Global Macro Hedge Funds: Living in an FX Traders’ Paradise?

Global macro might be the most paradoxical hedge fund strategy.

Some global macro trade ideas are so simple that the average person who knows nothing about finance could understand them.

But the execution is extremely difficult, which explains why some of the largest trading losses in history have come from macro-oriented ideas (“short nickel,” European index futures, oil and gas futures, etc.).

In practice, very few hedge fund Portfolio Managers consistently achieve good results with this strategy over long periods.

And if you add in all the armchair “macro specialists” on online forums, the percentage of traders who perform well plummets.

On the other hand, global macro might be the best strategy if you have a professional sales & trading background or you’ve been an economist, strategist, or policy researcher:

What is Global Macro?

Global Macro Definition: Global macro is an investment strategy in which hedge funds aim to profit from broad market moves rather than from specific stocks or bonds; they invest in currencies, commodities, futures, forwards, swaps, and more, and they analyze fiscal, monetary, trade, and geopolitical trends to make decisions.

The simplest example of a global macro trade idea is a bet on currencies.

Currencies are affected by many factors, including interest rates set by central banks, trade policy, economic growth, inflation, and geopolitical events.

You believe that worldwide inflation will accelerate due to massive fiscal stimulus and money printing by central banks, which should, in theory, boost gold prices.

You’ve also reviewed the central bank policies of Australia and the U.K., and you believe that rate hikes in Australia are not properly priced into the current AUD/GPB exchange rate.

Also, since Australia is the second-largest gold producer globally and one of the top exporters, higher gold prices should boost the AUD because they’ll create a bigger trade surplus.

The simplest trade here would be to long the AUD/GBP, currently at 0.56, with the expectation that it could move above 0.60 over the next 12 months.

You could buy FX put options at 0.53 to limit your losses.

But there are many other ways to trade this scenario:

- Long gold or gold futures and hedge by longing the USD/AUD or the USD against the currency of some other gold-heavy country (as there’s often an inverse relationship between the USD and gold).

- Buy interest rate swaps based on the relative increases in interest rates you expect in the U.K. vs. Australia.

- Use equity or fixed income index futures in these two countries to bet on the one that will be most affected by the interest-rate hikes.

As a PM, you decide which idea is best in terms of risk, potential returns, and overall fit with your portfolio, and then ask your traders and analysts to implement it.

What Makes Global Macro Hedge Funds Different?

The biggest differences vs. other strategies include:

- Broad Sectors and Securities – You need to know at least a little about many different asset classes and derivatives for hedging and risk management.

- No Geographic Restrictions – As the name implies.

- Liquidity – Most global macro hedge funds invest in markets with tons of liquidity, as they must be able to change their positions on short notice.

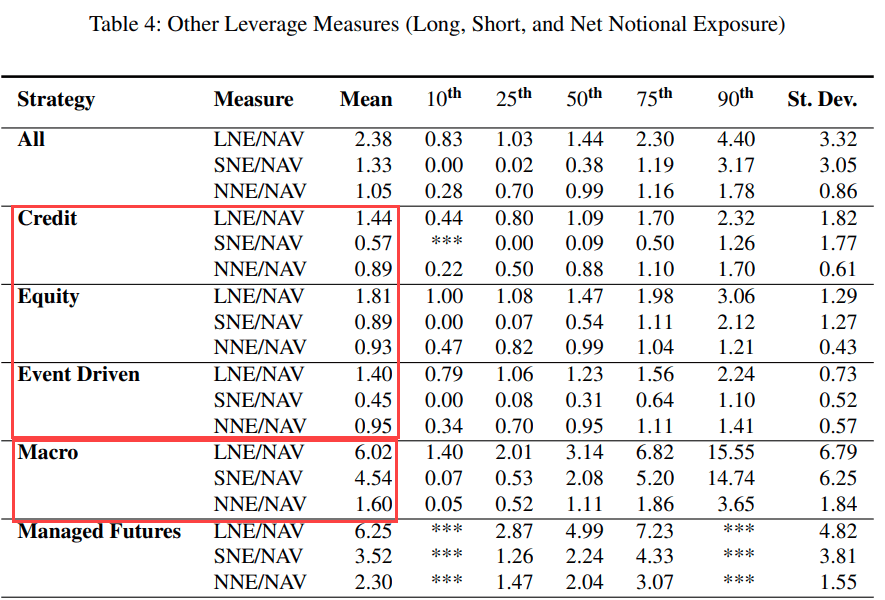

- High Leverage – The average macro or managed futures fund uses a multiple of the leverage that an event-driven, equity, or credit fund uses (source: page 42 of this paper):

For the Limited Partners, a big selling point of global macro is that it has historically had a low correlation with a traditional equities and fixed income portfolio.

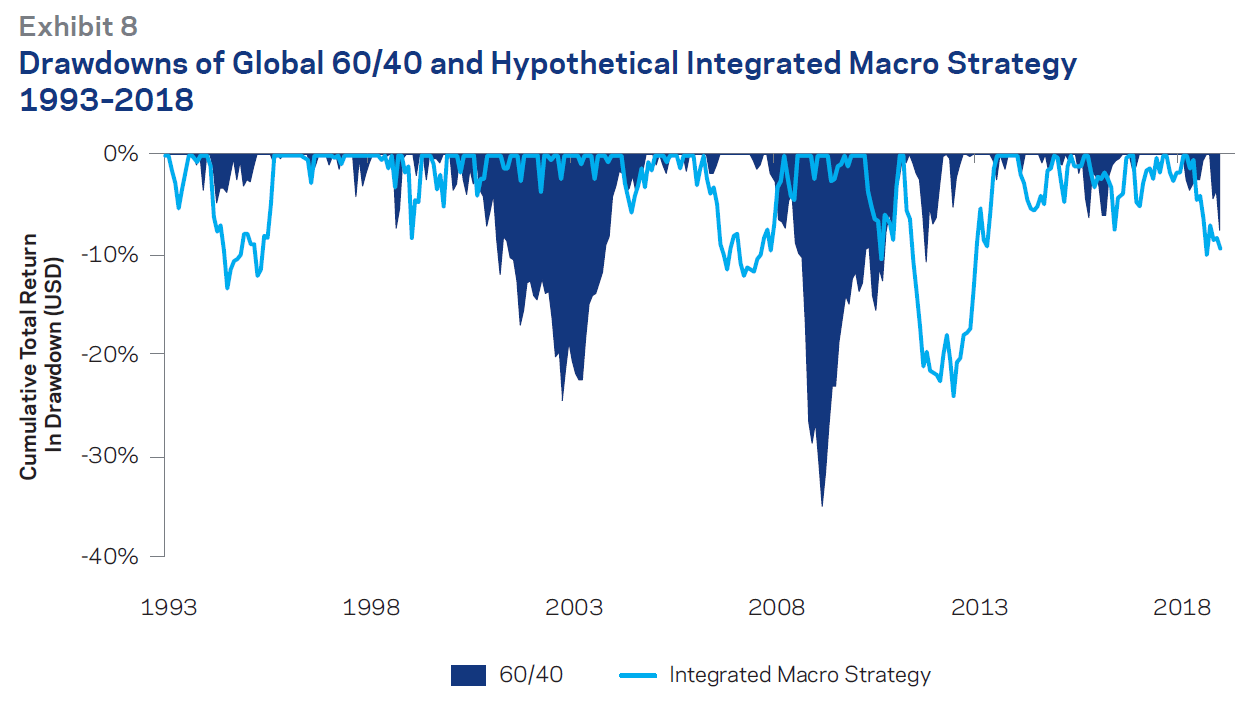

This chart from AQR on a 60/40 portfolio vs. “integrated macro” strategy (i.e., systemic and discretionary) from 1993 to 2018 shows the benefits:

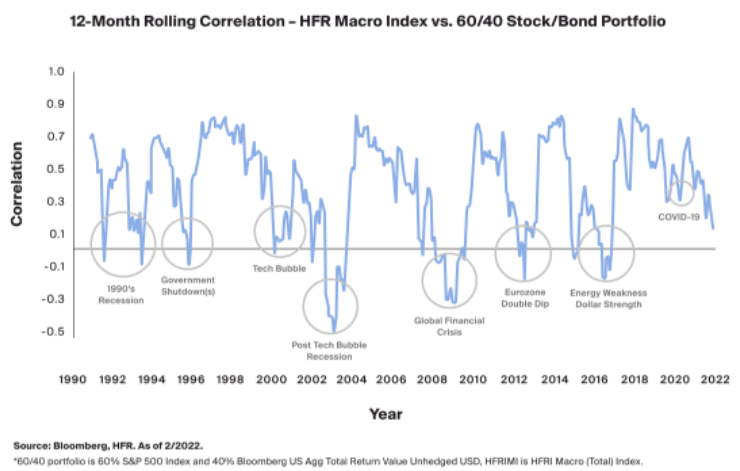

And here’s one based on an actual hedge fund macro index vs. a 60/40 portfolio from 1990 to early 2022:

Although the global macro hedge fund index outperformed 60/40 in this ~30-year period, the main benefit is not so much “outperformance” as it is diversification.

Either approach will produce drawdowns, but they’ll occur at different times and with different magnitudes.

Within the space, global macro hedge funds are split up by the same criteria as always: single-manager vs. multi-manager, discretionary vs. systemic (“quant”), number of positions and average holding period, long/short bias, and gross and net exposure.

Generally, the big multi-manager platform funds tend to be more trader-dominated because their returns depend heavily on risk management and position sizing.

On the other hand, smaller and single-manager funds are more likely to use a research-focused approach in which idea generation is more valuable.

Then there are also commodity trading advisors (CTAs), which are similar to global macro funds, but focus on trend-following algorithms to trade futures, swaps, and commodity options.

What Skills Do You Need for Global Macro Hedge Funds?

The main skill set differences include:

- Risk Management – Yes, this skill is required in all trading and investing roles, but it’s arguably the most important with global macro because it can be tricky to determine the correlations between your different positions.

- Flexibility in Mindset and Views – You need to be able to flip from bull to bear and back very quickly because news and geopolitical events can rapidly change or invalidate your investment theses.

- Trading Track Record – It’s very difficult to “learn” global macro trading independently because the individual contracts for securities like S&P 500 index futures, spot forex, etc., could potentially be worth hundreds of thousands of dollars (or more).

With the first point about risk management, let’s say that you’re long U.S. Treasuries, short the JPY/NZD, long oil futures, long commercial banking equities, and short copper futures.

These might seem like unrelated positions, but in reality, there’s probably some correlation between them (e.g., UST and commercial banks are both highly sensitive to interest rates).

If you misjudge that correlation, a single incorrect macro view could result in you losing money on all these trades.

Global Macro Investment Analysis

Global macro strategies do not rely on traditional Excel-based financial models, so I can’t share much here.

“Idea generation” could consist of anything from reading history books to creating statistical models for different asset classes and external factors like interest rates, trade surplus/deficits, economic growth, and inflation.

Rather than screening by corporate metrics such as FCF Yield or TEV / EBITDA, you might sift through large sets of data and use correlations to find a few ideas that might be profitable.

For example, maybe a statistical analysis based on economic signals has produced a few promising ideas:

- The Malaysian ringgit might be set to rise against the Chinese yuan.

- Palladium prices could rise by 5-10% over the next year, while oil prices could fall by the same percentage.

- The life insurance sector in emerging markets looks cheap, while P&C insurance in developed markets looks expensive.

- And European sovereign bonds seem greatly overpriced, while Asian bonds are underpriced.

As a PM or Analyst, you go through ideas and decide which to pursue and which to drop.

The execution traders then tell you which ones are feasible in terms of position size, liquidity, and risk.

The Top Global Macro Hedge Funds

Almost all the large, multi-manager funds have global macro teams, and they often rely on systematic (quant) strategies: think AQR, Bridgewater, Citadel, and DE Shaw.

Other firms known for being global macro specialists include Brevan Howard, Moore Capital, Caxton Associates, Tudor, Element Capital, Rokos Capital, Balyasny, and ExodusPoint.

Soros Fund Management could also be on this list, but it is currently structured as a family office (it formerly operated as a hedge fund).

Other names include Graham Capital, Pharo, Tenaron Capital, and PolarStar (some of these are known for other or more specific strategies, such as commodities only).

The top places worldwide for global macro are, unsurprisingly, London and New York.

There are far fewer global macro hedge funds based in Asia, and the top ones tend to be the Asian offices of U.S. or European firms, such as Brevan Howard.

The most notable Asia-specific global macro fund is Dymon Asia in Singapore; others include Ocean Arete, Quantedge, Oasis Management, Polymer Capital, and Counterpoint (now owned by Morgan Stanley).

Recruiting Into Global Macro Hedge Funds: Who Gets In?

It’s very rare for investment bankers or equity research professionals to get into global macro hedge funds because the skill sets have almost nothing in common.

The most common entry points are:

- Sales & Trading – Ideally, on a macro-related desk, like FX, rates, commodities, or government bonds.

- Other Hedge Funds and Asset Management Firms – Especially if your strategy was related to global macro or you were an execution trader.

- Central Banks, Governments, and Global Organizations – Common options include a policy/research/economist background at the Federal Reserve, European Central Bank, or International Monetary Fund (IMF). A Ph.D. in Economics also helps.

- Prop Trading or Commodities Trading in Industry – For example, maybe you’ve traded and managed commodity hedges for firms like Cargill or Exxon-Mobil.

- Quant Research or Related Background – Many people with Ph.D.’s and other graduate degrees or other tech experience can do the work required for macro analysis.

- Economics/Strategy Roles at Large Banks – Similar to candidates from the IMF, ECB, or Fed, you should, in theory, have more insight into global trends.

You want to demonstrate skill in research or trading along with solid brand names.

I took a random sample of professionals in my LinkedIn network with “global macro”-related titles and got the following results for their previous backgrounds:

- Sales & Trading: 34%

- Other Hedge Funds and Asset Management Roles: 34%

- Economics/Strategy/Policy: 25%

- Prop Trading: 3%

- Other Finance (Private Equity): 3%

It’s possible to win global macro roles right out of undergrad, but it’s more difficult than winning HF roles in other strategies because it’s difficult to gain the required experience.

If you want to do this, you should focus on quant roles because you can win key internships there that give you a leg up for quant macro roles.

Global Macro Interviews and Case Studies

As with any hedge fund role, interviews will revolve around your thoughts on different sectors and specific trade ideas.

You should aim for at least 1 Long idea and 1 Short, with 3-4 total, and they should be tailored to commodities, FX, rates, futures, and forwards.

A few other tips include:

- Trade Complexity – The simplest idea is an FX trade, and while these can work, you usually want to go beyond by incorporating options or other derivatives into your ideas. A trade idea that spans several asset classes can also help you stand out.

- Non-Directional Trades – You should also consider trade ideas based on something other than price, such as volatility.

- Market Inefficiencies – Probably the most common error when presenting macro ideas is failing to explain why the market is not already pricing in your views.

So, if your trade idea is based on “high inflation,” you need to explain why no one else has noticed and made money from it yet.

For example, are you expecting it to last for more or less time than the consensus view? Will it have 2nd and 3rd order effects that most people are ignoring? Will it result in much higher price increases in some areas than others?

Global Macro Careers, Hours, and Compensation

Not too much is different here; compensation and stress levels, as usual, depend mostly on the single-manager vs. multi-manager distinction and your firm’s culture.

However, there are a few points worth noting:

- Exposure – In global macro, there tends to be less of a “divide” between the Analysts and PMs because the day-to-day work is so varied (economic forecasts, ad hoc research, statistical analysis, etc.). As a result, you’ll get exposed to all aspects of the investment process, arguably making promotions more feasible if you perform well.

- Hours – Your in-office hours will be similar to any other hedge fund, but your out-of-office hours might be higher because markets like FX trade 24/7. Also, you tend to spend a lot of time reading, doing outside research, and even traveling to different regions to assess situations on the ground.

Global Macro Exit Opportunities

The short answer here is that the “exit opportunities” from most global macro hedge fund roles are similar to the entry points into the industry.

You can move to other hedge funds or asset management firms, you can become more of a “macro quant” with the right skills and education, and if you get tired of trading, you can move into strategy, economics, or research at a large bank or organization like the IMF.

On the trading side, you might also be able to win corporate roles at firms that depend heavily on commodities and FX and need to hedge their exposure.

With all that said, hedge fund exit opportunities are still fairly limited, and global macro exit opportunities are even more limited because you do not do “micro” analysis.

Deal-based roles such as investment banking, corporate development, private equity, and venture capital are extremely unlikely unless you’ve worked in one of them before, and even equity research is unlikely because the skill sets don’t match.

So, if you want to move into a completely different career after working at a global macro fund, you’ll probably need an MBA.

Additional Resources

Since global macro deals with all asset classes, the “reading list” here could be quite long.

But here are a few highlights:

- Interest Rate Swaps and Other Derivatives (Corb)

- The Handbook of Fixed Income Securities (Fabozzi)

- A Trader’s First Book on Commodities (Garner)

- Higher Probability Commodity Trading (Garner) (more advanced version)

- Options, Futures, and Other Derivatives (Hull)

- Options Volatility and Pricing (Natenberg)

- The Art of Currency Trading (Donnelly)

- Fed Up! – Personal account of trading through a crisis by Colin Lancaster, the former Head of Macro at Citadel and Balyasny

- The Alchemy of Finance – The classic by George Soros, one of the most famous macro investors of all time

Global Macro Hedge Funds: Final Thoughts

For the right person, global macro hedge funds can be great opportunities.

Ironically, their ability to invest across all asset classes worldwide makes them more specialized than many other types of hedge funds.

If you’re an FX, commodities, or rates trader, you have plenty of ideas, and you want to do more than make markets on the sell-side, global macro could be great for you.

And if you have more of a CS, math, or physics background, along with an interest in the global markets, even better.

But don’t expect to move into a completely different field, or even a much different hedge fund strategy, if you ever get tired of it.

As with long/short equity, people often claim that discretionary global macro is “dying” because of poor performance in the 2010 – 2019 period.

But if you look at the history, that’s fairly typical: it doesn’t have a strong correlation with stocks or bonds, and it tends to do poorly in calm/boring periods.

The strategy benefits from crises and surprises, and this decade is shaping up to be filled with many more shocks than the previous one – so global macro is in a prime position to benefit.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

How feasible is jumping from a macro desk at a top Canadian big 5 to a global macro fund? Or is a stint at a BB in between more useful?

Assuming you want to work at a hedge fund in the U.S. or U.K. (much bigger HF markets than Canada), your chances would be higher coming from one of the official BB banks. Yes, I realize the Canadian Big 5 are similar to the BB banks in Canada, but outside of Canada, their reputation is not the same (maybe with some exceptions, like RBC M&A… but we’re dealing with sales & trading here).

If you want to stay in Canada, potentially you could do this if you move to some type of macro trading group there (maybe within one of the pension funds). But for HFs / buy-side trading in other markets, experience at a BB will help a lot.

Loved this one Brian! I have an upcoming internship at a Global Income Trading desk, and I’ve been looking for more info on this career path. Thank you!

Thanks!

Great article! Defo super relevant given the macro volatility we are especially seeing in FX from central banks raising rates and making the environment more interesting. Are you going to make an article on commodity trading houses (like Glencore, Vitol, Cargill, etc). They are similiar to global macro but much more secretive and have a lot of influence on the world.

Thanks. Yes, I hope to cover commodity trading firms in the future. Not sure how to find much information on them, though…

Hopefully this year some cocky commodity traders will be feel the need to share their stories to the public. On another note, do you think the type of people who get into Sales at a BB are more suitable for commodities in terms of personality? Commodity trading emphasizes more on relationships and logistics rather than market making or directional bets.

Maybe? I honestly couldn’t say because I would have to do more research on the area. I think it also depends a bit on where you’re working (prop trading firm vs. big oil/gas company vs. large bank). But we hope to cover this topic in the future.