Commodity Hedge Funds: The Most Lucrative “Hidden Gem” in Finance?

If you want to work in the most cyclical role in the finance industry, it’s hard to beat commodity hedge funds.

But a few related areas, such as commodity desks at banks, commodity trading advisors (CTAs), and physical commodity trading shops could put up a good fight for that “most cyclical” title.

Many of the largest hedge funds put commodity trading within their global macro strategies, but plenty of smaller funds, banks, and desks make it a separate category or focus on commodities within their macro strategies.

And since it’s both specialized and potentially very lucrative, it’s worth discussing separately:

What Are Commodity Hedge Funds, and What is “Commodity Trading”?

Commodity Hedge Fund Definition: A commodity hedge fund buys and sells futures contracts and other derivatives based on mining, energy, power, and agricultural products and earns profits via fundamental and technical analysis; the trading may be systematic, discretionary, or both.

We should also step back and define “commodities” and “commodity trading” since they’re massive areas.

Commodities are physical products that come out of the ground, are delivered in bulk globally, and are exchangeable for other physical products with similar characteristics.

There is no “brand premium,” and they may be stored for long periods, such as months, years, or even decades.

The main categories include agriculture (coffee, cocoa, sugar, corn, wheat, soybeans, etc.), power, energy (oil, gas, NGLs, etc.), and metals and minerals (gold, silver, copper, lithium, etc.).

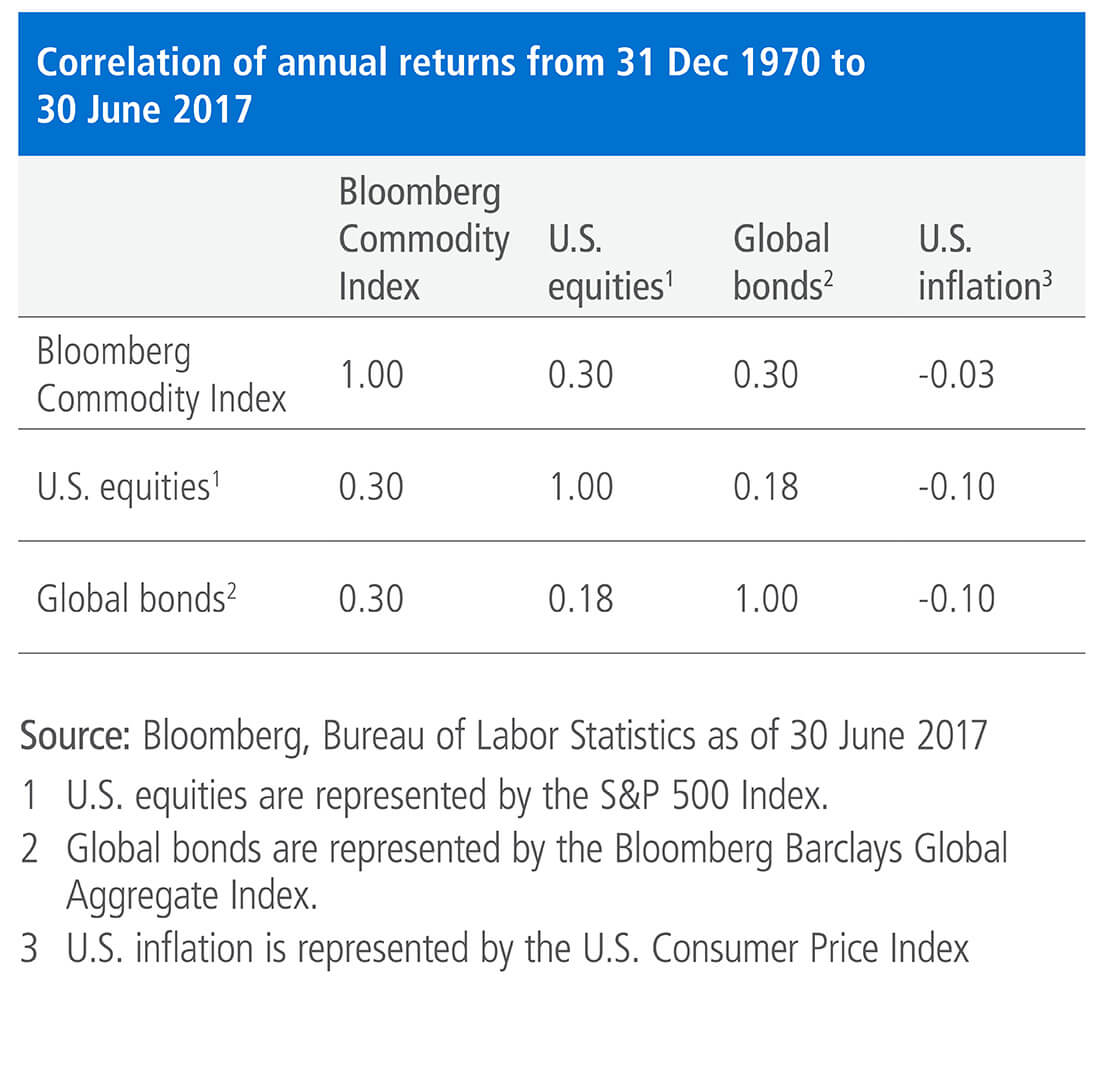

Commodity trading and investing are appealing for many of the same reasons global macro strategies are appealing: inflation protection, diversification, and potentially higher returns when financial assets perform poorly.

This article from PIMCO and the correlation data sum it up quite well:

Included within commodity trading are the following firms and groups:

- Commodity trading desks at oil, gas, mining, power, and agricultural companies.

- Commodity trading desks within sales & trading at the large banks.

- Commodity trading advisors (CTAs), which are like hedge funds in some ways (see below).

- Commodity hedge funds, either as independent entities or as part of larger global macro teams.

- Dedicated commodity trading firms such as Trafigura and Gunvor that buy and sell physical commodities and transport them globally.

There are two broad categories of commodity trading, and each firm above fits within one or the other:

1) Physical – This category is more capital-intensive and requires serious logistics and operations know-how and a wide network.

This type of trading requires you to connect buyers and sellers and ensure, for example, that oil can flow between continents without being stolen by pirates, ninjas, or evil robots.

Regional market dynamics are important here, as are your relationships with the buyers, sellers, and freighters. You focus on fundamental analysis, such as supply and demand curves, and you usually specialize in one commodity.

2) Paper – Here, you focus on trading futures, forwards, options, and swaps rather than the underlying physical commodities.

A future is a contractual agreement to buy or sell a commodity on a listed exchange in a certain quantity and quality and on a certain delivery date. As the delivery date approaches, the underlying commodity’s price and its futures price converge.

In practice, true physical delivery of the underlying commodities rarely happens, so futures trading goes in the “paper” category.

Fundamental analysis around supply and demand is still important, but you also spend time on the technical analysis, data, and everything that derivatives traders would think about.

Natural resource firms and dedicated trading firms tend to focus on physical trading, while bank trading desks, hedge funds, and CTAs focus on paper trading.

The other side might still “exist” at these firms, but it’s often a lower priority.

For example, physical traders at the oil majors often earn more than paper traders because they influence the main energy production business.

The financial traders at these companies might focus on hedging and run a few speculative trades on the side.

Examples of Physical vs. Paper Commodity Trades

To make these concepts concrete, I’ll describe three commodity trades here: a “paper trade,” a “physical trade,” and a mixed paper/physical trade.

In each one, you’ll trade wheat or its derivatives (futures or options linked to the underlying price).

You’ll be based in the U.S., where wheat futures for delivery in 6 months are currently $8.00 per bushel.

A Paper Commodity Trade

If you believe that the price of wheat will increase above $8.00 in 6 months, you could set up a “bull call spread” by purchasing a call option above this price and selling a call option at an even higher price.

Doing so limits your losses if you’re wrong but also caps your gains if you’re correct.

For example, you might buy a $10.00 wheat call option for $0.50 and sell a $12.00 wheat call option for $0.20.

These options use the wheat future itself as the underlying asset.

Each wheat future represents 5,000 bushels, so the premium to set up this trade is ($0.50 – $0.20) * 5,000 = $1,500 (ignoring commissions and other fees).

Your maximum profit is the difference between the exercise prices times the number of bushels, or ($12.00 – $10.00) * 5,000 = $10,000.

If wheat prices remain below $10.00 after 6 months pass, the options expire worthless, and you lose your $1,500 premium.

If wheat prices rise to between $10.00 and $12.00, you will profit based on (Wheat Price – $10.00) * 5,000.

And if wheat prices rise above $12.00, your profits would be capped at $10,000 because of the $12.00 call option you sold.

A Physical Commodity Trade

Now, let’s say that you’re connecting a U.S. wheat seller to a buyer in China.

Futures are currently $8.00 per bushel, the “basis” (the local cash price minus the futures price) in San Francisco is $4.00 / bushel, and it costs $4.00 / bushel to ship wheat from SF to Beijing.

So, it will cost you $16.00 per bushel to deliver this wheat to your buyer in China. You and the buyer agree to a price of $17.00 per bushel.

If you deliver 5,000 bushels, that’s a profit of $5,000.

Your value-add in this trade is that you knew the buyer, seller, and freighter and got the best quotes and delivery times from everyone involved.

Someone without your network might have been able to make this trade, but they would have gotten worse prices and earned less profit.

A Mixed Physical and Paper Trade

You could earn a higher profit from this same trade if you bet on market prices first.

Maybe you believe that wheat prices will fall by the time of this delivery in 6 months, so you decide to hold off on purchasing the wheat.

But you could be wrong, so you also decide to hedge your risk by buying futures.

You review your forward price curve and purchase some futures at $9.00 to lock in the price if it goes even higher.

A few months pass, the wheat harvest is good, and the basis in SF falls to $3.00 / bushel.

Now, you decide to lock in your profits by buying the wheat and paying for the shipping.

You also sell the $9.00 futures you previously bought; you’ll take a loss on these since wheat prices have fallen.

It now costs you a total of $8.00 (futures price) + $3.00 (basis in SF) + $4.00 (freight) = $15.00 per bushel to ship your wheat to China.

You earn $2.00 per bushel rather than $1.00, so your profit is $2.00 * 5,000 = $10,000 minus the amount you lost on the futures.

Commodity Hedge Funds vs. Commodity Trading Advisors vs. Global Macro Hedge Funds

There’s a ton of overlap in these areas since all these firms focus on paper trading.

The main difference is that global macro hedge funds pursue the broadest range of strategies since they can invest in almost anything.

Commodity hedge funds are a subset of the global macro category and focus on derivatives of the main commodity types above.

And commodity trading advisors (CTAs) are in the smallest category (theoretically) because they only trade in the futures markets, and they mostly use momentum or “trend-following” strategies.

But this description of CTAs is no longer correct because many trade futures and options on products outside of pure commodities, which raises the question of why “commodity” is still in the name.

The real difference is that the licensing, registration, and legal structure differ, and unlike hedge funds, CTAs can advise a broader group than just high-net-worth investors and institutions.

The Skills Required for Commodity Trading

You do not use traditional financial statement analysis or valuation in commodity trading because the underlying asset is a futures contract, not a stock.

The fundamentals do not relate to EBITDA, Free Cash Flow, or valuation multiples but to factors like the weather, human behavior, geopolitics, and supply and demand.

You think about these issues and commodity-specific factors, such as pipeline/plant capacity, outages, and new drilling activity for oil, to predict how prices might change.

One of the key tasks is creating a forward price curve based on your view of supply and demand. The U.S. Energy Information Administration has a few simple examples here:

Your discussions with customers, competitors, and other commodity brokers will also inform this curve.

If you get completely different views about pricing from these different sources, you’ve either made a mistake or discovered an arbitrage opportunity.

Given the amount of data analysis required, you might be wondering if it’s essential to have computer science skills for commodity trading.

CS and programming skills help but are not necessarily “essential” for all roles.

For example, on the physical trading side, most of the job consists of simple arithmetic, geopolitical/market knowledge, and sales/relationship/networking skills.

You must also consolidate information from various sources and present it effectively to build relationships and execute deals.

Coding skills are more useful for paper trading because you’ll trade based on trends, numbers, and correlations.

The Top Commodity Hedge Funds, Trading Firms, and Trading Desks

All the large, multi-manager hedge funds use global macro strategies, and some have dedicated commodity groups.

So, expect to see commodity traders at the likes of Citadel, Millennium, Balyasny, Squarepoint (quant focus), DRW (quant), and DE Shaw (quant).

If you include family offices, names like Soros, Duquesne, and BlueCrest could also be on this list.

If you consider newer commodity hedge funds with strong performance, the names might include Quantix Commodities, East Alpha (quant), Statar Capital (natural gas), Valent (renewables), Drakewood (metals), Orion (discretionary), and PIMCO’s Commodity Alpha Fund (PIMCO is not “new” and is not even a hedge fund, this specific fund launched in 2013).

The top CTA funds are harder to pinpoint because there’s so much overlap with the hedge funds, but a few larger names include Transtrend (Netherlands), Crabel Capital, Quest Partners, DUNN Capital, Quantica Capital, and Aspect Capital.

On the physical trading side are firms like Glencore, Vitol, Trafigura, Mercuria, and Gunvor in energy and metals and Cargill, Archer Daniels Midland (ADM), Louis Dreyfus Company (LDC), Bunge, and Wilmar International in agriculture.

Finally, on the investment banking side, the “top 3” banks (GS, MS, and JPM) all have a good presence in commodities, as do BofA and Citi.

Among smaller firms, Macquarie is quite strong, probably because it is based in commodity world-leader Australia.

How to Recruit for Commodity Hedge Funds and Other Trading Roles

If you want to be a commodity trader, there are three main paths into the industry:

- Start at a large bank in a commodity-related group within sales & trading. Some IB natural resource groups could potentially work, but if you want to be a trader, you’re still much better off starting in S&T.

- Join a physical trading shop or natural resource company in an operations, “scheduling,” or middle-office role with a pathway to becoming a trader. These roles are less competitive, but they also pay less than S&T at a bank, and even if you perform well, it usually takes 3-7 years to gain P&L responsibility.

- Start in trading and pivot into commodities. For example, you could start trading a slightly more accessible product (equities, options, etc.) at a hedge fund, prop trading firm, or asset management firm and then move into a commodity role once you prove yourself.

I did a quick LinkedIn survey of a few dozen people with “commodity trading” in their profiles, but it wasn’t too interesting: 80%+ had started in trading and stayed in it.

I noted the following points:

- A few people (~5-10%) had a political, legal, or compliance background, probably for the same reason that people use experience at central banks or in economics/strategy roles to get into global macro.

- Almost no one (< 5%) had management consulting or investment banking backgrounds, and the ones that did also had something closely related to commodities.

- Around 10% had wealth management experience. This one probably falls within the “pivot into commodities” category.

- Many people started out trading something else, such as fixed income or equity derivatives, and then moved into commodities.

We’ve covered sales & trading interview questions and how to get a job at a hedge fund in previous articles, so I’ll refer you to those for the process details.

Practical experience is king with commodities.

If you don’t know where to get that experience, start trading. Write your own scripts, create automated strategies, and develop tools to help traders.

No, it’s not the same as managing a P&L at a large firm, but it’s much better than applying without relevant experience.

You’re unlikely to get case studies in interviews, but you will have to discuss your trade ideas and explain your thoughts about supply/demand and forward price curves.

If you’re interviewing for a physical trading position, expect it to be more like a sales interview, where they test your presentation and networking skills.

And if you’re applying for operations or scheduling roles at companies like Glencore, expect mostly “fit” questions because they don’t expect you to walk in knowing how to connect European lithium buyers with Australian producers.

Careers, Hours, and Compensation

These points differ based on your role (Analyst vs. Trader vs. Originator) and firm type, but at a high level:

- At physical trading firms, you’ll usually start in a middle office, operations, or scheduling role. If you do well, you’ll get promoted to a front-office Analyst and then a Trader. You could stay and earn a lot if you’re good at trading or move into a management role with lower incentive compensation but more stable pay.

- Base salaries for entry-level positions here will probably be under $100K, rising to ~$150K plus a discretionary bonus once you’re an Analyst. As a Trader, you might get another base salary bump and a small percentage of your P&L.

- Traders at the largest firms could easily earn over $1 million per year, and the top traders at the oil supermajors could even earn in the 8-figure range.

- The downside is that it takes a long time to get your own book, which creates a lot of market/cyclical risk.

- On the hedge fund side, expect base salaries in the $100K – $200K range at the entry level, with a huge bonus variance based on overall and individual performance. If you do well, you could reach the high-six-figure-to-low-seven-figure range once you have some P&L responsibility. The hierarchy follows the one in the hedge fund career path article.

The hours are like other public-markets roles: expect to wake up early and arrive 1-2 hours before your market/exchange opens and leave 1-2 hours after it closes.

You’ll be busy most of the day placing trades, speaking with buyers/sellers/counterparties, following the news, and updating your positions, so there is almost no downtime.

Commodity Trading Exit Opportunities

Like the exit opportunities from global macro funds, you don’t have many options coming from commodity trading because the skill set is so specialized.

If you’re at a hedge fund or CTA, your main options are:

- Move to a different or broader strategy, such as global macro rather than just commodities. Or, if you’ve traded futures for indices or something other than commodities, join a fund that uses them as part of its strategy.

- Join a normal company in the agriculture/natural resource space that needs price hedging for its production.

- Take a trading role at a place like Trafigura or Vitol – if you can find one that’s more on the “paper trading” side since your skill set is less relevant for physical.

And there are other options, such as joining or re-joining an S&T team at a bank, moving into a risk management role, or taking a macro research role at a global organization like the IMF (see the list of sales & trading exit opportunities for more ideas).

But the bottom line is that if you want to make a dramatic change after gaining experience in commodity trading, you’ll probably need an MBA.

For Further Learning About Commodity Hedge Funds

Many of the resources in the global macro article are also relevant here, but I’ll add a few that are specific to commodities:

- A Trader’s First Book on Commodities (Garner)

- Higher Probability Commodity Trading (Garner)

- Options, Futures, and Other Derivatives (Hull)

- The World for Sale: Money, Power, and the Traders Who Barter the Earth’s Resources – More narrative than technical analysis, but great for an industry overview.

- Out of the Shadows: The New Merchants of Grain – Similar but with an agricultural focus.

- The King of Oil – Biography of an infamous billionaire oil trader.

- Trafigura White Papers – Free reports on all commodities from one of the top firms.

- CME Group Educational Materials – Market updates and overviews on all commodities.

- Trafigura – Commodities Demystified – Great overview

- Trafigura – The Economics of Commodity Trading Firms

You can find various “commodity training programs” online, but they have little value because practical experience is king.

No one will hire you as a trader because you took a course; you must show them your P&L or relevant work that supports trading (scripts, data analysis, automated strategies, etc.).

There is the Series 3 exam, which is required to be a licensed commodity broker in the U.S.

Passing this one might help on the margins, but you should still prioritize real trading experience.

Final Thoughts on Commodity Hedge Funds and Commodity Trading

For the right person, commodity trading could be an incredible opportunity.

But this “right person” has a much narrower profile than in fields like investment banking or generalist hedge funds.

The good news is that you don’t need an Ivy League or Oxbridge degree to get in or advance; if you can make money, you will move up.

You will gain a highly specialized skill set, and if you’re on the physical trading side, you’ll also gain a solid network and relationships with buyers, sellers, and transportation/storage companies.

If you leverage that correctly, you could earn just as much or more than other traders and hedge fund PMs.

And if you have no interest in networking/relationships and are more quant-oriented, you could go the paper route and do well there.

But this specialized skill set is a double-edged sword because if you spend enough time in commodity trading, you won’t have a great shot at “generalist” trading, investing, or corporate finance roles.

The other downside is that commodity strategies are far more cyclical than ones like long/short equity, credit, and even global macro.

So, if you start in a middle-office role and get promoted right as volatility falls and the market cools off, you could be in for a long stretch of difficult years for your P&L.

But if you can wait it out and make some huge trades as the next commodity super-cycle begins, you might not even remember the bad times – as large chunks of gold move from the ground to your bank account.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Finally, you made the article.

Would like to pushback on this

“Join a physical trading shop or natural resource company in an operations, “scheduling,” or middle-office role with a pathway to becoming a trader. These roles are less competitive, but they also pay less than S&T at a bank, and even if you perform well, it usually takes 3-7 years to gain P&L responsibility.”

Those roles are definitely not less competitive (I’d even go as far as to say more competitive than S&T programs) as there is a large candidate pool beyond undergrads.

You might be right. I don’t know, as I found different sources/reports saying different things, so I attempted to consolidate the main points here. I’m not sure that a larger candidate pool necessarily means they’re more competitive, though, as you also need to look at how well-qualified/prepared each candidate is and how many positions there are. I think you could argue that physical trading roles are more accessible, in that they’re not going to immediately rule out certain people, as most large banks would for S&T.