Convertible Arbitrage Hedge Funds: The Perfect Combination of Investment Banking and Sales & Trading?

Traditionally, if someone asked the “sales & trading vs. investment banking” question, the response was easy:

“Do banking unless you really, really like trading and could not imagine doing anything else.”

But there might be another equally valid answer: “If you can’t decide, do both and use your combined skills and experience to move into a convertible arbitrage hedge fund.”

Convertible bonds are hybrid instruments with elements of debt and equity, and some groups that trade convertible bonds also combine elements of S&T and IB.

But before delving into the best candidates for these roles, typical trades, careers, and more, let’s start with the basic definitions:

What is a Convertible Arbitrage Hedge Fund?

Convertible Arbitrage Definition: Convertible arbitrage is a relative value strategy in which a hedge fund profits based on the pricing discrepancy between a company’s convertible bonds and its underlying stock; the fund exploits changes in volatility, credit quality, and interest rates to make money while minimizing overall market risk.

If you’re using a strategy like long/short equity, you could long or short a company’s stock, and your results would depend heavily on the stock market’s overall direction.

If the market goes up 20%, and you bought the stock, you are probably going to make money because most stocks have a positive correlation with the overall stock market.

But with convertible arbitrage and other relative value strategies, the overall market’s results do not matter (to the same degree).

For example, if you long a company’s convertible bond and short the underlying stock, and you manage the positions properly, the stock’s volatility – not its absolute price – determines whether or not you make money.

If the stock price goes up or down by 10%, but the volatility stays the same, you might not earn or lose anything on the trade.

But the convertible bond’s current market price implies a volatility of 30%, but you believe the real volatility is 60% or 15%, you can profit if your prediction proves correct.

To explain the mechanics of this trade, we need to start with some background information about convertible bonds:

What Are Convertible Bonds, and Why Do Companies Issue Them?

We have a video overview of convertible bonds along with a simple Excel file and a PDF with the written version below:

Table of Contents:

- 2:20: Part 1: Typical Terms and Conversion Options

- 5:23: Part 2: Which Companies Issue Convertible Bonds?

- 9:25: Part 3: Convertible Bonds on the Financial Statements

- 16:00: Part 4: Convertible Bond Valuation & Black-Scholes

- 20:01: Part 5: Payoff Diagrams and Payback Periods

- 24:01: Part 6: Blended Cost of Convertible Bonds

- 29:05: Recap and Summary

Files:

- Convertible Bond Analysis and Valuation (XL)

- Convertible Bond Analysis – Notes and Presentation (PDF)

Convertible bonds offer lower coupon rates than traditional bonds because they also include conversion options that allow investors to turn the bonds into common shares if the company’s stock price reaches a certain level (the “conversion price”).

So, if a company could issue a traditional bond at a 5% coupon rate, it might be able to issue a convertible bond at a 1% or even a 0% coupon rate.

You can think of a convertible bond as a traditional bond plus an embedded call option on the company’s shares.

These bonds are the most common among companies such as tech and healthcare startups and others in “growth mode.”

These types of companies issue convertible bonds because:

- The cash cost is lower; annual interest on a $1 billion bond might be only $5-10 million on a convertible vs. $50 million on a traditional bond.

- Convertibles lack the same types of covenants (financial restrictions) that many other forms of debt have.

- Convertibles do not create immediate dilution, unlike a traditional IPO or follow-on equity offering.

- And investors like convertibles because they let them capture the equity upside while getting downside protection if the company’s stock price falls.

Let’s say that a company issues a $5 billion convertible bond at a 0.50% coupon rate, and its share price is currently $200. The conversion price is $300.

If this company’s stock price falls to $50 or $100, the convertible bond investors would still receive back their $5 billion when the bond matures, assuming the company remains solvent:

But if the company’s stock price rockets up to $500, the convertible bond investors end up with shares that are worth far more than the $5 billion they initially invested:

Asset managers and long-only funds often buy and hold convertible bonds for this exact reason: equity upside + downside protection.

You can see this by plotting a “payoff diagram” based on the simple examples above:

Note that investors pay a premium to get “the best of both worlds”:

- The underlying shares would have cost only $3.3 billion ($200.00 * 16.7 million). The convertible bond cost 50% extra!

- And if the stock price had increased to $500, the investors would have realized a 150% gain with just the underlying shares (rather than a 67% gain with the convertible bond).

To analyze convertible bonds, you split them into their Liability and Equity components, and you value the Equity component based on Black-Scholes or another option valuation method:

We can’t explain Black-Scholes in detail here, but at a high level, call options (standalone or embedded in a convertible) are worth more when:

- The stock’s volatility is higher – because there’s a higher chance the stock price will exceed the exercise price (conversion price).

- The risk-free rate is higher – because investors benefit from “delaying” their eventual purchase of the underlying shares when they earn higher interest elsewhere.

- The time to expiration or maturity is further away – because there’s more time for the stock price to go up.

The risk-free rate and time to maturity also affect the Liability component (and other factors, such as the company’s credit quality, play a role).

Since a convertible bond’s valuation depends on many factors – volatility, the risk-free rate, credit quality, and time to maturity – convertible arbitrage hedge funds can bet on any or all of these to make money.

A Simple Example of a Convertible Arbitrage Trade

Continuing with the $5 billion convertible bond issuance above, let’s say that the bond is currently trading at $4.7 billion, which implies a volatility of 30%.

You disagree with the market’s assessment and believe the stock’s volatility is closer to 45%.

With a volatility of 45%, the convertible bond would be worth $5.2 billion instead:

Since the convertible appears to be undervalued, you long the bond and short the stock.

You set up the trade this way because you do not care whether the company’s stock price will rise or fall: you just believe the stock’s implied volatility is incorrect.

Therefore, to remove the impact of the stock price, you long an asset that rises when the stock price goes up and short an asset that falls when the stock price goes up.

Normally, you would buy convertible bonds and short-sell shares based on the bond’s delta, or its price sensitivity to a change in the underlying share price.

In this example, the convertible bond’s delta is just above 53% when the bond’s implied volatility is 30%:

So, if the share price rises by $1.00, the convertible bond’s price should rise by $0.53.

Based on that, you might short-sell ~$53 of stock for every ~$100 in convertible bonds you buy.

This setup creates a “delta neutral” position whose value does not change based on the stock price (for more, please see the article on options trading).

The value of your position changes only if factors like the volatility, risk-free rate, or the issuer’s credit quality change.

But there’s a problem: “delta” is not a constant number.

It changes as the underlying share price changes:

So, you need to keep adjusting the number of convertible bonds purchased vs. shares sold if you want to remain delta-neutral as the share price changes.

This process is known as gamma trading (“gamma” is the rate of change in delta), and it’s one reason why convertible arbitrage is much trickier than it seems.

To finish this example, let’s say that the company’s stock price increases by 10% ($200 to $220), and its volatility increases by 50% (30% to 45%).

These changes result in a higher convertible bond price.

If you purchased $2,000 of convertible bonds and short-sold $1,060 of shares, following the initial ~53% delta:

- The convertible bond would now be worth $5.4 billion, up from $4.7 billion, so your $2,000 of convertible bonds would be up by ~14%.

- The shares would now be worth $220 each instead of $200, so your short position would be down by 5.3 * $20 = $106.

For simplicity, I am ignoring the interest, dividends, borrowing costs, and other fees, but this example is the general idea with convertible arbitrage.

The increased volatility is the key.

If it had remained at 30% while the share price increased by 10%, you would have lost a small amount on the trade (assuming no hedge changes, ignoring fees, interest, etc.):

This is the simplest type of convertible arbitrage trade; you could make it more complicated by:

- Adding hedges for the risk-free rate or credit quality (such as interest rate swaps or credit default swaps).

- Selling call options on the company to capture the volatility discrepancy.

- Adjusting the delta hedge to increase or reduce the equity exposure.

You could even make the opposite trade and short the convertible bond while longing the shares if the bond is overpriced.

What Makes Convertible Arbitrage Hedge Funds Different?

Lazard Rathmore has some performance stats for the strategy between 2012 and 2021 here:

Convertible arbitrage is similar to merger arbitrage: it won’t outperform a buy-and-hold strategy on an equity index over many decades…

…but it’s still valuable for its hedging properties and low correlation with the rest of the market.

In terms of other characteristics:

1) Liquidity – Most convertible arbitrage hedge funds offer more liquidity than traditional credit hedge funds but less than strategies like global macro. One problem is that many convertible bond issuances are thinly traded.

2) Time Horizon – Most funds using this strategy approach it as more of a “trading” exercise, so the holding periods tend to be short (hours or days; sometimes weeks).

3) Leverage and Gross/Net Exposure – Most convertible arbitrage funds use more leverage than strategies like long/short equity or credit because it helps boost their moderate but consistent/predictable gains.

It’s common to see gross exposure over 100% (e.g., 100% long and 50% shorts, or even 300% longs and 200% shorts with leverage), with net exposure always positive.

Here’s how Nicholas Investment Partners describes its strategy:

4) Beta – Convertible arbitrage is right in the middle of hedge fund strategies, with a decent correlation to bonds (0.40) and less of a correlation to equities (0.20).

That said, it’s more correlated to the overall market than other relative value strategies, such as volatility arbitrage:

5) Portfolio Concentration – Expect to see dozens of positions rather than concentrated portfolios because most funds “trade” rather than completing fundamental analysis.

The Top Convertible Arbitrage Funds

All the large hedge funds use convertible arbitrage, so you’ll see it at firms such as AQR, Bridgewater, Citadel, Davidson Kempner, Millennium, Point72, and Two Sigma, among others.

It’s extremely difficult to find funds specializing in convertible arbitrage because most firms that do relative value operate in many strategies across the space.

That said, a few smaller funds that are known for convertible arbitrage and relative value include Advent, Alma Capital, Arrowgrass, Bluefin, Centiva, Context Capital, Highbridge, Hudson Bay, Lazard Rathmore (OK, not really an independent fund), Opti Capital, Pine River, and Suttonbrook.

Feel free to leave a comment if you know of others; I spent hours searching but could not find much.

Who Gets Into Convertible Arbitrage Hedge Funds?

The short answer is “mostly traders, some people who worked in hedge funds or asset management right out of undergrad, and a few bankers.”

I did a quick survey of a few dozen LinkedIn profiles and got the following results:

- Sales & Trading Background: 47%

- Hedge Funds / Asset Management Directly Out of Undergrad: 28%

- Investment Banking: 13%

- Mixed IB / S&T Background: 6%

- Credit Investing or Credit Rating Agency: 6%

I also found quite a few people who worked in areas like private equity or distressed investing in between, and even some with equity or credit research experience.

These numbers are heavily skewed toward traders because most convertible arbitrage strategies relate to volatility and rates.

And to implement most of these strategies, you need to know the Greeks, hedging, derivatives, and various other concepts that bankers do not get much exposure to.

Fundamental valuation and DCF models are close to irrelevant.

If you have a banking or research background and you want to invest in convertible bonds, you should find a fund that focuses on buy-and-hold strategies based on fundamental research.

Interviews, Case Studies, and Investment Pitches

Interviews at the average convertible arbitrage fund will be much closer to sales & trading interviews.

Expect to be quizzed on the Greeks, hedging strategies, convertible bond quick math, different indices, and how you might adjust your positions as you set up trades involving convertibles.

If you need trade ideas, I would recommend:

- 1 Traditional Idea and 1 “Different” Idea – For example, propose a long convertible bond / short equity trade and something else that is the reverse, more complex, or that uses instruments like CDS for hedging.

- Addressing All the Risk Factors – Each trade idea needs to address not just the pricing and volatility, but also delta, gamma, and how you’ll hedge the different risks. Something like FX risk might even come into play if the company operates across borders.

It is highly unlikely that you will get a traditional financial modeling test or case study unless you’re applying to a fund that uses buy-and-hold strategies.

If you are, convertible bond investing is similar to growth equity or VC investing with liquidation preferences: you’re evaluating the potential upside vs. the relatively capped downside.

If you’re pitching a “long convertible bond” idea, you need to explain:

- Why the potential equity returns exceed those of other, similar companies;

- And why you would pay extra for the convertible rather than buying the underlying shares directly (e.g., is the potential downside so bad that the cost is justified?).

Convertible Arbitrage Hedge Fund Careers

Not much is different vs. the hours and compensation in other strategies.

The main points are:

- Hours / Intensity – Unlike global macro, with FX markets that trade 24/7, bond markets follow regular trading hours, so you won’t have to spend as much time keeping up outside work. On the other hand, your hours at work will be quite intense because you need to manage your positions very closely.

- Niche Nature – Since convertible arbitrage is a very niche strategy that comes in and out of favor depending on macro conditions, it’s tough to get into and out of. It’s also quite difficult to “learn” independently because you cannot use this strategy effectively as a retail investor (with some exceptions for fundamental-oriented funds).

Exit Opportunities

Convertible bond arbitrage is one of the most niche hedge fund strategies, so it doesn’t give you a direct pathway into much else.

Therefore, your exit opportunities depend on what you did before this.

If you were in rates trading, options trading, or exotics, you could go back to one of those (I found several examples of professionals who moved between banks and hedge funds).

And if you were in equity capital markets or another IB group that dealt with convertibles, you could go back to that.

If you want to stay on the buy-side, you could move around within the relative value space, and something like fixed income or volatility arbitrage might also be possible.

Strategies like long/short equity, credit, activist investing, or global macro are more of a stretch because the skill sets are quite different.

That said, you could always do execution trading at one of these funds if you’ve had experience with derivatives and other instruments they use for hedging.

For Additional Learning

Unsurprisingly, there isn’t much reading material on this specific strategy:

- Convertible Arbitrage: Insights and Techniques for Successful Hedging

- Global Convertible Investing: The Gabelli Way

- Convertible Securities: A Complete Guide to Investment and Corporate Financing Strategies

- RWC Convertible Bond Guide – A useful introduction and quick reference.

Are Convertible Arbitrage Hedge Funds for You?

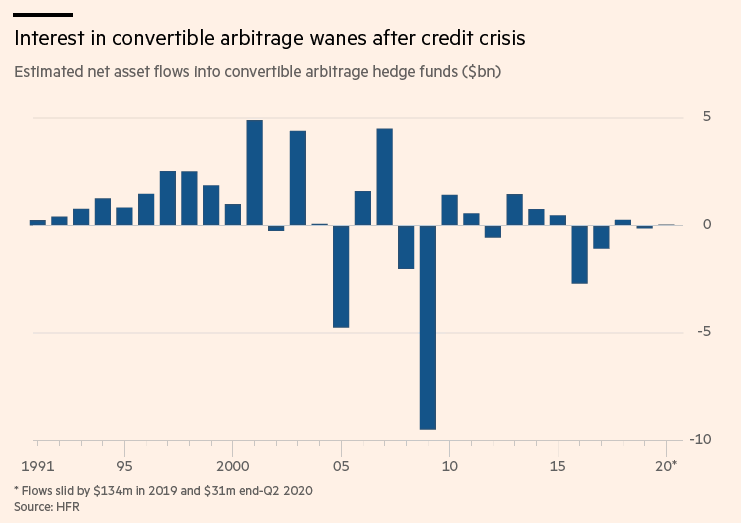

Besides the niche nature, the other problem with convertible arbitrage is that it comes in and out of favor quickly based on the macro environment.

This graph from the Financial Times plotting fund flows into the strategy over ~3 decades sums it up well:

In low-interest-rate environments, convertibles tend to be less appealing because companies could issue straight bonds and also pay low interest.

So, issuances decline, which is bad news if you’re a trader because all convertible bonds eventually mature.

With something like long/short equity, issuances decline in certain periods, but stocks never “mature,” so there’s always a certain amount of trading volume.

Also, despite these funds’ promise to be “market-neutral,” many failed or shut down during the 2008 financial crisis (see the graph above).

There are signs that this is turning around – see the Barclays data here – but in practice, convertible arbitrage may be less “market-neutral” than advertised.

On the other hand, the niche nature of this strategy is also a strength because very few professionals have deep experience with convertible bonds.

So, even if you leave the hedge fund world, you could find another convertible-related role at a bank, in research, or even at a normal company that relies on this financing source.

And if you want to get out of convertibles altogether, well, hopefully, you worked in another strategy or group before this.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Thanks so much! Definitely advanced stuff. I love the example.

Just wondering if you thought the volatility was lower – like 15% instead of 30% or 45%. Does that mean you should ‘short’ the conv bond?

Thanks. If you think the actual volatility is much lower than the implied volatility, then yes, you could short the convertible bond and long the stock.

This is mandatory reading for those interested in convertibles:

https://www.lw.com/admin/upload/SiteAttachments/Demystifying%20Modern%20Convertible%20Notes.pdf

Thanks for sharing that.