Opportunistic Real Estate: An Undiscovered Gem, or Another WeWork Waiting to Happen?

It’s a strategy favored by real estate private equity firms that are willing to use more “unconventional” methods to make deals successful.

For example, they might buy undeveloped land and build a property on it, take an existing property and “redevelop” it into something new, or buy a distressed property and turn it around.

If you’re also looking to take substantial risks, opportunistic real estate might be the field for you.

Some opportunistic deals might even offer greater rewards than equities, but the risk of “pulling a WeWork” and losing all your money is also quite high.

Here’s how you might use opportunistic real estate to elevate the world’s consciousness – or at least make some money without having to be bailed out by a wealthy Japanese guy:

The Main Real Estate Investment Categories

We covered the main categories in the article on core real estate, so please refer back to that.

I like this graph as a sector summary:

Note also that the developers that do the brick-and-mortar work are also, technically, “opportunistic,” but we focus on the investment/deal side on this site.

What Makes Opportunistic Real Estate Different?

Many articles claim that “opportunistic real estate” refers to brand-new developments: buying land, paying to build a new apartment building, office, mall, warehouse, or hotel on it, marketing it to win tenants or guests, and then selling it.

That is the most common deal type, but there are others as well:

- Redevelopments: In this case, the sponsors might acquire an existing property and then demolish and rebuild it to create something new. For example, they might turn an old apartment building into an industrial warehouse.

- Completely Vacant Properties: Maybe the property already exists, but it has major problems and no tenants currently, so significant construction work will be needed to reposition it and attract tenants.

- Distressed Properties: An existing property might be performing well below its potential (e.g., only a 50% occupancy rate), and the sponsor might see an opportunity to turn it around with significant construction work that results in more tenants.

- Distressed Loans: These are not even equity investments, but some people also classify certain types of commercial real estate lending as “opportunistic,” under the logic that distressed loans have higher risk and potential returns than traditional senior loans or mezzanine.

The common thread is that anything in the opportunistic category must be generating little or no cash flow currently.

That makes the category highly speculative because the vast majority of returns will come from capital appreciation.

If you compare opportunistic to core deals, here’s how they differ:

- Purchase Assumptions – You usually can’t assume a Cap Rate for the initial acquisition because the property might not even exist. So, the purchase assumptions are usually related to the cost of land and anything else required to start construction. Construction costs are incurred over time as the development proceeds.

- Little-to-No Cash Flow Initially – The property doesn’t exist, it’s vacant, or it’s greatly underperforming, so cash flows are anywhere between “0” and “very low.”

- Equity and Debt Draws Over Time – Most of the development costs will be incurred over time, so the sponsors draw on Equity and Debt as needed instead of paying for everything upfront. Interest on the Debt accrues to the principal instead of being paid in cash since there’s no cash flow to cover it.

- Development Costs and Time – The sponsor might have to pay for land and the labor and materials to develop or redevelop the property. These take significantly more time and money than in value-add deals.

- Ramp to “Stabilization” After the Development – The sponsor will market the property to potential tenants (or guests if it’s a hotel), sign enough tenants to boost the property to a high occupancy rate, and turn it cash flow and NOI-positive like that.

- Permanent Loan Refinancing – When development finishes and tenants start moving in, the risk profile of the property changes significantly, so the construction lenders that funded the development typically want an exit. When that happens, the sponsor raises a “permanent loan” to repay the construction loan and put in place new financing.

- Exit Assumptions – Unlike in core and value-added deals, you can’t pick an Exit Cap Rate based on the Going-In Cap Rate. So, you have to look at different potential outcomes for the market as well as what similar developments have sold for in the past.

Opportunistic deals become more popular late in the cycle when stabilized, core properties become overpriced, and it’s tougher to spot good “standard” deals.

Yes, a market crash could still be disastrous, but a completely new property could perform decently even if the market is poor.

Also, depending on the construction period, the sponsor could wait out the downturn and sell when prices begin to recover.

This graph from IPE Real Assets and Preqin sums up preferences over the cycle quite well:

The Returns Profile of Opportunistic Real Estate

To illustrate the returns profile, we’ll look at a modified version of a development model for a warehouse with two potential tenants (from the real estate financial modeling tutorial).

The parameters are:

- Property Type: Industrial

- Land: 18 acres (784K square feet) with 90% rentable square feet

- Land & Construction Costs: ~$52 million

- Annual Rent per Square Foot: $7.50 – $8.00

- Location: Calgary, Alberta

- Construction Loan – Loan to Cost (LTC) Ratio: 50%

- Construction Loan Terms: 25% fixed interest, accrued to principal; 1.00% issuance fees; no amortization; 1-year maturity

- Permanent Loan – Loan to Value (LTV) Ratio: 55%

- Permanent Loan Terms: 75% fixed interest; 30-year amortization; 1.00% issuance fee and prepayment penalty; 10-year maturity

The goal here is to finish development in one year (warehouses are simpler than offices, retail buildings, apartments, and hotels) and attract two tenants to fill 95% of the rentable area.

But we may or may not be successful, so we need to look at different cases:

- Upside Case: Both tenants move in and occupy 95% of the space; rent grows at 4% per year, each tenant has a 60% chance of renewing, there are only 6 months of downtime if one tenant cancels, and incentives are low (2-4 months of free rent). Cap Rates fall from 5.80% to 5.35% in a strengthening market.

- Base Case: Both tenants move in but occupy only 85% of the space; rent grows at 3% per year, each tenant has a 40% chance of renewing, there are 9 months of downtime if one tenant cancels, and incentives are higher (3-6 months of free rent). Cap Rates rise from 5.80% to 6.50% in a weakening market.

- Downside Case: Only one tenant moves in, so only 65% of the space is occupied. Rent grows at 1% per year, the tenant has a 30% chance of renewing, there are 12 months of downtime following a cancellation, and incentives are the highest (4-8 months of free rent). Cap Rates also rise from 5.80% to 7.00% in a weakened market.

Here are the numbers:

Scenario #1 – Upside (95% Occupancy and Improving Market):

In this case, deal and market conditions are both favorable, resulting in a 28% IRR and a 3.9x cash-on-cash-multiple:

Scenario #2 – Base (85% Occupancy and Weakening Market):

In this case, the deal does “decently,” but performs below our expectations, producing an 11% IRR and 1.9x multiple:

Instead, it’s because the cash flows fall by ~50%, but the capital appreciation component falls by ~72%, so the holding period cash flows gain a greater weighting.

Scenario #3 – Downside (65% Occupancy and Greatly Weakened Market):

This last case is disastrous because we do not manage to find a second tenant at all, which results in a (7%) IRR and a 0.5x multiple.

In other words, we lose money, earning both negative cash flows and taking a capital loss:

The spread between the IRR and multiple in different scenarios is massive, which is what you should expect in opportunistic deals: much higher risk and much greater potential rewards.

Should We Do This Deal?

Losing money in the Downside case here might be a deal-breaker… and sometimes it is.

But if we do assume that the second tenant moves in, the numbers improve, and we avoid losing money even when the Occupancy Rate is as low as ~75%.

Further work is required to assess just how likely this outcome is.

The Base and Upside case numbers seem fine and are in-line with what investors might target in those cases over a 7-year holding period.

But you could also take the opposite view and argue that the Downside case is not extreme enough since we did not change assumptions such as the development time and construction costs.

So, this is once again a strong “maybe” that could go either way based on the plausibility of these different outcomes.

Opportunistic Real Estate: Why Work in the Field?

You would like opportunistic real estate if you’re interested in finding the diamond in the rough and distinguishing between misunderstood properties/locations and legitimately bad properties/locations.

The technical and modeling work is more complex than it is for stabilized properties, but commercial real estate market analysis is still important so you can vet the more speculative assumptions.

Opportunistic deals are mostly the domain of real estate private equity firms and other “alternative investment managers,” so you won’t find much of this at pensions or endowments (unless they invest in REPE funds).

Why Invest in Opportunistic Real Estate?

Potentially, opportunistic real estate deals often even higher returns than those of equities, though the risk may be higher as well.

Unlike in the core, core-plus, and value-added categories, you do have a substantial chance of losing money here, and if it’s a brand-new development, there isn’t much downside protection.

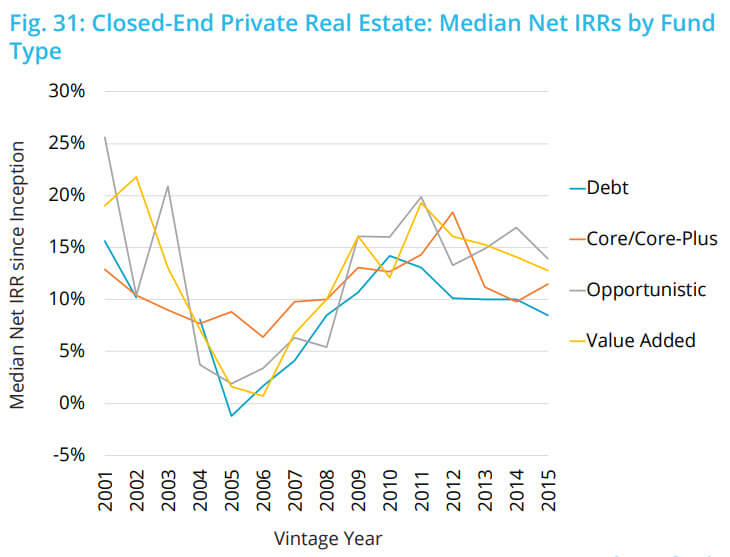

In practice, the data on median IRRs by private equity fund type from Preqin doesn’t show much of a boost in the returns in exchange for that additional risk:

By investing in a combination of core, core-plus, value-added, and opportunistic deals, you should, in theory, be able to weather downturns a bit better and still do well when the market is strong.

As with value-added real estate, I don’t invest much in opportunistic for similar reasons: there aren’t that many deals in the category available to individual investors.

Some of my funds do new property developments, so I gain a bit of exposure like that.

Another reason is that I tend to use real estate more like a “stable, cash-flow-generating asset class” than as one where I aim for outsized returns.

But if it’s done properly and fits with the rest of your strategy, opportunistic real estate can be great – as long as it looks more like Blackstone’s funds and less like WeWork 2.0.

Additional Reading

You might be interested in Value-Add Real Estate: What Makes It Different, and Why You Should Invest – Maybe.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews