if you’ve read all the articles in this series, your own decision shouldn’t be tough to make – once you’ve sorted through all the online confusion.

For Further Reading:

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Brian, super helpful and detailed sharing. Especially for the description of the regional boutique, it is my daily life and says what I feel every day—many thanks.

And Brian, do you have any tips for someone like me who stays in a regional boutique and wish to move to EB/MM? The average deal value for us is approx USD 50mn. Sometimes we have larger deals (>100mn) and don’t have an industry focus but a regional focus. (Asia deals). In your view, When is the time to prepare to move? (One year or longer)

I am looking forward to moving into a MM/EB with a better-known name. I haven’t decided if I want to go for PE but I am sure I want to keep on working in M&A.

Looking forward to hearing from you.

Thanks. I would wait until you have at least 2 solid deals you can speak about in interviews. Making the move is mostly about networking with other bankers and following up repeatedly. See the article on lateral hiring on this site for examples.

Hi Brian, thank you for your post.

I am a third-year uni student at an Ivy League, and was wondering whether it would be best for me to accept an offer at a mid-market boutique that close many deals (i.e. Clairfield International) or to go with a MM bank (i.e. Lincoln International or Crédit Agricole) in a region where they closed just a very few deals since many years? Is it, therefore, more important at an Analyst level to work on many deals as possible in a less-known firm or to be in a well-known firm and close less, but bigger, deals?

Thank you.

That is a good question. If this is a summer internship offer, I would go with the MM bank with the better-known name even if it’s in a region where they don’t have much deal activity. The reason is that for internships, you can always move around afterward, and the brand name tends to matter more than what you did on the job since you’re only there for a few months anyway.

If this is for a full-time role, you could potentially argue that the MM boutique that closes many deals will give you better experience if your goal is to stay in IB. However, I’d say that even in that case, you’re still probably better off going with the better-known MM bank if you’re interested in buy-side roles and do not plan to stay in IB for the long term.

Thoughts on exit opps from top industry specific firm (SVB/ FT Partners)? Not really interested in mega-fund PE but likely MM PE or potential Corp Dev/Strategic Finance. Know FT specifically has grown a ton recently, great deal flow, and added senior bankers from several EB/BBs but curious as to your thoughts?

You can probably do either of those coming from those firms. I haven’t really followed FTP’s growth, but if you want more of a scientific answer, do a search on LinkedIn and see where 20-30 FTP Analysts from the last few years have ended up. I would guess it’s probably a mix of MM/smaller PE, growth equity, VC, and corp dev.

Hi Brian,

Long time reader and big fan of your work. I was just wanting to ask what your thoughts were for Berkshire Global Advisors? Would you see many exit opportunities for firms like this that are probably classified as a regional boutique but do engage in FIG, FSG and are building their practice in other areas? I can see that they are specialised but are branching into real estate, fintech and infrastructure management plus they do deals in the millions but have done a few in the low billions.

I don’t know much about them, sorry. They seem to have advised on some large/well-known deals based on the website, but I haven’t done specific research on the firm. I’m not sure they are a “regional boutique,” probably more of an industry-specific boutique. So there will be exits, but probably not to PE mega-funds or large hedge funds because the spots at those places are just too limited.

Hi Brian,

Wanted your gut feeling on boutique vs top MM/low BB based on my situation:

Starting w/ a TL;DR, boutique M&A across multiple industries in low CoL area vs top MM in NYC for NFP hospitals, in context of IFC Investment Analyst exit in 2023. Details below.

I am choosing between a regional boutique (one office, ~15 people) as an experienced analyst doing M&A across industries in a low CoL area I currently reside in, or a lateral analyst at a top MM (though HR contact calls themselves a bulge bracket) in NYC focused on NFP Hospitals, which is the industry I have been working in for ~1.5 yrs.

My goal is to apply to the IFC as an Investment Analyst in January 2023, possibly go the impact investing route a few years after that/later in life or some career route similar to that (though I am not writing off PE, Corp Dev, or lateraling to another bank).

I like the culture of the boutique and the team there is great, granted they come from accounting/boutique banking backgrounds and do not come from top schools. Lifestyle is good, with 60-70 hours being the worst of it when properly staffed. However, since I am only planning on entering banking once for a 1.5-2 yr stint, is it worth it to take such a dive in prestige and some pay? After factoring in NYC CoL and conservative bonus estimate, I would make about the same or a little more at the more prestigious as the boutique (a lot more with an optimistic bonus estimate). Base varies by 5% between the two.

My background is undergrad from no-name school and masters from LSE, both in accounting. Internships in middle office MS and audit Deloitte, and FT experience in healthcare consulting at T20 CPA firm.

Side note, M&I has been incredibly helpful and arguably the main influence in how I have crafted my journey to the present opportunities since my sophomore year of college. It took me a while, but have finally won an offer in banking and your free content has been huge for me.

Thanks. I would go with the top MM in NYC for NFP hospitals because for something like the IFC, brand name/recognition matters a lot. The work may also be seen as more relevant.

Hi Brian,

When cold e-mailing regional boutiques to ask about unofficial summer internships, should we address the e-mail to their info address (such as info@xyzbank.com) or to a senior member of the firm, assuming they don’t have a dedicated e-mail address for recruiting? Thanks!

Ideally, email a senior banker there. If you can’t find one, go for a junior banker instead. If you can’t find an actual person’s email address, it’s a bit pointless to email the “info address” of the firm – at that level, you might as well just cold call the firm to ask about recruiting/internships because you’ll be more likely to speak with a human that way.

Hi Brian,

Thank you for the articles as always – very insightful. I am currently a junior who is late to the game but am networking to get a shot at a few industry specific boutique banks that have been mentioned above or even some regional ones in the NY office. I am frankly not 100% sure whether I want to do PE (definitely not hedge fund) or stay in finance and have still thought about consulting, but finance is the priority. What has the percentage of people moving from these boutiques to BBs have been like? Do you think FT recruiting from boutiques will be possible at all given the current situation with the economy and banks cuttin headcounts? How difficult is it to balance networking during working FT if you are considering this transition?

I don’t know the exact percentage, sorry. A fair number of people do switch because turnover is quite high, and people quit all the time. I think it will be very difficult to win any FT offer without a previous internship that converts into the FT offer, but you might as well try if you’re already networking extensively. If that doesn’t work, maybe just get a Big 4 or valuation or corporate banking role or something similar and use that to move in.

I have over 3 years’ M&A experience at a BB firm working on lower middle market size deals, a university degree majoring in accounting (GPA 2.5/4.0), and I am based in South Africa – therefore, I would need a US company to help with sponsoring me to (for example) get through the US work visa’s PERM Labor Certification Process…

Do I actually have any real chance of landing ANY full-time Investment Banking Analyst job (entry-level job) in the United States (or Canada)? Is it even worth my time to explore this? I mean if there are many other US-based candidates who have better GPA’s than me, then I guess it’s not worth even trying, right?

Or can my 3+ years’ experience in this field (perhaps) make up for my ‘geographic-handicap’ and ‘GPA-handicap’?

In other words, generally speaking what is more important to a typical IB employer / recruiter: that a new analyst has a ‘stratospheric-GPA’ and is US-based already (hence relatively easily employable), or is someone who knows the difference between a recapitalization deal and a growth capital deal, to name just one example, and who is someone that can find his own way through a deal (A-Z) to ultimately close a deal?

I think it’s going to be extremely difficult in the current environment, with a global pandemic, cities burning down in the US, massive social unrest, restrictions on travel/immigration, and the fact that you would need a domestic bank to sponsor you. Your experience sounds good, but the issue is that there are also experienced Analysts in the US and Canada who know deals and have solid experience. Not everyone in the country is an idiot, though it does seem that way from the news sometimes.

If you want exposure to a bigger/better market, you will probably have more luck applying to IB jobs in Europe at this stage. Though I’m not 100% certain how the crisis has affected work visas in each country there.

Thanks Brian, your feedback is sincerely appreciated. Before COVID-19 struck, would I have stood any chance? If yes, then should I simply “wait it out” until i.e. July 2022? In other words, do you think I will then (in i.e. June 2022) stand any chance in the US or Canada?

Sure, potentially. I don’t know what else you can do at this point other than wait.

Hi Brian, re the FINRA exams (FINRA series 63 and 79 exams), I see that there is actually an official FINRA exams writing venue nearby me in a city in South Africa. Would it make any difference for any typical US investment banking analyst Employer or Recruiter if I have already completed these two FINRA exams?

If yes, would the potential positive impact of this be (a) big, (b) medium, or (c) small on my chances of getting employed and therefore an employer also (actually) helping me to get a US work visa let’s say sometime in the future (i.e. mid-2022) after this COVID-19 mess has finally blown over?

These exams barely make a difference. They might help a small bit, but they’re not going to help you with a work visa or eventually working in the US (although I’m not really sure why you’d want to live or work in the US for any reason in the near future).

Thanks Brian, feedback much appreciated.

What would you classify Rothschild & Co as in the US? They mostly do M&A in the middle market space but their restructuring group takes on bigger scale mandates and has exit ops that are similar to some EBs.

Probably “industry-specific boutique” in the U.S. because of the difference between the Restructuring group and everything else there. In Europe they are considered an elite boutique.

What about the BDA Partners, a firm focused on deals in Asia. How would you classify them?

From what I can see, probably an industry-specific boutique:

-200+ employees on LinkedIn

-Focus on Asia deals

-9 locations

-Average transaction size is unclear, but if the sizes are all undisclosed, they’re probably small

Some people would say regional boutique because of the last point, but it’s probably closer to ISB judging by the headcount.

Saw you mentioned KeyBanc in the article. Do you happen to have any insights on them or a view on their reputation? Thanks.

I’d say it’s a solid middle market firm with several strong groups (tech, healthcare due to the Cain acquisition, industrials, real estate, etc.). It’s not as well-known as some of the other MM banks yet, so that hurts a bit when it comes to exits.

What about your exit opportunities from a boutique to BB IB team?

They exist, but it depends on the type of boutique you’re at. You are probably not going to move directly from a 5-person shop to Goldman Sachs in NY, but you could move from firms like SVB Leerink or FT Partners (for example) to BB banks. Same with transitioning from firms like LionTree and other UCEBs.

If you’re at a true regional boutique, you will usually have to move somewhere else first, such as a MM firm or a larger, industry-specific boutique, or something like that.