The Full Guide to Direct Lending: Industry, Companies & Careers

Hardly anything in the modern finance industry is truly “new,” but direct lending might come closest.

Private debt markets have always existed, but direct lending – a specific subset of private debt – took off in a major way after the 2008 financial crisis.

As the large commercial banks stepped away from lending to middle-market and lower-middle-market companies, due to new regulations and economics, “alternative lenders” stepped in to fill the gap.

And in the process, they created a sub-industry that blends elements of private equity, mezzanine, and traditional bank lending.

Table Of Contents

- What is Direct Lending?

- Direct Lending Recruiting & Ideal Candidates

- Direct Lending Fund Interview Questions and Answers

- Direct Lending Case Studies and Modeling Tests

- Direct Lending Jobs: Deals, Work, and Hours

- The Top Direct Lending Funds

- Direct Lending Salary + Bonus Levels

- Direct Lending Exit Opportunities

- Is Direct Lending Right for You?

- For Further Learning

What is Direct Lending?

Direct Lending Definition: Direct lending funds provide loans to middle-market companies that are originated and held by the lender rather than broadly syndicated; they are typically illiquid, senior secured loans with 5-7-year maturities and floating coupon rates, and returns expectations are in the high single digits to low double digits.

Just like private equity funds, direct lending (DL) funds raise capital from outside investors (Limited Partners) and then charge a management fee and incentive fee (carry), with a hurdle rate requirement to earn the incentive fee.

Unlike commercial banks, DL funds are unregulated, which means they can take higher risks and pursue deals that large commercial banks would reject or ignore.

Often, the financing required for middle-market M&A and buyout deals is in the “grey zone” for banks: it’s too large for the bank to fund directly but too small to be worth syndicating (i.e., splitting up the issuance and selling it to other investors).

So, instead of negotiating with several banks for a $150 million term loan, a company might find a direct lender that can fund the entire loan and complete the process quickly.

DL funds can also make deal processes more efficient by reducing the number of parties involved and the risk of leaks about the deal.

They’re often willing to lend up to higher multiples of EBITDA (e.g., 4.5x or 5.0x rather than 4.0x for a Term Loan)… in exchange for higher interest rates, of course.

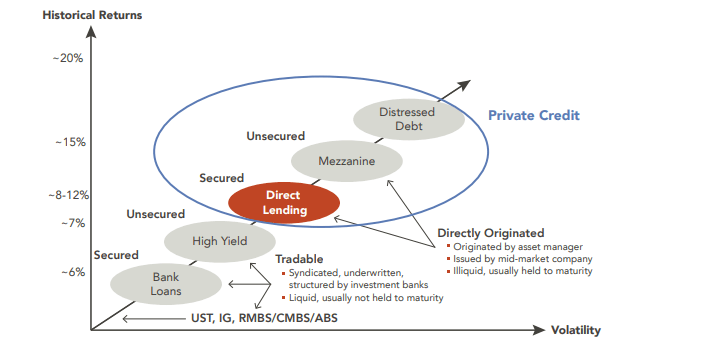

I’ve used this image before, but this graph from Marquette Associates sums up various credit fields quite well:

Direct Lending vs. Private Debt

These terms are often used interchangeably, but private debt is broader and includes direct loans, mezzanine, and forms of distressed debt.

“Private debt” means that the loan is funded directly by one investment firm rather than being syndicated and sold to many investors, and that that one investment firm plans to hold the loan until maturity.

Also, as the name implies, private debt is not publicly traded, so its market value is more difficult to determine.

But the terms, risk, and returns expectations for private debt vary widely, and distressed debt, at one end of the spectrum, is not comparable to the average direct loan.

Direct Lending vs. Leveraged Finance and Debt Capital Markets

The main differences here are:

- LevFin and DCM loans tend to be widely syndicated, i.e., the bank underwrites the loan, divides it, and sells it to a group of lenders called “the syndicate.”

- Direct lending funds are raised from Limited Partners such as pensions, endowments, and sovereign wealth funds, and they charge these LPs management and incentive fees. But if a bank holds a loan directly on its Balance Sheet, it’s funded by the bank’s deposits and debt, and the bank earns a small fee on the amount raised, with no incentive fee.

- Loan sizes tend to be smaller because direct lenders focus on middle-market companies.

Career-wise, direct lending is “better than DCM but not as good as LevFin.”

The work is more interesting than DCM since you get modeling and credit analysis exposure rather than constant market update slides.

But it’s still perceived as less modeling-intensive than LevFin or M&A or strong industry teams, and you’ll have fewer exit opportunities than in one of those.

Direct Lending vs. Mezzanine

The business models of direct lending funds and mezzanine funds are quite similar: raise money from outside investors, invest directly in issuances from companies, and charge a management fee and incentive fee.

But the risk and potential returns differ significantly:

- There is rarely equity participation with direct loans, but it’s common with mezzanine.

- Both types of loans may charge commitment fees, prepayment penalties, and other fees, but these fees tend to be higher for mezzanine.

- Capitalized or “Paid-in-Kind” (PIK) Interest is rare for direct loans but common for mezzanine.

- And direct loans are secured and have floating interest rates, while mezzanine issuances are unsecured and have fixed rates.

- Finally, mezzanine tends to fund the “last debt required” in deals, such as taking a company from 4x Debt / EBITDA to 5x Debt / EBITDA, while direct loans are used for funding up to that initial 4x.

Direct Lending Recruiting & Ideal Candidates

Credit-related groups at the large banks work well if you want to break into direct lending. Think: Leveraged Finance, Restructuring, and M&A and industry teams with solid deal flow and debt-related deals.

Capital markets groups, such as ECM and DCM, are not great options because you don’t get much modeling exposure.

Areas like corporate banking, commercial banking, credit research, and credit rating agency work are in the “maybe” category: yes, you do credit analysis, but you don’t necessarily work on the types of deals that direct lenders execute.

If you’re working in one of those fields and you want to move into direct lending, you would boost your chances significantly by winning an IB role first.

It is possible to break in straight out of undergrad, especially if you’ve had credit-related internships at banks or other investment firms.

However, it’s not necessarily the best idea for the same reasons that private equity right out of undergrad may not be ideal: you limit your options and may not get meaningful work.

Recruiting tends to follow the off-cycle pattern at the smaller direct lenders and the on-cycle pattern at larger groups attached to the private equity mega-funds.

So, if you want to work at one of the huge funds doing direct lending, you’ll need to be prepared for headhunters and recruiting long in advance of the start date.

But if you’re fine with going to a smaller fund, you can take your time, network around, and join when they’re ready to hire someone.

The interview process is the standard one for any finance role: an HR phone screen or HireVue, a phone or video interview with an investment professional, and then a Superday with 3-4 people at the firm, possibly including a case study or modeling test as well.

Direct Lending Fund Interview Questions and Answers

Interview questions for DL roles can be summarized as: “Take the mezzanine fund and corporate banking articles and make sure you know the interview questions listed there.”

Since the questions are so similar, we’re not going to repeat everything here – but we will present a few of the most common fit and technical ones:

Walk me through your resume / tell me about yourself.

See our walk-through, guide, and examples for the “Walk me through your resume” question.

You can put more of a “lending” spin on it by saying that the capital structure element of deals interests you most, and you want to work on that specific aspect.

What do direct lenders do?

They provide loans to mid-sized and smaller companies that are directly originated with no or minimal syndication. The loans are senior secured with 5-7-year maturities and floating interest rates, and direct lenders typically hold them until maturity.

The direct lending market exists because large banks stepped away after the 2008 financial crisis, partially due to new regulations and partially due to economics and industry consolidation.

Why direct lending rather than private equity or mezzanine?

You want to work on and close deals rather than looking at dozens or hundreds of deals and rejecting most of them right away, as in PE, and you like assessing companies’ credit risk.

You prefer direct lending over mezzanine because mezzanine is more of a split debt/equity focus, and you want to focus on the credit side.

What are some of the key maintenance covenants that you would analyze in a credit deal?

Maintenance covenants relate to financial metrics that the company must maintain after it raises debt.

The most common ones include the Leverage Ratio, or Debt / EBITDA, and the Interest Coverage Ratio, or EBITDA / Interest (and variations like Net Debt rather than Debt, or EBITDA – CapEx rather than EBITDA).

For example, secured loans often require companies to maintain Debt / EBITDA below a certain number, such as 5x, and EBITDA / Interest above a certain number, such as 2x.

How do you calculate the Fixed Charge Coverage Ratio (FCCR) and the Debt Service Coverage Ratio (DSCR), and what do they mean?

Both metrics may be defined in slightly different ways, but the FCCR is usually something like (EBIT + Non-Interest Fixed Charges) / (Non-Interest Fixed Charges + Interest Expense + Mandatory Principal Repayments).

The FCCR tells you how well the company’s business earnings can pay for its “fixed” expenses, such as rent/leases, utilities, and debt interest and principal repayments. Higher coverage is better.

The DSCR can also be defined differently, but we often use (Free Cash Flow + Interest Expense) / (Interest Expense + Mandatory Principal Repayments).

Some people also use EBITDA – CapEx, EBITDA – CapEx – Cash Taxes, or other variations in the numerator.

This one measures a company’s ability to pay for its debt with its business cash flow, and it does not consider other fixed expenses such as rent. Higher numbers are better.

What qualities would you look for in a company that’s seeking funding from us?

This one is covered in the corporate banking article; the criteria are quite similar.

You want companies with predictable, locked-in, recurring revenue, ones that can survive a downturn or industry decline, ones with low existing debt levels, and ones with low CapEx requirements and fixed expenses.

It also helps to be an industry leader in a growing market.

How can you quickly approximate the Yield to Maturity (YTM) on a bond?

We have a tutorial on this one, so please refer to it:

How to Approximate the Yield to Maturity (YTM) on Bonds

Suppose that we issue a $200 million loan to a middle-market IT services company to fund a leveraged buyout. It has a 7-year maturity, a floating interest rate of Benchmark Rate + 600 bps, an origination fee of 1%, and a prepayment penalty of 2%. What is the approximate IRR if the company repays this loan at the end of Year 5, and the Benchmark Rate rises from 1% in Year 1 to 3% in Year 5? Assume no principal repayments.

The interest rate here starts at 7% and rises to 9% by the end, so the “average” rate is 8%.

The origination fee is 1%, and the prepayment fee is 2%, so the lender earns 3% extra over 5 years; 3% / 5 = slightly more than 0.5% since 3% / 6 is exactly 0.5%.

You could say, “Between 8% and 9%, but slightly closer to 9%” for the answer.

In Excel, the IRR is 8.51%.

Direct Lending Case Studies and Modeling Tests

If you get a case study or modeling test, it will likely take this form:

“Please read this CIM or a few pages of information about this company, build a 3-statement or cash flow model, and make an investment recommendation about the potential Term Loan A/B or other loan issuance.”

If this is an on-site case study for 90 minutes up to 3-4 hours, skip the fancy models and create Income Statement projections, a bridge to Free Cash Flow, and a simple Debt Schedule.

You do not need to calculate the equity IRR, you don’t need purchase price allocation, and you don’t need the full financial statements to complete these case studies.

Building the correct operational cases, focusing on the pessimistic scenarios, and make sure you include the right credit metrics, such as the DSCR and Leverage and Coverage Ratios.

Sensitivities help but are not necessarily essential if you have reasonable scenarios.

Credit case studies are all about assessing the downside risk and rejecting deals where there’s even a chance of losing money if the company performs below expectations.

For a good example of what to expect, see our Debt vs. Equity case study on YouTube:

Debt vs. Equity Analysis: How to Advise Companies on Financing

Your write-up can follow the standard structure: yes or no decision in the beginning, the credit stats and potential losses in different cases, and the qualitative factors that support your decision (e.g., resistance to recessions, recurring revenue percentage, customer and revenue diversification, margin strength, fixed costs, and industry position).

If this is more of a take-home case study where you have several days or a week to finish, you still should not create a super-complex model.

Use cash flow projections and build the full financial statements only if they’re required.

Instead, use the extra time to do additional research so you can back up your numbers more effectively when you present your recommendation.

Direct Lending Jobs: Deals, Work, and Hours

The direct lending job itself, at least as an Associate, is similar to what you do in other credit and buy-side roles: origination, due diligence, process work, and financial modeling.

However, the “due diligence” part is often compressed because you look at so many deals and need to decide quickly.

It’s not like private equity, where your team could potentially take months to dig through a single company’s financial data and do on-site diligence.

The steps in a typical deal process might look like this:

1) Receive Non-Disclosure Agreement (NDA) from a Banker or Financial Sponsor – You then mark it up and agree on the changes, and both sides execute it so that you can receive information about the company and deal.

2) Receive and Analyze the Confidential Information Memorandum (CIM) – The bank or financial sponsor sends you the CIM, you build a simple cash flow model to assess the credit risk, and your team makes an initial decision on whether to go forward.

3) Submit an Indication of Interest (IOI) or Letter of Intent (LOI) – You outline your proposed investment terms, including the maturity of the loan, the fees, the interest rate, and so on.

4) Advance to the Next Round – If you’re selected, you complete more due diligence over the next few weeks, including a more detailed model, a review of the data room, and more detailed analysis of customers, revenue sources, and profitability by product/region/customer.

5) Write and Present Your Findings – You’ll then write a more detailed credit memo and present your findings to the investment committee.

6) If Approved, Close the Deal and Monitor the Company – If the committee likes it, they’ll approve the deal and transfer the funds, and you’ll start monitoring the company and reviewing its performance each quarter.

If you’re at an independent direct lending or private debt fund, the average weekly hours might be in the 50-60 range, with occasional spikes when deals close.

The hours are shorter than those in traditional private equity because direct lenders tend to do less due diligence, they have less concentrated portfolios, and they rely on sponsor relationships rather than cold outreach to win deals.

However, note that if you’re in direct lending at a PE mega-fund, your hours and stress levels might be nearly the same as they are in traditional PE.

The Top Direct Lending Funds

There are two main groups: managers linked to much larger private equity firms/hedge funds/investment banks, and “independent” managers with a credit focus.

In the first category are firms like Ares, Goldman Sachs Merchant Banking, Apollo, Bain Capital, KKR, Blackstone (GSO), Cerberus, Fortress, and Centerbridge.

In the second category are firms like Oaktree, Golub, Intermediate Capital Group, HPS Partners, PennantPark, Crescent Capital, Owl Rock, CarVal Investors, Hayfin, First Eagle, Maranon, and dozens of others.

Many of these firms also make mezzanine and other private debt investments, and some even make growth equity and equity co-investments as well.

Direct Lending Salary + Bonus Levels

While direct lending funds and private equity funds have similar business models, there are a few important differences:

- Fees Are Often Lower – For example, the management fee might be closer to 1% rather than 2%, and the incentive fee might be 10% or 15% rather than 20%.

- Fees Might Be Charged Based on Deployed Capital Rather Than Raised Capital – So, if your fund raised $1 billion but has only invested $200 million, the 1-2% management fee might be charged on the $200 million rather than the $1 billion.

As a result of these differences, average compensation tends to be lower.

The rule of thumb is “Take IB/PE base salaries and assume lower bonuses.”

So, the approximate total compensation ranges are:

- Analyst: $90K to $140K

- Associate: $125K to $250K

- Senior Associate / Assistant Vice President: $200K to $350K

- Vice President: $300K to $500K

- Principal / Senior Vice President: $450K to $700K

- Managing Director: $400K to just over $1 million

The bonus starts at a relatively low percentage of base salary (10 – 50%), but rises to 100% by the mid-levels and potentially over 100% for MDs.

These are wide compensation ranges because of the differences between different fund types.

For example, an Associate who just finished an IB Analyst program and joined a larger, well-known direct lender might earn total compensation of $200K to $250K.

But at a smaller firm that’s unattached to a large bank or PE firm, total compensation might be closer to $150K.

The bottom line: you still earn a lot in direct lending, but it is a discount to private equity salaries and bonuses, and the “ceiling” tends to be lower because of the lower fees.

Note that we’re not including carried interest in these figures – if we did, there would be an even bigger difference between DL and PE pay at the top levels.

Direct Lending Exit Opportunities

After the “What is direct lending?” question, the second-most-common one is “What do people do after direct lending? What are the exit opportunities? Show me the exit opps!!”

Unfortunately, the answer is quite boring: “Stay in the space and work their way up at the same fund or move to a different fund.”

One of the major disadvantages of direct lending is that it tends to be difficult to move into other industries, even ones related to credit, such as distressed private equity, standard private equity, or credit hedge funds.

The issue is that you work mostly with secured debt, not the high-yield or distressed issuances that these other firms buy and sell.

Also, while PE and DL share some aspects, the “investing philosophy” is quite different since one is a pure equity role, and the other is a pure debt role.

I’m sure that some people have moved from DL to PE, but it’s more difficult than you would think; the reverse move is easier.

Mezzanine funds might be one potential exit opportunity, especially if you worked at a fund that did more than secured loans.

And if you go to a mezzanine fund, you open up exit opportunities at some of the other firm types mentioned above.

These limited exit opportunities also explain why it may not be a great idea to start in direct lending out of undergrad: Leveraged Finance would pay you more and give you more options.

Is Direct Lending Right for You?

You would be a good fit for direct lending if you want to work on many different deals but not go into each one in extreme depth, and you want to do only credit analysis without considering the equity side.

You would also be a good fit if you want a slightly better lifestyle, still-high-but-lower-than-PE compensation, and you want to stay in credit for the long term.

You would not be a good fit if you want to analyze the equity side of deals, work directly with portfolio companies’ operations, or make the most amount of money possible.

Also, if you’re not sure you want to be in credit for the long term, stay away – because most people in direct lending do end up staying for the long term.

Personal Opinion: While direct lending roles are fine, you could get many of the same benefits (shorter hours in exchange for slightly lower pay, more deals, etc.) by joining a mezzanine fund.

You would also gain access to more exit opportunities, so you could move around more easily if you decide it’s not for you.

So, I’m not sure why you’d choose direct lending over mezzanine if you interview around and win offers in both fields.

For Further Learning

Here are some links if you want to learn more about the field:

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Comments

Read below or Add a comment

Hey Brian,

I work in sponsor finance in commercial banking; we make first lien loans for private equity transactions. Do you think this is helpful experience for direct lending roles?

Potentially, yes.

Useful article! Do you know what the responsibilities, comp, and exit opps look like for a portfolio management analyst or associate at a direct lender?

Different lending shops define PM differently and some have a separate team for it whereas others have associates handling PM tasks in addition to sourcing / underwriting / DDing new investments. Thanks.

Sorry, we don’t have information on that one. Most compensation surveys do not have much specific information on direct lending or differences in the different DL groups.

Hi Brian, thanks for the article. I am headed into a corporate banking role this summer in a bank with CIB umbrella structure. I sometimes get confused when you refer to lack of deal experience when it comes to corporate versus investment banking roles: if I am doing credit analysis/due diligence, modeling, and helping to execute on project financing, term loans, etc. where my firm has “skin in the game”, why are those less of a transaction than syndicating loans on the LevFin or DCM side?

CB deals are somewhat different because you don’t necessarily do as much modeling work, and the hours and intensity are lower because the debt issuances in CB are usually not related to deals. But it does vary by bank, and at some firms, there’s barely any difference between CB and IB, or they’re even grouped together.

Hi Brian,

I’m currently a student looking at a prospective summer internship.

I was wondering what are your thoughts regarding Credit Portfolio Advisory (specifically at Alantra, Dublin). They have a team that apparently advises on credit transactions.

My eventual goal was to join a credit fund like GSO or Guggenheim but this idea of ‘advising’ on credit transactions somewhat confuses me (as I thought all decisions were analysed and made by the deal parties without ‘middlemen advisors’).

Job description looks pretty similar to a credit fund analyst (but considering those are written by HR… I’d rather not trust them lol).

Any opinions on this credit advisory service, Alantra, exit ops etc. is much appreciated if you have any insight^

Thank you!!!

Sorry, I don’t know enough about that specific group to say much. From the description, it seems like the exit opportunities would be similar to the ones discussed here. Not sure if the top credit funds would be realistic, but other credit funds, direct lenders, maybe mezzanine, etc. would be possible.

Hey Brian. Have you seen individuals move from commercial banking (C&I Lending) straight to Direct Lending? What do you think are the main areas or skills a commercial banking lender should focus on in order to transition his or her career to direct lending?

Not offhand, no, because the skill sets are somewhat different. You need to show more evidence of financial modeling and investing skills to move into direct lending. I’m sure some people have moved in from commercial banking, but it’s not as easy as you might think.

Hey Brian,

Great article. Do you know of any shops that hire recent grads with little to know experience?

Thanks. Some of the mega-funds that also have credit arms do hire undergrads (Apollo, Bain Capital Credit, KKR Credit, Ares, Oaktree, etc.). But you usually need some type of experience, such as previous internships, to have a good shot at those.