The Private Equity Career Path: The Complete Guide

- The Private Equity Job Description

- Why Work in Private Equity?

- Private Equity Skills and Career Requirements

- The Private Equity Career Path

- Private Equity Analyst Job Description

- Private Equity Associate Job Description

- Private Equity Senior Associate Job Description

- Private Equity Vice President (VP) Job Description

- Private Equity Principal or Director Job Description

- Private Equity Managing Director (MD) or Partner Job Description

- Careers Beyond the MD/Partner Level: Senior Managing Partner, COO, CEO, and More

- Private Equity Careers Pros and Cons

When thinking about the private equity career path, our favorite analogy still applies: a fraternity house.

Yes, we previously compared the investment banking career path to a frat house, and private equity careers are similar in many ways.

But if investment banking is more like a “party/drinking fraternity,” private equity is more like a “business fraternity.”

The hierarchy is a bit flatter, despite seeming similar on the surface, and it’s a more intellectual environment that demands critical thinking and risk assessment in addition to sales skills.

You still have to complete certain rituals to advance, there are still levels, and you receive added benefits as you move up – but the culture and long-term trajectory differ.

In this comprehensive article, we’ll explain the advantages and disadvantages of the private equity career path, including the work, hierarchy, promotions, lifestyle, and salaries and bonuses.

But let’s start with the basics before delving into “fraternal differences”:

The Private Equity Job Description

Private equity firms raise capital from outside investors, called Limited Partners (LP), and then use this capital to buy companies, operate and improve them, and then sell them to realize a return on their investment.

The industry is called “private” equity because the companies that private equity firms invest in are private initially, or become private as a result of the investment.

The outside investors or Limited Partners might include pension funds, endowments, insurance firms, family offices, funds of funds, and high-net-worth individuals.

Imagine that you and your friends went to all your contacts, asked for money, and then decided to become “home flippers” by buying homes, fixing them up, and selling them at higher prices.

You keep some of the profits for yourselves in exchange for operating the business, but you give the majority back to your contacts for providing the bulk of the required money.

That’s what private equity firms do, but on a much larger scale and for companies rather than houses.

The job is part fundraising, part operational management, and part investing.

For more, see our articles on the private equity industry, private equity strategies and investment banking vs private equity.

Why Work in Private Equity?

If you got the “Why private equity?” question in an interview, you’d probably say that you love investing and operations, and you want to build value for companies over the long term.

But in real life, most people are drawn to private equity because it offers high compensation, somewhat better hours than investment banking, and more interesting work.

Some people also enjoy the excitement of working on large deals and interacting with “the best and brightest,” as well as understanding company operations in more depth.

Unlike investment banking, exit opportunities are not a major reason to go into private equity because PE itself is viewed as an exit opportunity.

That said, some professionals do leave the field for hedge funds and other buy-side roles (for more, see our coverage of private equity vs. hedge funds).

Private Equity Skills and Career Requirements

The private equity career path attracts people who are:

- Competitive, high achievers who are willing to work long, grinding hours.

- Extremely attentive to detail.

- Interested in deals rather than simply following the markets or investing in public companies or other assets.

- Interested in investing and operations and using critical thinking to evaluate companies rather than selling or being an agent.

- Interested in long-term projects such as building a portfolio company over many years, and are also open to non-deal work, such as company monitoring and fundraising.

At large private equity firms (“mega-funds”), junior-level hires (“Associates”) are overwhelmingly investment banking analysts who spent 2-3 years at bulge bracket or elite boutique firms.

At smaller firms, more Associates come from middle market and even boutique banks; some management consultants and Big 4 and corporate development professionals also get in.

Firms have been hiring more students directly out of undergraduate, so there are now quite a few “Private Equity Analyst” positions in the industry as well.

Getting into private equity directly after an MBA is nearly impossible unless you’ve done investment banking or private equity before the MBA.

You could complete the MBA, use it to win a full-time investment banking job, and then recruit for private equity roles…

…but that is significantly more difficult than breaking in pre-MBA from investment banking, and it’s not an ideal path (see: more on the investment banking associate job).

To get into private equity, you’ll need:

- A sequence of highly relevant work experience, including transactions and financial modeling.

- Top academic credentials (grades, test scores, and university reputation);

- A lot of networking and interview preparation;

- Something “interesting” that makes you appear to be a human rather than a robot;

- The ability to think critically about companies and investments rather than just “selling” them.

- A strong cultural fit with the firm – PE firms are much smaller than banks, so “fit” and soft skills are even more important.

For more, see our comprehensive guide on how to get into private equity.

If you want to learn all the required technical concepts – Excel, accounting, valuation, financial modeling, and LBO modeling – from the ground up, your best bet is our BIWS Premium package, which includes several LBO and 3-statement modeling case studies:

BIWS Premium

Learn Excel & VBA, accounting, valuation, financial modeling, and PowerPoint for investment banking and private equity - and save $194 with our most popular course bundle.

learn moreIf you want to review the concepts and quickly test yourself before interviews, our IB Interview Guide includes a 120-page guide to LBO models and shorter/simpler LBO case studies:

IB Interview Guide

Land investment banking offers with 578+ pages of detailed tutorials, templates and sample answers, quizzes, and 17 Excel-based case studies.

learn moreFinally, if you have more experience, already know the fundamentals, and want complex case studies and practice models, the Advanced Financial Modeling course has an advanced LBO model and a take-home private case study example.

If you do not have the skills and work experience mentioned above, your best bet is to gain transaction experience in corporate development at a normal company or in M&A at a Big 4 firm and use that to move in.

Or, join a PE firm’s portfolio company, work on the operational side, and eventually move to the firm itself.

Do not bother with non-deal-related jobs such as equity research, or back or middle office roles.

The CFA is the only certification that means anything at all in PE; it is marginally helpful, but it plays a small role next to everything above.

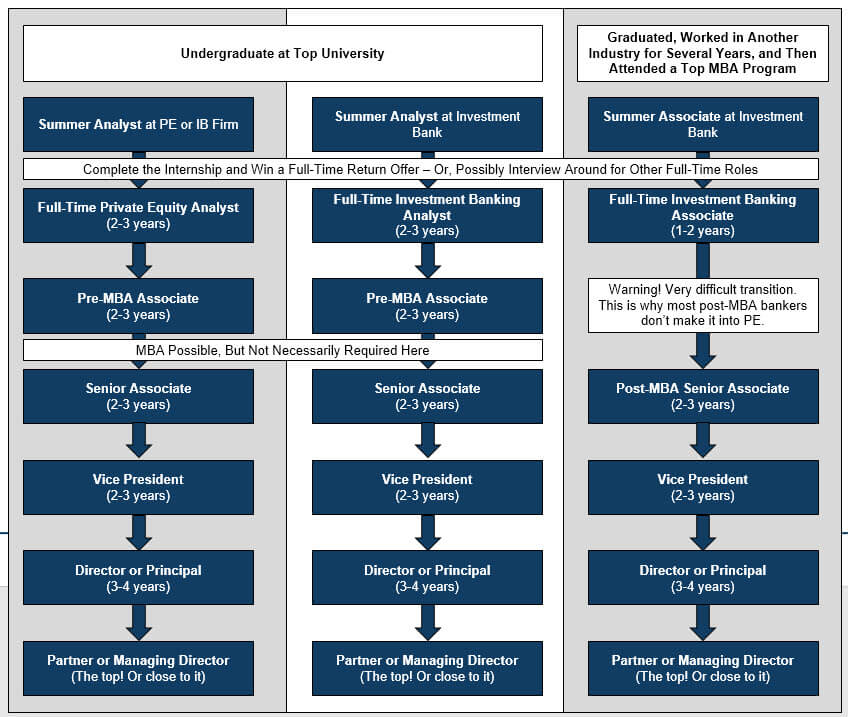

The Private Equity Career Path

The private equity career path and hierarchy vary from firm to firm, but here’s a representative example:

- Analyst – Logistical Monkey.

- Associate (Pre-MBA) – Deal and Analytical Monkey.

- Senior Associate – More Experienced Monkey.

- Vice President – Manager of Deals.

- Director or Principal – Generator and Negotiator of Deals.

- Managing Director or Partner – Rainmaker, Fundraiser, and Chief Representative.

And here’s a flow-chart summary:

We’ll look at each level in detail below, but here’s a summary of the age, earnings potential, and promotion time for each one:

| Position Title | Typical Age Range | Base Salary + Bonus (USD) | Carry | Time for Promotion to Next Level |

|---|---|---|---|---|

| Analyst | 22-25 | $100-$150K | Unlikely | 2-3 years |

| Associate | 24-28 | $150-$300K | Unlikely | 2-3 years |

| Senior Associate | 26-32 | $250-$400K | Small | 2-3 years |

| Vice President (VP) | 30-35 | $350-$500K | Growing | 3-4 years |

| Director or Principal | 33-39 | $500-$800K | Large | 3-4 years |

| Managing Director (MD) or Partner | 36+ | $700-$2M | Very Large | N/A |

We are not going to address the exit opportunities and hours/lifestyle for each level because PE is usually the end goal, and the hours don’t necessarily change much as you move up – expect 60-70 per week at smaller firms and 80+ at mega-funds.

The key differences at each level of the private equity career path lie in the work tasks, promotion time, and compensation.

Also, note that all the compensation figures below refer to figures in North America – they will be lower, sometimes significantly lower, in regions such as Europe and Asia-Pacific.

Private Equity Analyst Job Description

Private Equity Analysts are hired directly out of undergrad without previous full-time experience.

They work on the same types of tasks as Associates: deal sourcing, reviewing potential investments, monitoring portfolio companies, and fundraising, but they complete fewer projects independently from start to finish.

For example, an Associate working on a deal might build the entire financial model and coordinate the due diligence process, including speaking with lawyers, auditors, consultants, and other parties to get answers.

But an Analyst on the same deal might help only with specific tasks such as setting up conference calls, sifting through data, and assisting the Associate with certain research or documents.

Age Range: These roles are only for students who just finished undergrad, and they only last for a few years, so we’ll say 22-25.

Private Equity Analyst Salary + Bonus: You’ll almost certainly earn less than an IB Analyst in terms of total compensation; your salary + bonus will likely be in the $100K – $150K range, with the bulk coming from your base salary.

Carry, i.e., a share in the profits from investments, is unlikely-to-borderline-impossible for Analysts, so don’t even think about it.

Promotion Time: Expect 2-3 years for a promotion to Associate, if your firm promotes Analysts (it varies widely).

Private Equity Associate Job Description

Private Equity Associates must be able to lead deal processes from start to finish without step-by-step instructions.

They spend their time on sourcing – generating new deal ideas – as well as financial modeling and due diligence for active deals, portfolio company monitoring, and even some fundraising.

The PE Associate role is an evolution of the IB Analyst role, so you still spend a lot of time in Excel, PowerPoint, and data rooms – but you have more responsibility and must act more independently in those tasks.

A typical day for a PE Associate might include the following:

- Meet with their boss or other team members to discuss ongoing deals and potential ideas.

- Build a financial model for an active deal or review and tweak an existing one.

- Conduct a conference call with the owners of a private company that might be interested in selling to your firm.

- Review customer contracts in the data room for an active deal.

- Review a portfolio company’s quarterly financial results and speak with the CFO about them.

- Assist with the fundraising process by setting up webinars with potential new Limited Partners (LPs).

- Complete administrative work such as editing NDAs or conducting market research.

Age Range: You need several years of IB or a closely related field to get in, so we’ll say 24-28.

Private Equity Associate Salary + Bonus: Your salary + bonus will probably be in the $150K to $300K range, depending on the size of the firm and your performance.

Some of the large funds may pay more than $300K, but we’re using the 25th percentile to 75th percentile range as a reference here.

Carry is still quite unlikely unless the firm is brand new and you’re an early hire.

Promotion Time: Expect 2-3 years for a promotion to Senior Associate.

Private Equity Associate vs Analyst

As discussed above, the Associate tends to be more involved with the entire deal process from start to finish, while the Analyst might only help with specific tasks the Associate can’t get to.

The Associate is more of a “Coordinator,” and the Analyst is more of an “Assistant.”

Analysts are hired directly out of undergrad, while Associates join following several years in investment banking or a related field, such as management consulting.

Associates also earn more and are more likely to stay at the firm for the long term – if there’s a path to advancement there.

If there is no direct promotion path, Associates might complete an MBA or move into a different industry, such as hedge funds, corporate development, or strategy at a tech company.

Private Equity Senior Associate Job Description

“Senior Associate” and “Associate” are nearly the same.

The main difference is that “Senior Associate” is used to denote:

- An Associate who has been at the firm for a few years and been promoted directly, or

- An Associate who worked for a few years, went to business school, and then returned to the firm.

The work is not much different, but Senior Associates move closer to the VP-level, where they have more “manager” responsibilities.

Age Range: We’ll say 26-32 because at the minimum, you must have completed two years of IB or PE Analyst work, followed by two years of PE Associate work.

Some Senior Associates may be in their low 30s because they may have switched industries after undergrad, broken into IB, switched into PE, and then completed an MBA program.

Private Equity Senior Associate Salary + Bonus: These increase incrementally over the Associate level, but not dramatically so. The range might be more like $250K to $400K depending on the firm size, region, performance, etc.

At this level, a small amount of carry is more plausible. You’re not going to become a multimillionaire and retire at age 35, but it might boost your bonus a bit.

Promotion Time: You’ll need 2-3 years to reach the next level of Vice President.

It’s quite difficult to get promoted to VP because the nature of the job changes a fair amount at that level.

Many Associates and Senior Associates at larger PE firms realize there is no great path to VP there, so they end up going downmarket to advance.

Private Equity Vice President (VP) Job Description

In private equity, Vice Presidents are “deal managers.”

They need to convince the senior team members – Principals and Managing Directors – that they know what they’re doing so that the senior staff trusts them to manage deals.

VPs also lead and mentor others on the team, work more directly with clients, vet transactions, and lead due diligence and negotiations.

The VP role may sound similar to the Associate role, but it is very, very different.

Soft skills start to matter far more at the VP level, and you need to be a good talker and presenter to advance.

If you can prevent an important deal negotiation from falling through with some smooth talk on a conference call, that matters 100x more than being an Excel/VBA guru.

Very few, if any, professionals make it to this level with poor communication skills, but plenty of people with mediocre technical skills make it – as long as they talk and present well.

Age Range: The likely range here is 30-35 because you must have already spent at least ~4 years in PE at the Associate levels, you probably did something before that, and you might have gone to business school as well.

Private Equity Vice President Salary + Bonus: The likely range here is $350K to $500K, with about half in base salary and half in the year-end bonus.

Carry becomes increasingly important at this level, which could boost your bonus a fair amount – but you probably won’t see its full effects unless you stay at the firm long-term.

Promotion Time: You’ll probably need 3-4 years to advance to the Principal level.

Private Equity Principal or Director Job Description

You can think of Principals as “Partners in training.”

They have a lot of decision-making power, but they don’t have the same type of ownership in the partnership that the MDs/Partners do.

Principals leave most of the deal process management to the VPs and Associates and get involved when deals are nearing the finish line, and critical negotiations are required.

They also spend more time on sourcing deals and fundraising, and they are often the ones who convince business owners to consider a sale in the first place.

Principals also act as the go-between between the deal team and the MDs/Partners.

Age Range: It’s 33-39 here because of all the previous experience you need.

Private Equity Principal Salary + Bonus: Compensation reports indicate highly variable numbers, but the 25th to 75th percentile is in the $500K to $800K range.

Carry becomes even more important at this level and may substantially increase total compensation.

Promotion Time: It normally takes 3-4 years to reach the next level of Managing Director or Partner.

Private Equity Managing Director (MD) or Partner Job Description

Private Equity Partners or Managing Directors are the king of the hill.

They spend their time on fundraising, deal origination, and “fund representation,” which could mean attending events and conferences, speaking with LPs, and doing everything required to boost the firm’s brand name and reputation.

They still spend some time reviewing deals, but they are less involved than the Principals unless it’s an extremely important deal.

Unlike the other roles here, this one depends 100% on human relationships – not Excel, VBA, Python, or small details in documents.

That makes it the toughest job because it’s much harder to address LPs’ concerns and convince them to invest in your new fund than it is to write an Excel formula or lead a deal process.

Oh, and one more thing: MDs and Partners must also invest a significant amount of their personal wealth into the fund to ensure they have “skin in the game.”

So… if you’re a risk-averse person, this is probably not the role for you.

Age Range: You’re unlikely to reach this level before your mid-to-late 30s, so we’ll say 36+. But that’s just the minimum – most Partners are likely in their 40s or beyond.

Many MDs and Partners stay in private equity indefinitely because there’s no reason to leave unless they’re forced out or the firm collapses.

Private Equity Managing Director Salary + Bonus: Compensation here is highly variable, but a reasonable range is $700K to $2 million, with slightly less than half from the base salary.

“Senior Partners” will earn more if the firm makes the distinction.

But carry is the key driver at this level and could increase total compensation by a multiple of the range above.

For example, the senior professionals at firms like Blackstone could earn tens or hundreds of millions per year (!), largely due to carry.

However, you should keep your expectations in check: the average case for total compensation at mid-sized and smaller firms is in the low millions if you make it this far.

Promotion Time: N/A – this is the top of the ladder.

Careers Beyond the MD/Partner Level: Senior Managing Partner, COO, CEO, and More

Some firms distinguish between normal Partners and “Senior” ones; Senior Partners own a higher percentage of the partnership, earn more carry, and have more decision-making power.

At the private equity mega-funds – the likes of Carlyle, Blackstone, and KKR – there are also C-level executive positions in the hierarchy.

There is no set path for advancing into these roles, so it depends on timing, performance, and who’s planning to retire.

We’re not covering them here because there’s little tangible information about these roles, and most students and professionals won’t even make it midway up the ladder.

Private Equity Careers Pros and Cons

Summing up everything above, here’s how you can think about the trade-offs of the private equity career path:

Benefits / Advantages:

- High salaries and bonuses at all levels, with the potential for carry to boost senior-level compensation far beyond what investment bankers earn.

- More interesting work than investment banking and other sell-side roles.

- Somewhat better hours than investment banking, at least at mid-sized and smaller funds, and a more predictable schedule… if you’re not working on a major deal.

- Direct exposure to different companies, industries, and management teams, and significant responsibility even at the junior levels.

- Firms are small, so advancement is directly linked to your performance; office politics is less of a factor than at large banks.

- The industry is unlikely to be disrupted by technology because it’s a relationship-based negotiation and sales role at the top levels.

Drawbacks / Disadvantages:

- Still fairly long hours and an intense work environment, and significant travel may be required, especially as you advance.

- There may not be a clear path to advancement at your firm, depending on the firm’s size and policies and your level. And even if there is a path, advancement can be challenging because Partners rarely get “burned out” and leave.

- You could end up doing a lot of cold calling, research, or portfolio company monitoring rather than deal execution – and even if you do work on deals, you’ll be lucky to close ~1 major transaction per year.

- You won’t gain the same network or structured training that you would at a large bank because PE firms are so much smaller.

- You will have to contribute a significant portion of your net worth at the top levels, which is fine if the fund performs well… but a big issue if it struggles.

- It’s extremely tough to get into the industry if you get a late start, you’re a career changer, or you did not attend a top university and then do investment banking.

So, is private equity right for you?

Rather than assuming that it is because “everyone” does the investment-banking-to-private-equity-path, you should consider these factors and be honest about what you’re looking for in a long-term career.

If you want more of a “business frat” than a party/drinking frat, then a private equity career could deliver.

But if you don’t want to be in the frat house at all, you’ll need to consider strategic alternatives.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Hi , just want to confirm if its possible to break into PE by using CFA or CAIA without going to Ivy league schools?

As mentioned repeatedly on this site, PE firms do not care about certifications like the CFA or CAIA. They care about your work experience (specifically the deal or client experience you have) and other factors such as your university/MBA, grades, and so on.

So, no, the CFA is not equivalent to attending Harvard or Oxbridge and never will be. It may provide a modest boost for some finance roles, but it rarely, if ever, helps you much for PE. If you don’t have deal experience from a role like investment banking or corporate development, work on getting that first.

https://mergersandinquisitions.com/investment-banking-certification/

https://mergersandinquisitions.com/how-to-get-into-private-equity/

Hey, so I completed my MBA recently after engineering from a top B-School and ended up in Bain. Is it difficult to land myself into PE roles? If so, may I ask why is it the case? Especially up until few years ago PE firms would hire management consultants from top firms to PE. The IB –> PE trend is a more recent one. To add to that, PE firms anyways hire an investment bank, why do they still need bankers on their team as compared to management consultants who may have more business knowledge than IB role people?

It is generally difficult to win front-office, investing-based PE roles coming from consulting. Yes, some consultants do get in, but if you’re in the U.S., probably ~90% of people in PE have an IB background because there’s more of a clear skill set match since you work on deals and build models and conduct due diligence in both industries. IB to PE is not a “more recent” trend – PE firms have been hiring bankers for decades since is is the ideal feeder ground for PE.

PE firms usually hire banks to arrange the financing or to market portfolio companies they want to sell. They don’t hire them in buy-side advisory roles nearly as much. And they need people with IB experience to crunch the numbers and do quick assessments of whether companies are a good fit. Most consultants don’t have this skill set because much of their work is fuzzier.

If you want some tips on going from consulting to PE, please see: https://mergersandinquisitions.com/consulting-to-private-equity/

You could also consider operations teams at PE firms if you want to go this route.

Hi Brian, I have 6.7 years Big 4 management consulting experience (primarily in insolvency and company restructuring), a little under two years in banking but in risk and compliance and currently in a new job with one of Africa’s largest telecommunications companies in enterprise risk management. Actively in MBA application stage and the current plan post-MBA is to work in M&A for 2-3yrs then eventually find my way to PE. You said age really isn’t a factor that operates as a barrier to entry but rather a lack of pre-MBA PE experience. I turned 30 two months ago (which isn’t old old by definition) but I can’t help but feel like I may be setting too much of an unrealistic timeline of events for myself. I would love some realistic guidance. Thank you.

You can always get into PE from a post-MBA IB role, but it is more difficult and will require a lot more networking and focusing on smaller firms. So, I think it really depends on how much effort you want to put into it. If you have a burning desire to do it and stay in the industry for 10+ years, sure, maybe. If you’re doing it just because it’s the thing to do, you could easily get a corporate development job after IB, still earn a good amount (though much less than in PE), and get more of a life outside of work.

Thanks for your time, really appreciate it!

Hi Brian.

Thanks for this detailed article.

Responding to this from London, England.

I am seeking to break into PE. From my research, I have realised that internships are my way in. Would you suggest I continue to apply for PE off cycle internships? Would you have any guide to help me solidify my interview skills? Am I too ‘old’ to change careers?

I just finished an MBA from Imperial College and come from a software engineering background with over 6 years work experience in finance.

It is normally very difficult to go from an engineering background + MBA directly into PE because all PE firms want people with previous deal experience. So, in practice, most people who get in have done PE pre-MBA or IB or even something like corporate development.

I think your best move here would be one of the following:

1) Aim for IB roles and target tech/TMT groups to leverage your background. You could potentially apply to the large banks, but it might be hard if you’ve already finished the MBA, so maybe you should focus on boutique and other smaller firms and see if something opens up there.

2) Use your background to apply to smaller VC firms that might be interested in someone with a SWE + MBA. If you gain some experience at VC firms, you could potentially find an easier path into IB or PE in the future.

But the bottom line is that it’s not really about your age, but the fact that you have a lot of unrelated experience for a very competitive role. And I think you would need something deal-related first to have a good shot. Another option might be consulting since some PE firms hire consultants, but I’m not 100% certain how common it is to go the consulting –> PE route in the UK.

Brian – Great article. I will be going into Corp dev upon graduation from Villanova this May. However, I was looking to transition into PE after a few years in Corp dev. How likely is that transition? What size firms should I be targeting? I’ve been hearing I should be targeting smaller firms that focus the industry of which my corp dev company is in. Any comment or suggestions?

It’s possible but not that easy because PE firms still prefer bankers. Take a look at some of the corp dev articles on this site for more. Yes, you should target smaller funds that focus on your company’s industry. You are highly unlikely to get into KKR, Blackstone, etc., coming from a CD role out of undergrad with no IB experience at a large bank in between.

Do you think being a hedge fund senior portfolio manager or a managing partner in a private is more lucrative? Assuming if both person situated in fund has the same exact amount of AUM.

Depends completely on the fund’s performance and your time frame. The advantage of HFs is that if you have a great single year, with NAV above the high-water-mark, you can get a huge bonus in that single year from the carried interest. PE carried interest takes much longer to pay out because you need to buy and hold companies and eventually exit them. But it’s arguably more “stable” income if your fund performs well.

Hi Brian,

great article. So doing the math it looks like partners and principals at top PE firms average something like 5-10M annually (!), supposing that they receive 20M-30M in carried interest each 5-7 years. Is that right?

I am surprised because this is much more that what quant PMs make, isn’t it? Like 5-10x. So how come that people keep saying that the HF and PE pay is comparable?

You’ve left repeated comments on various articles of this site asking about compensation details, so I am not really sure what you’re looking for at this point. Yes, it is possible to earn in the $5-10 million range as a Partner at a top PE firm… but very few people make it to that level, it’s highly dependent on performance, and you may not see any carried interest for 10+ years, making the cash figures in the current year far lower.

People say that HF and PE pay are comparable because the “average case” in either one at mid-sized funds is similar (low millions per year and lower at smaller/start-up funds).

Carried interest is rarely factored into compensation reports because it’s not a sure thing, unlike base salaries and bonuses. It’s highly dependent on performance, avoiding blow-ups, and actually staying at the fund for 10+ years, which most people do not do.

Question as someone who is an international student in Venture Capital (1st year analyst) looking to break into PE in the USA thru an MBA (rationale: no visa, so use top MBA to get visa and become “US attractive”)

Which of the following three tracks would you recommend (first two not in your diagram):

1. VC analyst local > IB analyst local > Top US MBA > USA PE (have you seen this pre MBA-IB to post MBA PE? Again, reason being visa, hence MBA)

2. VC analyst local > PE Local (if possible) > Top US MBA > US PE

3. Or still try the “difficult” VC/whatever else > Top US MBA > IB Associate > PE associate

The rationale here is that it’s easier to get into IB/PE in my country so wanted to know if it would look better to break-in at the pre-MBA level.

#1 and #2 are better if your eventual goal is PE. I don’t think there is a huge difference between them. If it’s easier to get in in your country, yes, do it there because it’s much harder to get in at the MBA level without previous pre-MBA experience. I wouldn’t recommend #3 because it’s less direct and VC straight to an MBA isn’t necessarily the best background for that.

You mention that it can be very tough to break into PE if you don’t have investment banking experience. I have sales and trading experience (macro), do you think this could be used as a way to break in, or can i at least spin it a certain way to try?

Traditionally, it’s very difficult to move from S&T into PE because you don’t have deal experience. But you might have a chance if you can find some type of PE firm with more exposure to macro factors (maybe something commodities-related?). Honestly, you should probably move into IB or get related deal experience before you try to make this type of move.

Hi Brian,

Great article, thank you. You mentioned that the work is interesting in PE. I work in IB and I don’t find the work interesting at all, so wanted to ask how much more interesting the work in PE really is, as am debating over whether making the move to PE is right for me.

Thanks,

Bass

It depends on what you find boring. If you fundamentally don’t like analyzing companies’ financials or picking apart their business models, don’t do PE. If you do like that, but don’t like all the useless nonsense like fixing fonts and formatting in huge presentations that no one ever reads, then PE may be better for you.

Thank you for this article. It is very helpful. What is the career path if you work for a private equity team within an insurance company?

I don’t know, but I am assuming that compensation is quite a bit lower and that the path to the top is also slower. There isn’t much survey data on PE at insurance firms.

Are there any specific articles or insights on joining a lower middle market private equity firm (~$250m – $500m Fund size) and the potential career trajectory?

https://mergersandinquisitions.com/off-cycle-private-equity-recruiting/

Hi Brian,

I am actually transitioning into a LMM PE firm and wanted to know if their was any information detailing the career trajectory post 2 year associate role?

We don’t have anything more detailed on LMM PE specifically.

A little bit of topic here but if someone that goes to a non target school is possible for them to get into investment banking and then get into PE? Do you have to work for a top investment bank to get into PE?

It is possible, but your chances go down if you’re from a non-target school and you also work at a bank outside the top tier. See: https://mergersandinquisitions.com/off-cycle-private-equity-recruiting/

If I was to get a masters in finance from like a USC or a Santa Clara right after I earn my Undergrad degree at USFCA, do you think that I would be able to get hired on as a PE analyst with no work experience in PE? Also, do you think that its likely to move up in PE with a Masters in Finance instead of an MBA?

Neither of those is a target school, so this is highly doubtful. You are at a big disadvantage trying to get into PE without a brand-name school and IB experience, no matter what you do. Moving up is less about degrees than it is about getting in and performing well on the job.

“…the hours don’t necessarily change much as you move up.” – Is this really true? I would not expect that principals and partners at mega-funds are pulling 80-hour weeks. If true, I think this makes PE a much less appealing long-term career.

They’re not necessarily “working” 80 hours per week, but they are always on call, especially when major deals are closing. It is a 24/7 job, just like IB, because when a deal is in motion it’s difficult to stop until it closes.

Hi Brian, thanks for the very insightful content. All else equal, how much of a haircut (in rough % terms) would a Private Debt group take vs the datapoints above? Mostly trying to figure out for Associate – VP levels. Apologies if this has been covered elsewhere.

Please see: https://mergersandinquisitions.com/direct-lending/ https://mergersandinquisitions.com/mezzanine-funds/

Hi Brian – thanks for the sharing.

How much more useful are MBA/CFA/CAIA to a PE analyst straight out of college? Or do these only matter for individuals trying to break into the industry?

And if you could rank the above three in terms of relevance.

If you get into PE directly out of university, none of these certifications really add much or mean anything. Some firms might require you to complete an MBA to advance, so that’s the only one that could potentially be useful… but a lot of firms don’t even care about it anymore. The CFA, CAIA, and anything else that starts with a “C” are all useless if you already have direct work experience in the industry.

How did you get the compensation numbers for each position? Is this the most recent figures for the Private Equity industry? And do you have any compensation figures for impact investing?

You can find compensation reports online. These figures are as of last year, so fairly recent. I have nothing on impact investing, sorry.

Is your 25th percentile salary number applicable for, say a firm of 8-10 people, or is that below the 25th percentile? I don’t know how firms rank in terms of size and comp. Thanks!

Depends on the AUM more than the headcount. It’s plausible to earn $150K total as an Associate at a smaller firm.

if i complete a msc then work into IB and exit to PE

do i still have to do an MBA to move up the ranks

Depends on the firm, but usually no.

How often do you see associates / senior associates move into the corp dev world as a manager or director, if they decide the VP+ life is not what they want (mainly due to increasing travel requirements / desire to work a little less)?

Joining at the Director level would be difficult because you normally need a track record at the company to do that. Manager is more feasible.

Thank you for the article. I am currently in the recruitment process for the Analyst role at MM PE firm where analysts get solid deal experience alongside the usual sourcing and logistical work and routinely get promoted to Associate. I was curious how difficult you think it might be to recruit for roles at a larger fund from a top MBA program after doing 4-5 years Analyst–>Associate at the smaller fund. I understand MF’s are a longshot but what about moving from a ~$1B fund to a ~$5-10B fund?

Sure, that’s doable, but I’m not sure why you would need an MBA for that. It’s not really necessary if you’re already in the industry.

Great article –

You mentioned the difficulty in entering into PE post MBA. I am a bit of a square peg – round hole. I am considering moving into IM/PEfrom a successful career as in house counsel. I started off doing IM law, negotiating ISDAs and derivatives related work with asset management firms like Franklin Templeton at a top 10 global firm before transitioning in house as a general counsel at a engineering company. Lately I’ve noticed much of my job satisfaction derived from negotiating and closing big deals, and less from the legal aspects. I have the MBE scores to get into a top tier MBA program. Is my uniqueness a benefit or a burden in this field?

It tends to be extremely difficult to move directly from law/legal roles into a front-office investing role in PE because the skill sets don’t overlap that much (less so than in corporate law and IB, for example). So, if you want to do this, you’ll probably have to get into IB first, possibly through an MBA program, and then move into PE from there. You might be able to find a smaller/newer firm that goes for your background, but it’s still tough because all the usual objections will come up (do you know finance, can you run a deal from start to finish, can you coordinate with 5 other parties to do something, etc.).

Hi, some shops in Asia use a title called “Investment Manager”, where does it fall in the hierarchy? The job description sounds like a combination of the Senior Associate and Vice President roles. Thank you.

Yes, it seems like a combination of Senior Associate and VP from what I could see in recent job postings.

What strategic alternatives should someone consider if they dont wanna be in the frat at all?

Corporate development/finance/strategy at big companies, maybe venture capital, join a startup, etc.

Hi Brian,

Thank you for your prompt response. I actually do work for a PE backed company. So are you saying there is a chance to get into PE if I did work for a PE backed company? Overall, I have about 12 years of accounting work experience. I think there is a big challenge to get into PE a Manager level. I would probably need to take a step back.

I assume you work in PE? You’re so knowledgeable!

If you have 12 years of accounting experience, you are unlikely to get into private equity. It’s an industry where you can get in at the entry level or at the top level, but where it’s very difficult to get in at the mid-levels because they only want people with previous PE experience. You might be able to get a non-investing/non-deal role in private equity, but probably not the roles described here.

Hi Brian,

Wow – awesome article. It’s basically cliff notes 101, you hit all the points. Thank you for sharing! I wish i started in investment banking and work my way to PE. Like you said in your article might be too late to start since I am far along in my career. I am a CPA, work in corporate accounting as a manager. Started in public accounting as an auditor. I think my technical skills can transfer over and i can pick up, learn and adapt to more depth financial modeling; but the soft skills such as the sales aspect of it is what I think I lack. The idea of evaluating a firm is super interesting to me. Accountants usually come in after the acquisition is made and handles all the accounting/on boarding from there. The comp in PE is very attractive!!

It’s tough to say without knowing the number of years of experience you have, but it’s generally quite difficult to move from accounting to PE because the skill set doesn’t line up as well as you think – since you don’t work on company-wide transactions in accounting/auditing (at least, not the entire process from beginning to end). Your best bet might be to join a PE-owned portfolio company, advance up the corporate finance hierarchy, and try to move into PE from there.

Hello,

Thanks a lot for this article again.

I still have a question, if I achieve to work within a BB bank, does my non-top tier Business school, matter?

Thx

Yes, it will be a big problem. You can still get into IB, but a BB bank will be a challenge. See: https://mergersandinquisitions.com/mba-investment-banking-recruiting-process/

Thank you. Sorry I was meaning, If I achieve to get an IB, will my educational background still be an issue if I want to work in PE after ? Maybe my non top-tier BS will be erased by the brand name of the BB ?

I will be over with my master in management at 24 and a half, if I had a Msc from a top-tier I will be 27 at the end … It seems to be very late to enter in the industry/labor market

I don’t know what you mean by “achieve to get,” but if your question is, “If I win a job offer in IB, work in IB, and then want to move into PE, will my non-top-tier business school be a problem?” then the answer is “maybe.”

PE firms are prestige-driven and definitely care about the names of the schools and firms you worked at, but it may not matter quite as much at the post-MBA level as it does for undergrads (see: https://mergersandinquisitions.com/private-equity-recruitment/).

The bigger issue is that it’s quite difficult to win PE offer at all as a post-MBA IB associate.

Hi Brian,

It was an absolutely amazing article. I am curious to know if MDs would share losses of the investments and in that case can their share of carry be negative? Also are bonusses and carry used interchangeably for MDs or they are paid separately?

Yes, it’s possible to lose money if an investment does poorly. It won’t always happen (depends on the deal terms, how poorly the investment goes, etc.), but it is possible, which is one of the main risks in buy-side roles.

Carry is different from normal annual bonuses. Normal annual bonuses aren’t linked as directly to long-term investment performance and are more about AUM and the fund’s performance in a given year.

Hi – terrific article. Thanks so much. Question: There are BB PE (KKR/BX) firms offering secondary PE summer analyst positions with likelihood of FT hire. As a full-time secondary PE Analyst I am told that hires will work secondary, coinvest and will do the same modeling as an IB analyst. Is this true and can one go to a top B-school and then switch over to regular PE? Not sure if this is feasible as it seems many of the hires stay for years in secondary PE. Should one just go the IB route to regular PE, or go the secondary BB PE route to MBA and then off to regular PE. Long question, but have not seen anything on this anywhere really. Thank you!

I don’t think that’s really true, as it’s normally difficult to switch from secondaries / funds of funds work into traditional PE. Also, most of the large PE firms are going to come out of this crisis in very poor shape. I expect compensation and hiring to fall significantly as portfolio companies fail and the traditional business model breaks due to the pandemic. So it’s probably even less of a good idea than usual to go into PE right out of undergrad, and IB will hold up better because companies always need to borrow, ask bankers for advice, etc.

I know that MDs in both IB and PE are relationship-driven jobs that require winning clients/investors, managing many parts of deals and people, etc. But what is the difference between IB and PE MDs/Partners besides winning clients to your bank vs. winning investors to your firm? They seem like very similar roles at this level. Are there any detailed differences in the day-to-day that differentiates the job responsibilities outside of the core function of the business (i.e. investing vs. advising)?

And to that end, what would you say would be the telling factors of whether someone would prefer IB or PE as a long term option.

The roles are similar, but MDs in PE are still more analytical because they weigh in on all investment decisions, while MDs in IB are more sales/relationship-focused because they’ll do any deal that generates fees.

I don’t think you can really tell upfront which one you prefer until you do internships in both and see them firsthand. But if you think your IQ is higher than your EQ, PE is probably better (and vice versa for IB).

Hi Brian,

Great article. When you say, “Many Associates and Senior Associates at larger PE firms realize there is no great path to VP there, so they end up going downmarket to advance,” do you mean that they move to smaller PE firms and become VPs there? Do smaller PE shops often get their VPs from associates at megafunds?

As a follow up to this, how often do you see the opposite situation, where an associate at a smaller PE firm moves to a megafund after a few years or after an MBA? Thanks in advance.

It is definitely harder to move in the other direction, but it happens… they’d still rather hire you over someone with 0 PE experience. But prestige and reputation are real factors in the industry, so the mega-funds can afford to be picky with their hires.

Yes. I wouldn’t say “often,” but it happens a fair amount.

Excellent write-up. One of the major concerns I have about PE is the seeming lack of job security and advancement opportunities, as touched upon in the article. I want to know greater detail on this point though. Is it possible that you could be an above average performer, but simply not end up making it? My concerns lie with the factors you can’t control. Is it common for people to be left jobless somewhere in there career, and are forced to move to a much lesser-known/worse paying firm/industry? Is IB better suited for someone who is dedicated but more risk-averse like me? If I was a partner at a large PE firm, I’d be pretty confident investing my own money, but my risk aversion lies not within the job, but for the job itself. I guess my question boils down to: is it really common/easy to be laid off, despite somewhat decent performance, and end up getting screwed career-wise? Thanks.

Thanks! Yes, it is very possible to be “above average” and simply not make it up the ladder at a certain fund. It depends on timing, performance, the org structure, whether or not the fund is expanding, and so on. I have seen and heard of many people who go to mega-funds or upper-middle-market funds and then either move out of PE or move to smaller funds to advance.

I don’t know if it’s “common,” but it definitely happens, and it is one downside of the career. Advancing in IB is arguably easier because bankers get burned out and few people want to stay in the job for life, so there’s higher turnover.

Yes, I would say IB is a better bet if you’re dedicated but more risk-averse.

I don’t think it’s common / easy to be officially “laid off” in PE, but it is fairly common to figure out that you’re not going to advance up the ladder at a specific firm. Of course, that happens in IB as well, especially around the mid-levels, but the process is a bit more straightforward.

Thank you for the insights and this article. I think compensation is often a highly discussed factor in this job, and ramps pretty significantly in this industry. For instance, at my middle market PE firm (bit over $10bn of total money raised), analysts get squarely in the bracket you listed, but senior associates get $450k all in.

Yup, and it could go even higher than that. But remember that we are trying to represent the *range* of different PE funds here, not just the bigger ones. Compensation reports show a wide range of salary + bonus levels, even for Associates and Senior Associates. So, our approach is to use the 25th percentile to 75th percentile of the range, which means that the numbers will probably be lower than what bigger funds pay.

Useful article – though I must say I disagree with parts of the job description for the Analyst role. Based on my knowledge of the analyst role at several mega/upper mid market funds:

– Analysts are almost never involved in fundraising,

– Analysts are usually responsible for the the bulk of the modeling work, most of the time associates / senior Associates just check it.

Having experienced it I found the job very stimulating from an intellectual standpoint, far from an « Assistant » job :) but it is true that the Associate still coordinate the deal process and the advisors.

Yes, that may be true, but we’re attempting to cover the Analyst role at a wide range of funds here, not just bigger ones. And at smaller ones, Analysts will do more of the logistical tasks and less of the modeling work.