WACC Formula: Quick Calculations, Interview Questions, and More

If I had to pick a single concept in corporate finance< most deserving of the “much ado about nothing” award, it would be WACC (the Weighted Average Cost of Capital).

In a standard discounted cash flow (DCF) model based on Unlevered Free Cash Flow, WACC represents the Discount Rate: the expected or required annualized return from investing in the company you’re valuing.

Many textbooks and academic sources spend an insane amount of time and energy on detailed calculations for this number.

Banks sometimes do the same, but they’re a bit less extreme – and at least they’re getting paid for it.

The WACC formula, which is what everyone seems to Google, is easy:

WACC = Cost of Equity * % Equity + Cost of Debt * (1 – Tax Rate) * % Debt + Cost of Preferred Stock * % Preferred Stock

And if you want to be fancy and add Leases into the mix, it becomes:

WACC Including Leases = Cost of Equity * % Equity + Cost of Debt * (1 – Tax Rate) * % Debt + Cost of Leases * (1 – Tax Rate) * % Leases + Cost of Preferred Stock * % Preferred Stock

As with many other financial concepts, the formula is simple; the real difficulty is determining the right inputs with limited time.

WACC Formula: Video Tutorial and Excel Templates

If you’d prefer to watch rather than read, you can get this [very long] tutorial below:

Table of Contents:

- 2:08: Part 1: The Big Idea Behind the Discount Rate

- 3:15: The WACC Formula

- 4:47: Part 2: Quick-and-Dirty WACC

- 10:40: Part 3: More Complex Calculations

- 18:25: Cost of Equity and WACC

- 22:57: Part 4: Leases in WACC: What to Do

- 28:11: Part 5: WACC Interview Questions

- 31:33: Recap and Summary

And here are the accompanying Excel files:

- Sample WACC Calculation for Steel Dynamics, With and Without Leases

- WACC Formula – Slide Presentation

- Steel Dynamics 10-K with Relevant Areas Highlighted

The Big Idea Behind the WACC Formula

The DCF model is based on projecting companies’ cash flows years or decades into the future.

But since $1,000 in 10 years is worth less than $1,000 today – as we could invest it today and earn more by then – we need to discount these future cash flows to their Present Value.

For a standard DCF based on Unlevered Free Cash Flow, i.e., a company’s core-business cash flows available to all investors in the company, WACC is the appropriate Discount Rate:

WACC = Cost of Equity * % Equity + Cost of Debt * (1 – Tax Rate) * % Debt + Cost of Preferred Stock * % Preferred Stock

The Cost of Equity represents the potential returns from the company’s stock price increasing and its dividends.

The Costs of Debt and Preferred Stock represent the potential returns from the interest or dividends they pay and the changing market value of these items.

If you invest proportionally in the company’s capital structure, WACC represents what you might earn, annualized, over the long term.

For example, maybe you’re valuing a company with 80% Equity, 20% Debt, and a 25% Tax Rate.

If you want to invest $1,000, a proportional investment would be $800 in its Equity (the common shares) and $200 in its Debt.

This company’s stock price has increased by 8% per year over the long term, on average, and its dividends have produced an additional 2% in annualized returns.

This company’s yield on its Debt is 6%, and similar companies yield around the same 6%.

Therefore, the Cost of Equity is 2% + 8% = 10%, and the pre-tax Cost of Debt is 6%.

Since the interest paid on Debt is tax-deductible, it “costs” the company less than 6% per year, so we multiply by (1 – Tax Rate), or (1 – 25%), here:

WACC = 10% * 80% + 20% * 6% * (1 – 25%) = 8.9%

So, in theory, you’ll earn $89 per year over the long term from this investment… but most of these returns come from the company’s stock price going up, so you won’t see them in cash until you sell your investment.

Also, anything could happen in a single year or even a few years, so you could easily lose money in the short term.

Because of all these issues, it’s best to think of WACC as a metric where you should aim to be “roughly correct” rather than “precisely wrong.”

The WACC formula should produce very different results for a pre-revenue startup vs. a mature, profitable company, but the differences are more difficult to pin down within these categories.

WACC Formula: The Quick-and-Dirty Method

Fortunately, you can make a quick approximation for WACC with about 5 minutes of work.

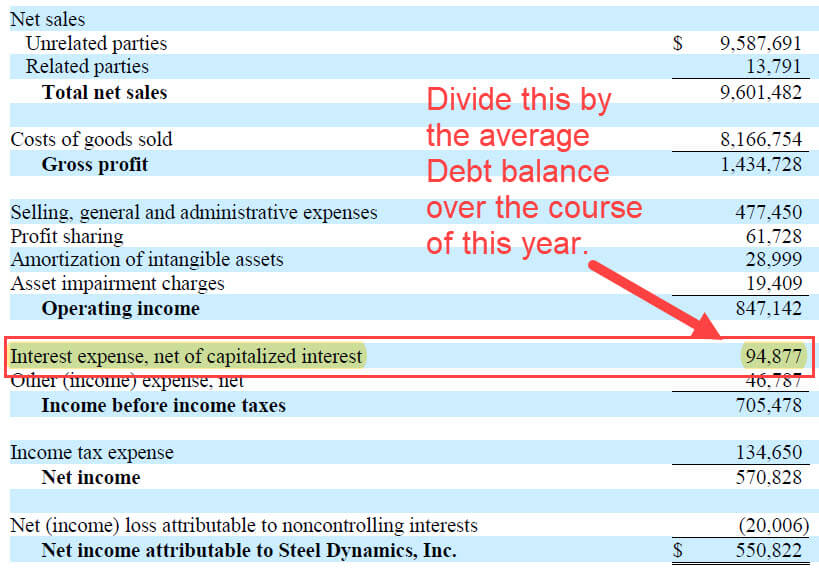

Start by looking up the market cap, or Equity Value, of the company you’re valuing and finding its Debt and Preferred Stock figures in its filings (example for Steel Dynamics below):

You can use these numbers to calculate the % Equity, % Debt, and % Preferred Stock in its capital structure:

To estimate the Cost of Debt, you can take the Interest Expense on the annual Income Statement and divide it by the average Debt balance over the period:

If you’re using a quarterly or half-year report, you’ll have to annualize this figure.

The same approach applies to Preferred Stock; you can often skip this step because Preferred Stock is rare for most modern companies.

Estimating the Cost of Equity is trickier, but the most common method is:

Cost of Equity = Risk-Free Rate + Equity-Risk Premium * Levered Beta

The idea is to take what you could earn in “risk-free” government bonds – the Risk-Free Rate – add the additional return offered by the stock market – the Equity Risk Premium – and then multiply by a factor representing this company’s volatility relative to the market’s – Levered Beta.

In theory, this represents what the company’s stock price + dividends “should” return on an annualized basis over the long term.

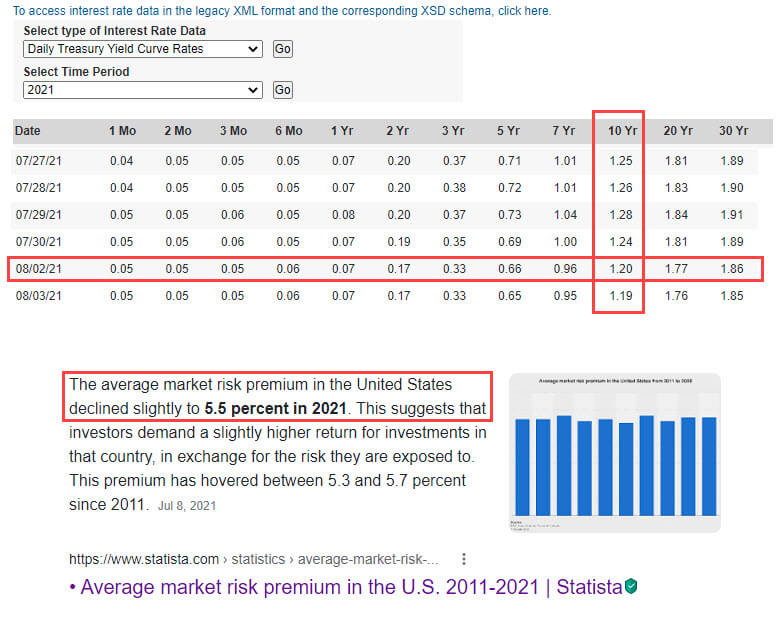

You can find the Risk-Free Rate based on 10-year government bond yields in the company’s country (easy to look up online), and Equity Risk Premium estimates are fairly easy to find as well:

To find Levered Beta for the company you’re valuing, you can use sources like Finviz or Yahoo Finance (or paid services such as Capital IQ if you have access):

And in a few minutes of work, you can turn the WACC formula into a rough estimate for this company:

WACC Formula: The More Complex Method

The method above is simple, efficient, and produces decent results, so why go beyond it?

Like everything else in financial modeling, you can make the WACC formula as easy or as complicated as you want, and banks like to make things complicated.

The main reasons to do so are:

- To get a proper range of values for WACC. We want to know if a company’s Discount Rate should be between 10% and 12% or between 6% and 8%, for example.

- It’s more accurate to calculate the Costs of Debt and Preferred Stock by factoring in their market values. And it may be more accurate to estimate the risk and potential returns in the Cost of Equity by analyzing the comparable companies.

We’ll start with the Cost of Debt since that’s easier to explain.

With this one, it’s best to look up the fair value or fair market value of the Debt and use it in the capital structure calculations (as opposed to the book value, which appears on the company’s Balance Sheet).

You can also use these fair values to calculate the yield to maturity (YTM) of the Debt, which reflects premiums and discounts (if the Debt trades at a discount to its par value, the investor will earn more than the stated coupon rate if they hold it until maturity).

Here’s an example for Steel Dynamics (based on the annual filings since it doesn’t close the fair value of Debt in detail in its interim filings):

This “slightly more accurate” method produces 2.22% for the Cost of Debt rather than 3.25%.

That may seem like a big difference, but the company uses only ~20% Debt, so it barely changes WACC.

There are other ways to approximate the Cost of Debt; for example, you could take the Risk-Free Rate and add an estimated credit default spread based on the company’s credit rating.

You could also look at the YTMs on similar debt issuances from comparable companies, but this one requires a lot more work (see below).

Cost of Equity in the WACC Formula: Added Complications

There are several ways to make the Cost of Equity calculation more complicated, but the main one is to go through a process known as un-levering and re-levering Beta.

Rather than using the company’s own historical Beta – how it performed against its own stock-market index – it may be more accurate to measure risk and potential returns based on other, similar companies in the industry.

All companies have two types of risk: risk from operating their core business and risk from leverage (Debt).

The “Beta” figures you find on sites like Yahoo Finance and Finviz include both risks, so they are known as “Levered Beta.”

To separate the business risk, the first step is to find a set of comparable companies and look up the Debt, Equity, Preferred Stock, Beta, and Tax Rate figures for each one:

We can then “un-lever” Beta for each company by reducing it based on the company’s leverage:

Unlevered Beta = Levered Beta / (1 + Debt / Equity * (1 – Tax Rate) + Preferred / Equity)

Dividing by a term that starts with “1 +” ensures that Unlevered Beta will always be less than or equal to Levered Beta.

Once we have this for all the peer companies, we can “re-lever Beta” by following the process in the opposite direction for Steel Dynamics:

Re-Levered Beta = Unlevered Beta * (1 + Debt / Equity * (1 – Tax Rate) + Preferred / Equity)

“Re-levering” Beta like this takes the inherent business risk from the comparable companies and then adjusts it upward for this company’s risk from leverage.

But there is one question: do we use the company’s current capital structure, or its “optimal” or “targeted” structure?

The argument for the latter is that over time, any company will start to resemble other, similar companies in the industry in terms of capital structure.

So, it may be more accurate to use the median percentages from the comparable companies instead. We use both approaches here:

As a result of these different calculation methods for Beta, we now have three different ways to calculate the Cost of Equity and WACC:

- Method #1: Use the company’s own historical Beta and its current capital structure.

- Method #2: Base Beta on the comparable companies but use the company’s current capital structure.

- Method #3: Base Beta and the capital structure on the comparable companies.

There is no “best” method; the point is to establish a plausible range of values.

Here are the results for Steel Dynamics:

As a rule of thumb, a good range of WACC values for mature companies spans about 2-3% from the minimum to the maximum.

So, 10-12% or 6-9% would be fine.

But 5-10% might be a bit too wide, and 5-15% would be too wide to be useful.

(Exceptions apply in emerging markets and for more speculative companies.)

How to Deal with Leases in the WACC Formula

We published a detailed tutorial on lease accounting, so you should refer to that for the fundamentals.

The main issue here is that lease accounting worldwide changed in a major way in 2019, and people are still figuring out how to deal with leases in models and valuations.

At a high level:

- Companies often group Finance Leases with their Debt balances, and they tend to be quite small, so they rarely make a significant impact on WACC. Historically, people ignored them and didn’t break them out as separate items.

- Since Operating Leases moved onto companies’ Balance Sheets in 2019, there have been many questions about how to treat them in the DCF and the WACC formula. They are much bigger than Finance Leases for most companies, which makes the decision more significant.

Our recommendation is to not count Operating Leases as a form of capital in the WACC formula and to deduct the full Operating Lease Expense in the Free Cash Flow projections.

Regardless of how a company classifies its leases, the lease expense still represents a cash outflow resulting from the company’s business operations, and the DCF is based on cash inflows and outflows from the core business.

A company’s leases are mostly operational decisions based on where it needs employees and production capacity.

Therefore, it doesn’t make much sense to say that leases represent “outside investors” in the same way Debt and Preferred Stock do.

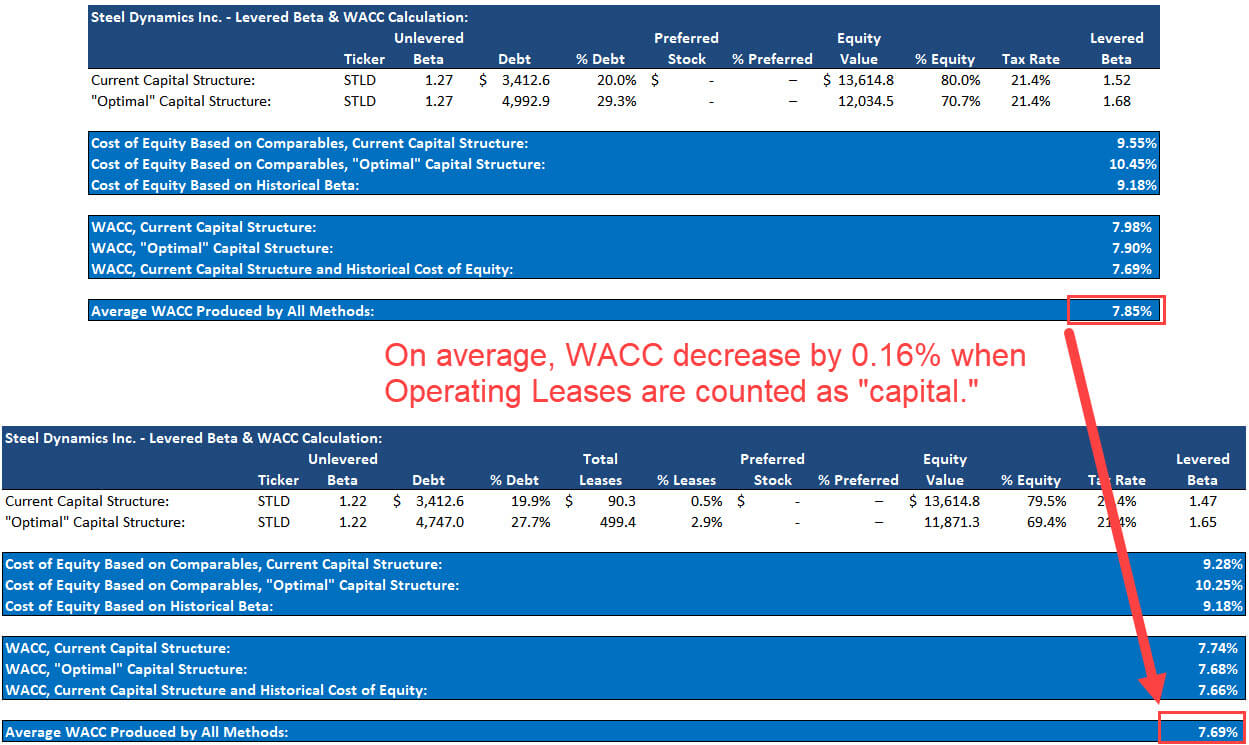

But if you wanted to, you could count Operating Leases as capital by modifying the Unlevered Beta, Re-Levered Beta, and WACC formulas to include an extra term (we separated Finance Leases from Debt and added them to Operating Leases here):

In the WACC formula, you can find the Pre-Tax Cost of Leases by looking up the discount rate the company uses to calculate its Lease Liabilities in its filings:

In this case, the results barely change:

WACC decreases by 0.16% because Leases are, effectively, another low-cost funding source for this company.

If we do this in the WACC calculation, we also need to modify the Enterprise Value calculations to include Leases and add back or exclude the full Lease Expense in Unlevered Free Cash Flow.

The company’s implied value tends to increase because the lower WACC affects everything more than the subtraction for the Lease liability in the Enterprise value bridge.

But it’s extra work that makes almost no difference in the DCF output, so it’s hard to recommend this approach in a valuation.

Interview Questions About WACC

The most common interview questions here are variations of:

- “Item X goes up. How does WACC change?”

- “Item Y goes down. How does WACC change? What about the implied value from a DCF?”

This chart sums up the most common topics:

To understand these points intuitively, think about the risk and potential returns for each component of WACC.

For example, smaller companies and ones in emerging markets tend to be riskier but also have higher growth potential than larger companies and ones in developed markets.

Therefore, you’d expect WACC to be higher, along with components like the Cost of Equity and Cost of Debt.

Some of these points are a bit tricky; increased Debt, for example, tends to reduce WACC at first but then increases it past a certain level.

The rationale is that at minimal or low Debt levels, the cost advantages of Debt outweigh its drawbacks (the added risk of bankruptcy), but above a certain level, the bankruptcy risk starts to dominate everything else.

Note that you won’t “see” a change like this directly in a model unless you make the Cost of Debt change as the company’s Debt % changes.

For Further Learning About WACC

If you want to learn more about DCF models and concepts like WACC and get a step-by-step walkthrough, sign up for our free financial modeling tutorials.

These tutorials cover a 3-part series on the valuation of Michael Hill, a retailer in Australia and New Zealand, and they explain the entire process from beginning to end.

And if you want in-depth case studies backed by real-world data and research, the Core Financial Modeling course delves into valuation/DCF analysis in even greater detail:

Core Financial Modeling

Learn accounting, 3-statement modeling, valuation/DCF analysis, M&A and merger models, and LBOs and leveraged buyout models with 10+ global case studies.

learn moreA few modules are dedicated to valuation and DCF analysis, and there are example company valuations in other industries.

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street. In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews